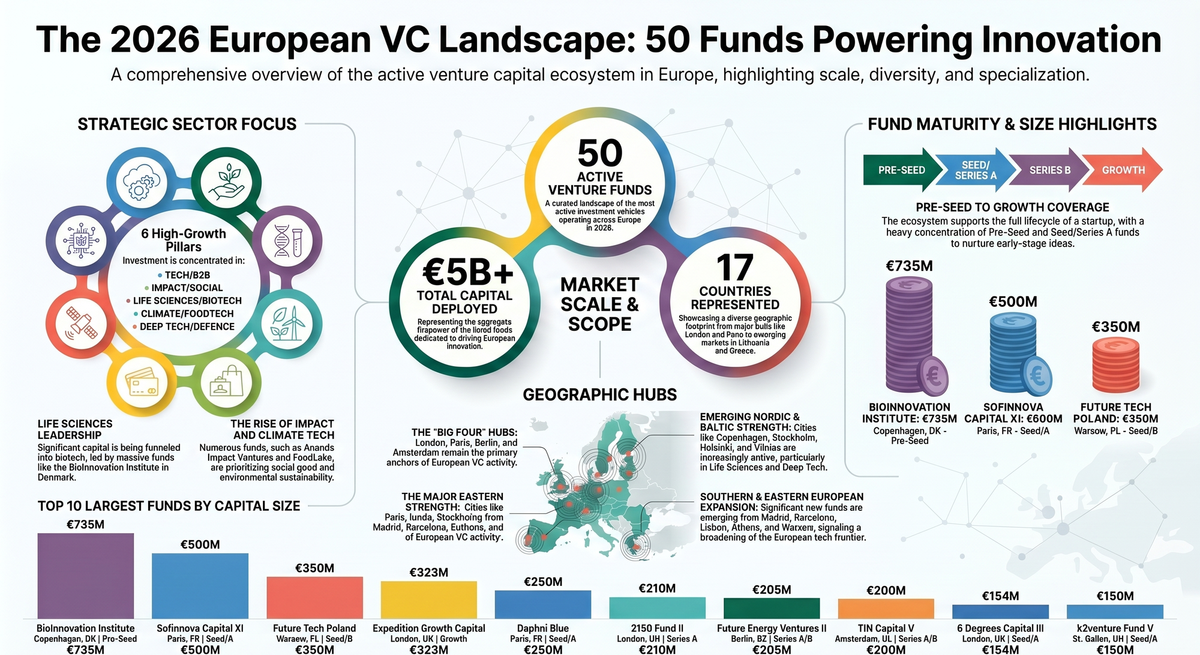

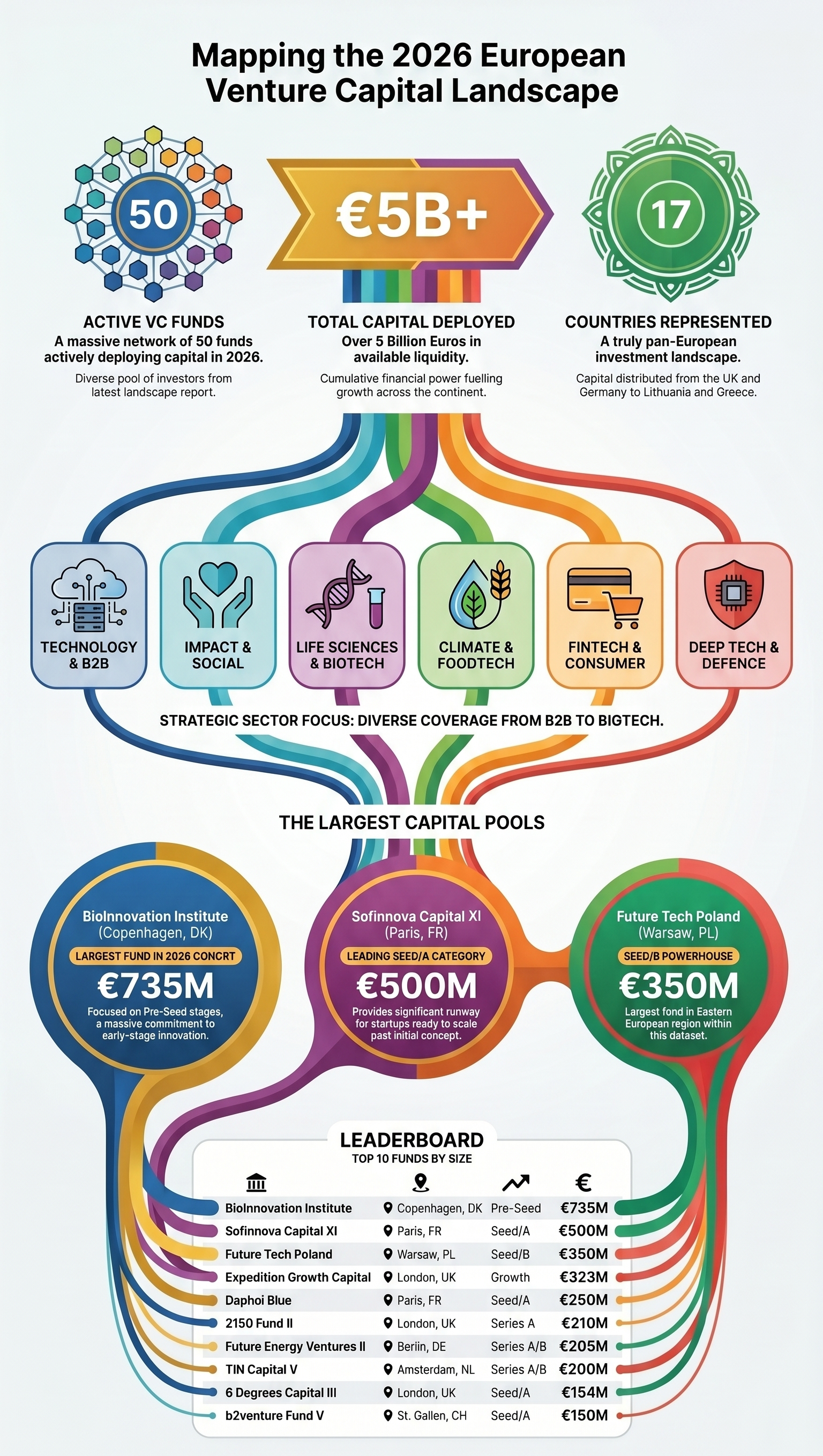

50 European VC Funds Actively Investing in 2026

A Comprehensive Guide to Active Venture Capital Funds Across 17 Countries, 6 Sectors, and Over 5 Billion Euros in Capital

Europe's venture capital ecosystem has entered a period of remarkable transformation. After a challenging cycle between 2022 and 2023 when rising interest rates and global uncertainty caused funding volumes to contract sharply, the continent's startup economy has re-emerged with renewed energy. Fresh fund formations, bolder thesis-driven mandates, and a widening geographic footprint across Central and Eastern Europe are reshaping the landscape in ways that founders, investors, and observers should pay close attention to.

This guide presents 50 venture capital funds that are actively deploying capital across Europe in 2026. These are not passive or historical names. Each fund on this list has recently raised or closed a new vehicle and is now in active deal-making mode, seeking founders, reviewing term sheets, and building portfolios. Together, they represent more than 5 billion euros in committed capital, span 17 countries, and cover six major sectors: Technology and B2B, Impact and Social, Life Sciences and Biotech, Climate and FoodTech, Fintech and Consumer, and Deep Tech and Defence.

Understanding who these funds are, what they back, at what stage they write their first check, and what signals they look for in founders is valuable not only for startup founders seeking capital but also for limited partners evaluating fund managers, corporate innovation teams mapping the competitive landscape, and researchers tracking the direction of European private markets.

The data, fund descriptions, and sector observations in this guide are drawn from public fund announcements, press releases, and market research current as of early 2026. Each section is organized to give readers a fast, clear picture of who these funds are and what distinguishes them from one another.

Key Takeaways

|

European

VC is in active deployment mode heading into 2026, with over 50 newly closed

funds seeking founders. |

|

The

geographic footprint has expanded beyond London, Paris, and Berlin into

Poland, Portugal, Lithuania, Greece, and the Baltic states. |

|

Six

sectors dominate: Technology/B2B, Impact/Social, Life Sciences,

Climate/FoodTech, Fintech/Consumer, and Deep Tech/Defence. |

|

Pre-seed

and seed-stage capital dominates the list, signaling that early-stage

conviction is strongest among European fund managers right now. |

Section 1: The European VC Landscape in 2026 – An Overview

European venture capital in 2026 is defined by a set of structural forces that distinguish it sharply from prior cycles. The first is the continued dominance of early-stage investing. Pre-seed and seed funds account for a disproportionate share of the 50 vehicles in this guide, a clear signal that the market has become more cautious at growth and late stages while conviction at the earliest stages remains intact. Climate change, aging populations, food system fragility, and geopolitical pressure are generating real, urgent problems that founders are racing to solve, and early-stage fund managers are betting on that urgency.

The second force is geographic diversification. For years, European startup capital was effectively concentrated in London, Paris, and Berlin, with Stockholm and Amsterdam as strong secondary hubs. That picture has evolved significantly. Warsaw has emerged as a serious capital for deep tech and B2B software investing. Lisbon has become a destination for Atlantic-facing founders who want access to both European and Latin American markets. Copenhagen and Helsinki represent mature but still undervalued ecosystems for life sciences and climate ventures. Athens and Vilnius are entering the map for the first time with institutional-quality early-stage funds.

The third force is sector specialization. Generic tech-agnostic funds are giving ground to vehicles with sharp theses. The 50 funds in this list include funds dedicated exclusively to FoodTech, funds built around biotech acceleration, defence and dual-use technology vehicles, impact-only mandates, and funds with explicit bioeconomy or circular economy frameworks. This specialization benefits founders who are building in focused domains and need investors who genuinely understand their space rather than generalists who are learning alongside them.

A fourth force worth noting is the role of public capital. The European Investment Fund, the European Investment Bank, national development finance institutions from Germany, France, Poland, and Portugal, and mission-driven foundations like the Novo Nordisk Foundation have become systematic anchors for new VC fund formation across the continent. Several funds on this list received first-close anchor commitments from public institutions, which has lowered the fundraising friction for first-time fund managers and allowed more geographically distributed funds to reach institutional scale.

Key Takeaways

|

Pre-seed

dominance signals that early-stage conviction is the primary driver of new

European VC formation in this cycle. |

|

Geographic

diversification is real: Warsaw, Lisbon, Copenhagen, Athens, and Vilnius now

have institutional-quality local funds. |

|

Sector

specialization is accelerating, with funds built around tight theses in

FoodTech, biotech, defence, and climate. |

|

Public

capital institutions like the EIF, EIB, and Novo Nordisk Foundation are

systematic anchors for new European fund formation. |

🚀 1000+ Angel Investors

A massive, curated list of angel investors actively funding early-stage startups.

Whether you're building your first product or scaling fast — this is your shortcut to reaching the right backers.

- ✔️ 1000+ verified angel investors

- ✔️ Early-stage & seed-focused

- ✔️ Save months of investor research

- ✔️ Built for founders, freelancers & creators

Limited-time access. Get in front of investors before everyone else does.

Section 2: Funds 1 to 10 – UK and DACH Region Leaders

The first ten funds on this list are concentrated primarily in London and Munich, reflecting the continued dominance of those two cities as the principal poles of early-stage European venture capital. Within this cohort, the range of check sizes and stage focus is notably wide, from micro-funds writing initial checks below 500,000 euros to institutional-scale vehicles deploying hundreds of millions.

1. 6 Degrees Capital III (London, UK) – Seed/A – 154 Million Euros

6 Degrees Capital is a London-based B2B technology fund focused on software and data infrastructure companies across Europe. The third fund builds on a thesis that enterprise software companies in Europe are systematically undervalued relative to their US counterparts and that a concentrated portfolio of fifteen to twenty high-conviction bets will outperform broader market approaches. The fund writes initial checks in the range of five to ten million euros and is built around a network of operator-investors who serve as active board members and strategic advisers.

2. 2150 Fund II (London, UK) – Series A – 210 Million Euros

2150 is a purpose-built urban technology fund with a distinctive focus on the built environment, infrastructure, and city systems. Fund II continues the thesis from its debut vehicle: that the world's cities are fundamentally broken in terms of energy consumption, housing affordability, waste generation, and transportation efficiency, and that the companies solving those problems will be among the most valuable of the next decade. The fund backs founders at Series A working on construction technology, smart energy, urban mobility, and digital infrastructure for cities.

3. Ananda Impact Ventures V (Munich, Germany) – Seed/A – 73 Million Euros

Ananda Impact Ventures is one of Europe's longest-standing dedicated impact funds, with five successive vehicles and a track record stretching back more than a decade. The Munich-based team backs founders whose companies deliver measurable social and environmental returns alongside financial performance. The fund's portfolio spans health access, education, employment technology, and rural economic development. Ananda uses a proprietary impact measurement framework to track portfolio outcomes beyond standard financial metrics.

4. Aniel Capital (Vilnius, Lithuania) – Seed/A – 35 Million Euros

Aniel Capital represents the growing maturity of the Baltic startup ecosystem. Based in Vilnius and deploying capital across the Baltic states and wider CEE region, the fund backs B2B software, fintech, and deep tech founders at seed and early Series A. Lithuania has developed a disproportionately strong fintech licensing and regulatory infrastructure, making Vilnius an increasingly attractive base for regulated technology businesses, and Aniel Capital is positioned to benefit from that structural advantage.

5. Armilar Venture Partners IV (Lisbon, Portugal) – Series A – 120 Million Euros

Armilar is Portugal's leading institutional venture fund and one of the oldest in Southern Europe. Fund IV focuses on Series A investments in technology companies with meaningful traction and an ability to scale across European and Latin American markets. Lisbon's geographic and cultural proximity to Brazil and the Portuguese-speaking world gives Armilar-backed companies a natural bridge for international expansion that few European funds can replicate. The team has a strong track record in B2B SaaS, cybersecurity, and digital health.

6. Backed VC III (London, UK) – Pre-Seed – 86 Million Euros

Backed VC is a London-based pre-seed fund with a distinctive operating model: the team runs structured residency programs for early-stage founders, providing intensive support before and immediately after making investment decisions. Fund III continues this model with a focus on consumer and B2B technology. Backed has historically backed founders from underrepresented backgrounds at higher rates than the sector average, a deliberate portfolio construction choice that the team argues produces better-distributed deal flow and stronger founder loyalty.

7. Balnord I (Luxembourg) – Seed/A – 70 Million Euros

Balnord is a recently launched fund with a focused mandate to back deeptech and dual-use companies in the Baltic Sea region, an area that encompasses Sweden, Finland, Estonia, Latvia, Lithuania, Poland, Germany, and Denmark. The fund reached its first close exceeding its initial target and is tracking toward 100 million euros by mid-2026. The Baltic Sea region has developed significant strength in cybersecurity, robotics, and defence technology, and Balnord positions itself as a specialist investor in that corridor with a mandate that explicitly includes dual-use applications.

8. Baseline Venture Fund (Dublin, Ireland) – Pre-Seed – 51 Million Euros

Baseline is Ireland's most active pre-seed fund and operates as a key early entry point into the Irish startup ecosystem for founders across enterprise software, fintech, and climate technology. The fund writes initial checks between 250,000 and 750,000 euros and provides hands-on operational support through a structured post-investment program. Ireland's status as a European headquarters destination for major US technology companies creates a distinctive talent pipeline and commercial go-to-market advantage for enterprise software startups, which Baseline actively leverages for its portfolio companies.

9. Baobab Ventures I (London, UK) – Pre-Seed – 12.9 Million Euros

Baobab Ventures is a micro-fund with a specific thesis around backing underrepresented founders in the UK and wider European market. The fund writes very early checks and provides intensive coaching and community support alongside capital. While the fund size is modest by institutional standards, micro-funds of this type play a critical role in surfacing talent from communities that institutional VC historically overlooks, and Baobab's portfolio construction philosophy is designed explicitly to address that gap.

10. b2venture Fund V (St. Gallen, Switzerland) – Seed/A – 150 Million Euros

b2venture is Switzerland's most active seed-stage fund and one of the leading early-stage investors in the DACH region. Based in St. Gallen and operating closely with ETH Zurich and the University of St. Gallen academic communities, the fund backs B2B software, fintech, and healthtech founders. Switzerland's status as a global headquarters for pharmaceutical, financial services, and manufacturing companies gives b2venture portfolio companies exceptional proximity to enterprise customers at scale.

Key Takeaways

|

London

and Munich continue to anchor European pre-seed and seed capital, but the

geographic expansion of serious institutional funds into Vilnius, Lisbon,

Dublin, and St. Gallen shows the ecosystem is maturing rapidly. |

|

Impact-first

funds like Ananda are entering their fifth successive vehicle, signaling that

impact investing in Europe has moved from experiment to established

institutional practice. |

|

Dual-use

and deeptech mandates are gaining ground in Baltic and Northern European

funds, reflecting the region's growing strategic importance in defence and

cybersecurity. |

|

Micro-funds

below 15 million euros are playing a critical market gap role in backing

underrepresented founders that institutional capital historically misses. |

Section 3: Funds 11 to 20 – Nordic Power and CEE Rising Stars

The second cohort of ten funds introduces the Nordic life sciences ecosystem and the rapidly maturing Central and Eastern European market. Copenhagen, Warsaw, and Paris feature prominently, and the range of fund sizes within this group is striking, from a micro-fund with just 10 million euros under management to Denmark's BioInnovation Institute with its transformational 735 million euro capital base backed by the Novo Nordisk Foundation.

11. Betacluster Fund I (Warsaw, Poland) – Pre-Seed – 15 Million Euros

Betacluster is a Warsaw-based pre-seed vehicle backed by PFR Ventures, Poland's government-backed fund of funds manager, and is one of four new Polish investment vehicles launched with PFR backing in Q4 2025. The fund focuses on building a 'Smart Data Economy' thesis in Poland, backing AI-first and data-centric startups with initial checks between 200,000 and 500,000 euros. Poland has developed exceptional technical talent through its strong university engineering programs, and Betacluster positions itself as the first institutional partner for the best founders coming out of that talent base.

12. BioInnovation Institute (Copenhagen, Denmark) – Pre-Seed – 735 Million Euros

The BioInnovation Institute is one of the most extraordinary VC-adjacent vehicles in Europe. Backed by the Novo Nordisk Foundation with a 5.5 billion Danish krone commitment, BII operates as a not-for-profit incubator and early-stage funder for life science, healthtech, and deeptech companies in Denmark and the Nordic region. BII provides startups with laboratory infrastructure, mentoring networks, and founder-friendly convertible loans of up to 1.3 million euros per startup and 2.4 million euros per project. Portfolio companies from BII's Venture House cohorts have raised over 3 billion Danish krone in follow-on capital from third-party investors. Recent portfolio graduates include Synuca Therapeutics, Gefjon Pharma, MicroMiner, and Diasense, spanning neuropharmacology, crop science, environmental sensing, and continuous glucose monitoring.

13. Catalpa Health Fund I (Luxembourg) – Seed/A – 10 Million Euros

Catalpa Health is a dedicated digital health fund backing founders working to modernize European healthcare systems through technology. The fund is small by institutional standards but highly focused, concentrating on companies building software and data infrastructure for health systems, care coordination platforms, and patient engagement tools. Luxembourg's position as a pan-European financial hub makes it a practical base for a fund that expects its portfolio companies to work across multiple European healthcare regulatory environments simultaneously.

14. Cloudberry Venture Fund (Helsinki, Finland) – Pre-Seed – 30 Million Euros

Cloudberry operates at the very earliest stage of the Finnish startup ecosystem, writing initial checks into companies that are often still refining their product and early customer base. Finland has a well-documented track record of producing globally competitive B2B software companies, gaming companies, and cleantech ventures, and Cloudberry positions itself as the earliest institutional partner for the next generation of Finnish founders. The fund participates in follow-on rounds through its reserve capital and maintains active relationships with leading Nordic and global growth investors as downstream co-investment partners.

15. Clover Fund I (Paris, France) – Pre-Seed – 30 Million Euros

Clover is a Paris-based pre-seed fund with a focus on science-first ventures emerging directly from French and European research institutions. The fund's investment thesis is grounded in the belief that the most durable technology companies are built on genuine scientific moats rather than execution advantages alone. Clover backs founders who have published research, hold patents, or have deep domain expertise that creates structural competitive advantage. Paris has emerged as a particularly strong hub for deep science startups, and Clover is positioned in the centre of that ecosystem.

16. Cocoa Ventures II (London, UK) – Pre-Seed – 21 Million Euros

Cocoa Ventures is a London-based pre-seed fund with a high-conviction, founder-focused approach. The team describes its model as lean and founder-friendly, writing early checks into consumer technology and fintech founders who show strong product intuition and distribution creativity. The second fund builds on a first vehicle that produced several notable early exits and follow-on rounds from tier-one Series A investors.

17. Cofounder VC Fund I (Warsaw, Poland) – Series A/B – 12 Million Euros

Cofounder VC is a Warsaw-based growth-focused vehicle backing revenue-generating Central and Eastern European technology companies that are ready to scale internationally. Despite its relatively modest fund size, Cofounder targets a later stage than most other Polish funds on this list, focusing on companies that have demonstrated product-market fit and are now executing a regional or global expansion strategy. The fund is backed by PFR Ventures as part of the same cohort of Polish vehicles launched in Q4 2025.

18. Daphni Blue (Paris, France) – Seed/A – 250 Million Euros

Daphni is one of France's most established and well-regarded seed and Series A funds, known for its community-driven model and its ability to attract operator limited partners who provide portfolio companies with active commercial and strategic support. Daphni Blue is the fund's flagship vehicle and builds on a track record that includes early investments in several French startup success stories. The fund is generalist by design, backing the best European founders across enterprise software, consumer technology, and digital health.

19. e2vc Fund III (Istanbul, Turkey) – Pre-Seed – 100 Million Euros

e2vc is Turkey's most internationally oriented pre-seed fund and one of a small number of Turkish venture vehicles that actively participates in the broader European startup ecosystem. Fund III deploys capital into pre-seed technology companies with a primary focus on B2B software and marketplace models with the potential to scale across Europe and the Middle East. Istanbul's position bridging Europe and the Gulf region creates a distinctive commercial geography for e2vc portfolio companies building in regulated or relationship-intensive sectors.

20. Epidarex Capital Fund IV (Edinburgh, UK) – Seed/A – 122 Million Euros

Epidarex Capital is a life sciences fund based in Edinburgh with a deep focus on translational science: the process of moving academic discoveries in medicine, biotech, and medical devices from laboratory research toward commercial development. The fund works closely with Scottish and broader UK university technology transfer offices and is a systematic first institutional capital partner for spinouts emerging from leading research institutions including the University of Edinburgh, the University of Glasgow, and several London-based research hospitals.

Key Takeaways

|

BioInnovation

Institute's 735 million euro capital base backed by the Novo Nordisk

Foundation makes it the most powerful life sciences pre-seed vehicle in the

Nordic region and possibly all of Europe. |

|

PFR

Ventures-backed Polish funds are creating a new cohort of institutional

early-stage investors in Warsaw, accelerating the professionalization of the

Polish startup ecosystem. |

|

Translational

science funds like Epidarex Capital in Edinburgh are bridging the persistent

gap between academic research and commercial company formation across the UK. |

|

Paris-based

funds like Clover and Daphni Blue reflect the maturation of the French

startup ecosystem, which has emerged as Europe's second most important

venture hub after London. |

🚀 1000+ Angel Investors

A massive, curated list of angel investors actively funding early-stage startups.

Whether you're building your first product or scaling fast — this is your shortcut to reaching the right backers.

- ✔️ 1000+ verified angel investors

- ✔️ Early-stage & seed-focused

- ✔️ Save months of investor research

- ✔️ Built for founders, freelancers & creators

Limited-time access. Get in front of investors before everyone else does.

Section 4: Funds 21 to 30 – Climate, FoodTech, and Growth Capital

The third cohort of ten funds is where the climate technology and FoodTech thesis becomes most concentrated. Berlin and London continue to anchor the group, but Copenhagen, Amsterdam, and Stockholm also feature. This cohort also includes some of the largest vehicles on the list by capital under management, reflecting the significant scaling of growth-stage European VC over the past several years.

21. Expedition Growth Capital (London, UK) – Growth – 323 Million Euros

Expedition is a London-based growth equity fund backing European technology companies that have achieved meaningful revenue and are building toward market leadership. With 323 million euros, Expedition is one of the larger vehicles on this list and operates in the growth stage where European capital has historically been thinnest relative to demand. The fund's thesis is that European technology companies are systematically undervalued at the growth stage compared to US counterparts and that a concentrated portfolio of fifteen to twenty exceptional businesses will generate superior returns.

22. Firgun Ventures I (London, UK) – Series A/B – 70 Million Euros

Firgun Ventures is a London-based Series A and B fund with a focus on Israeli and European technology companies. The fund's name reflects its founding team's Israeli heritage and commitment to backing founders who demonstrate deep customer empathy. Firgun invests in enterprise software, cybersecurity, and developer tools, sectors where Israeli and European technical talent has historically produced globally competitive companies.

23. FoodLabs Fund (Berlin, Germany) – Pre-Seed – 105 Million Euros

FoodLabs is Europe's most dedicated and thesis-driven FoodTech investor, and the third fund closed in December 2025 at 105 million euros represents both a validation of its approach and a significant expansion of its capital base. The Berlin-based fund backs startups across three core pillars: sustainable agriculture, food security, and human health nutrition. Agriculture accounts for roughly a third of global greenhouse gas emissions, and FoodLabs positions its investments as essential infrastructure for addressing both climate change and food system fragility simultaneously. Current and recent portfolio companies include Formo, which makes animal-free dairy using precision fermentation; Klim, a regenerative agriculture platform connecting farmers with carbon markets; Infinite Roots, which develops mycelium-based meat alternatives; and Voltrac, a Spanish startup building autonomous electric tractors for small-scale farmers.

24. Footprint Fund I (Copenhagen, Denmark) – Seed/A – 76 Million Euros

Footprint is a Copenhagen-based climate technology fund with a specific mandate to back companies reducing the carbon footprint of industrial and commercial operations. Denmark's status as a global leader in renewable energy and clean industrial design gives Footprint access to an exceptional ecosystem of technical co-founders and potential corporate customers. The fund's thesis is grounded in industrial decarbonization rather than consumer-facing green products, reflecting a conviction that the largest emissions reductions will come from transforming industrial processes rather than changing consumer behavior.

25. Future Energy Ventures II (Berlin, Germany) – Series A/B – 205 Million Euros

Future Energy Ventures is the corporate venture arm of E.ON, one of Europe's largest energy infrastructure companies, and invests from a dedicated fund structure rather than a traditional balance sheet. The second fund backs startups across energy storage, smart grid technology, electrification of transport, and digital energy management. FEV's corporate relationship with E.ON gives portfolio companies an unmatched pathway to commercial pilot programs, utility partnerships, and scaled deployment across E.ON's extensive European infrastructure network.

26. Future Tech Poland (Warsaw, Poland) – Seed/B – 350 Million Euros

Future Tech Poland is the largest Polish venture fund on this list and represents the emergence of genuine institutional scale in the Warsaw ecosystem. With 350 million euros, the fund deploys capital across the full early and growth stage spectrum from seed through Series B, giving it the flexibility to lead rounds at multiple stages and maintain meaningful ownership as portfolio companies scale. The fund is backed by the Polish Development Fund and focuses on deep tech, artificial intelligence, and B2B software companies with strong potential for international expansion from a Polish technical base.

27. HenQ VC (Amsterdam, Netherlands) – Seed – 67.6 Million Euros

HenQ is a founder-run Amsterdam seed fund with a reputation for being one of the most accessible and operationally useful early-stage investors in the Dutch ecosystem. The fund backs B2B software and marketplace companies, and its network of operator limited partners provides portfolio founders with direct access to commercial and hiring support. The Netherlands has developed a particularly strong B2B SaaS ecosystem over the past decade, and HenQ has been a consistent early backer of companies that have gone on to raise significant Series A and B rounds from European and US investors.

28. Indico Capital Partners III (Lisbon, Portugal) – Seed/A – 125 Million Euros

Indico Capital Partners is Lisbon's leading dedicated venture fund and has been the most consistent institutional backer of Portuguese technology companies over the past decade. Fund III continues the firm's generalist early-stage approach with a particular emphasis on B2B software, fintech, and digital health companies that can use Lisbon as a base for global expansion. Indico has built an exceptional track record of connecting its portfolio companies with US venture investors at Series A, with several portfolio companies having raised follow-on rounds from top-tier American firms.

29. Inception Fund I (Stockholm, Sweden) – Pre-Seed – 21 Million Euros

Inception is a Stockholm pre-seed fund that backs the earliest-stage technology companies in the Swedish ecosystem. Sweden has an extraordinary track record of producing globally significant technology companies relative to its population, and Inception positions itself as a first institutional capital partner for the founders who will build the next generation of Swedish success stories. The fund writes checks between 200,000 and 600,000 euros and provides intensive operational support through a structured accelerator program.

30. Investing For Purpose (IFP) (Athens, Greece) – Pre-Seed – 25.4 Million Euros

IFP is a remarkable institution: a dedicated impact pre-seed fund based in Athens, bringing institutional early-stage capital to the Greek startup ecosystem for what is effectively the first time. The fund backs founders whose companies generate measurable social, environmental, or community value alongside financial returns, with specific interest in climate adaptation, education technology, and social services innovation. Greece's startup ecosystem has developed rapidly over the past five years, and IFP's presence creates a new institutional anchor for the community.

Key Takeaways

|

FoodLabs

Fund III, closed at 105 million euros in December 2025, demonstrates that

specialized foodtech and agritech investing has reached institutional scale

in Europe. |

|

Future

Energy Ventures II benefits from E.ON's corporate relationship to offer

portfolio companies direct pathways to commercial deployment across major

European energy infrastructure. |

|

Future

Tech Poland at 350 million euros is the largest Polish VC fund in history and

reflects the ecosystem's rapid maturation into genuine institutional venture

capital. |

|

Athens-based

IFP represents the arrival of impact investing infrastructure in Southern

Europe's most underserved startup ecosystem. |

Section 5: Funds 31 to 40 – Deep Tech, Defence, and Benelux Innovation

The fourth group of ten funds is characterized by concentration in the Benelux and Iberian Peninsula markets, alongside several highly distinctive thesis-driven vehicles with specific mandates in deep tech, semiconductor hardware, and defence. This cohort also includes two Spanish funds, reflecting Madrid's emergence as a genuine venture capital hub, and two Athens-based vehicles reflecting the continued development of the Greek startup ecosystem.

31. KBC Start it Fund I (Brussels, Belgium) – Pre-Seed – 100 Million Euros

KBC Start it Fund is a corporate venture initiative from KBC Group, one of Belgium's largest banking and insurance conglomerates. The fund deploys pre-seed capital into Belgian technology startups with particular interest in fintech, insurtech, and digital services companies where KBC's corporate distribution network and financial infrastructure can provide portfolio companies with immediate commercial advantage. Belgium's position at the heart of the European institutional landscape makes it a particularly valuable base for financial technology companies targeting pan-European enterprise customers.

32. Keen Venture Partners II (Amsterdam, Netherlands) – Seed/B – 150 Million Euros

Keen Venture Partners is a well-established Amsterdam fund with the flexibility to deploy capital across a wide stage range from seed through Series B. The fund's generalist approach allows it to follow companies across multiple rounds and maintain ownership concentration in its best performers. Keen's portfolio spans B2B software, marketplace technology, and developer infrastructure, and the fund has built a strong reputation for being operationally useful to portfolio companies navigating European market complexity.

33. Kibo Ventures Fund IV (Madrid, Spain) – Seed/A – 100 Million Euros

Kibo Ventures is Madrid's leading seed and Series A fund and has been the most consistent institutional backer of Spanish technology companies over the past decade. Fund IV continues a thesis built around backing Spanish founders with genuine product innovation and the ambition to build global companies from a Madrid base. Spain's rapid development as a European tech hub, driven by strong engineering universities, competitive living costs, and an increasingly active angel and accelerator ecosystem, has created a much stronger deal pipeline for Kibo than existed when the fund was founded.

34. Make Sense Seed (Paris, France) – Pre-Seed – 25 Million Euros

Make Sense Seed is a Paris-based pre-seed fund deeply connected to the Make Sense social entrepreneurship community, one of the largest networks of purpose-driven innovators in France. The fund backs founders whose companies address social and environmental challenges through scalable technology, combining impact orientation with commercial discipline. Make Sense's community network provides portfolio founders with extraordinary access to talent, advisers, and potential customers who are motivated by the same values that underpin the fund's investment thesis.

35. Metavallon Brain Gain Fund (Athens, Greece) – Pre-Seed – 5.8 Million Euros

Metavallon Brain Gain Fund is an Athens-based micro-vehicle with a specific mandate to attract Greek technical talent back to Greece from the diaspora, particularly engineers and scientists who have built careers in the United States, United Kingdom, and Germany. The fund's thesis is that returning diaspora founders bring a unique combination of international network, technical sophistication, and cultural knowledge of the Greek market that makes them exceptional company builders. The fund is small but strategically significant as part of Greece's effort to reverse the brain drain of the post-2008 recession era.

36. Mission Pre-Seed Fund (Barcelona, Spain) – Pre-Seed – 35 Million Euros

Mission Pre-Seed Fund operates from Barcelona with a focus on backing the earliest-stage founders in the Spanish and Catalan startup ecosystems. Barcelona has developed a distinctive startup culture built around strong design talent, consumer technology, and digital health, and Mission positions itself as the natural first institutional partner for founders emerging from that environment. The fund places particular emphasis on backing founders from diverse backgrounds and has been an active participant in the Barcelona startup community's efforts to develop more inclusive funding pathways.

37. Nextgen Ventures (Ede, Netherlands) – Seed/A – 28.5 Million Euros

Nextgen Ventures is a Netherlands-based fund focused on university spinout investing, working closely with Wageningen University, one of the world's leading institutions for life sciences and agritech research. Based in Ede, near Wageningen's campus, the fund invests in early-stage companies commercializing research in food science, plant biology, environmental technology, and bioeconomy applications. Wageningen's global reputation as the premier agricultural research university gives Nextgen access to a deal pipeline with exceptional scientific depth.

38. Oyster Bay VC II (Berlin, Germany) – Seed/A – 100 Million Euros

Oyster Bay VC is a Berlin-based fund that invests in startups redefining work, education, and productivity in the era of artificial intelligence. The fund's second vehicle builds on a thesis that the transition to AI-augmented work will create enormous opportunities for software companies that help individuals and organizations adapt their skills, workflows, and organizational structures. Berlin's deep pool of product talent, engineering graduates, and international founders makes it an ideal sourcing ground for this thesis.

39. PROTOTYPE Capital III (Berlin, Germany) – Pre-Seed – 15 Million Euros

PROTOTYPE Capital is a Berlin-based pre-seed fund focused on Europe's semiconductor and hardware resurgence, backing founders building deep industrial technology, embedded systems, and physical computing infrastructure. The fund's third vehicle reflects a growing conviction that Europe's strategic vulnerabilities in semiconductor supply chains and industrial hardware will drive a sustained investment cycle in companies that can reduce dependence on Asian manufacturing. PROTOTYPE writes very early checks and invests heavily in technical due diligence.

40. PSV Hafnium (Copenhagen, Denmark) – Pre-Seed – 60 Million Euros

PSV Hafnium is a Copenhagen-based pre-seed fund with a focus on deep science ventures emerging from Danish and Nordic research institutions. Named after the chemical element hafnium, the fund reflects a scientific sensibility in its investment approach, backing founders who are solving fundamental technological challenges rather than applying existing technology to established markets. Copenhagen's extraordinary concentration of life sciences research, materials science expertise, and quantum computing talent gives PSV Hafnium access to a deal pipeline that few other European pre-seed funds can match.

Key Takeaways

|

Benelux

funds including KBC Start it, Keen Venture Partners, and Nextgen Ventures

demonstrate the Netherlands and Belgium's deepening institutional VC

infrastructure. |

|

Madrid

and Barcelona have both developed dedicated institutional seed funds,

reflecting Spain's emergence as a genuine European startup hub. |

|

PROTOTYPE

Capital's semiconductor and hardware thesis reflects growing European anxiety

about strategic dependencies in critical technology supply chains. |

|

Copenhagen's

deep science ecosystem supports multiple institutional pre-seed vehicles with

complementary but distinct theses. |

🚀 1000+ Angel Investors

A massive, curated list of angel investors actively funding early-stage startups.

Whether you're building your first product or scaling fast — this is your shortcut to reaching the right backers.

- ✔️ 1000+ verified angel investors

- ✔️ Early-stage & seed-focused

- ✔️ Save months of investor research

- ✔️ Built for founders, freelancers & creators

Limited-time access. Get in front of investors before everyone else does.

Section 6: Funds 41 to 50 – Impact, Defence, and the Final Cohort

The final ten funds on this list span a notably broad range of mandates, from dedicated impact and social venture vehicles to defence and dual-use technology funds, from consumer and fintech-focused investors to B2B software specialists. Amsterdam, Berlin, Copenhagen, and London all feature in this cohort, alongside Milan and Barcelona. Several of these funds are first-time vehicles managed by emerging managers with distinctive backgrounds in operating companies, non-profits, and government.

41. Rubio Impact Ventures III (Amsterdam, Netherlands) – Series A/B – 70 Million Euros

Rubio Impact Ventures is one of Europe's most established impact-focused venture funds, with a track record across three successive vehicles and a consistent strategy of backing companies that generate measurable positive outcomes in climate, social equity, health access, and education. The third fund deploys at Series A and B, supporting companies that have demonstrated early commercial traction and are now ready to scale their impact alongside their revenue. Rubio's investment approach integrates impact measurement into portfolio management rather than treating it as a reporting exercise separate from core investment decisions.

42. Seed + Speed Ventures III (Berlin, Germany) – Pre-Seed – 50 Million Euros

Seed + Speed is a Berlin-based pre-seed fund that combines traditional equity investment with an accelerator operating model, providing founders with intensive early-stage support alongside capital. The fund's third vehicle focuses on B2B software, marketplace technology, and climate-adjacent businesses where Berlin's combination of technical talent, founder culture, and corporate access provides a genuine competitive advantage for early-stage companies.

43. Ship2B Ventures II (Barcelona, Spain) – Seed/A – 55 Million Euros

Ship2B Ventures is Barcelona's leading impact-focused venture fund, backing founders whose companies address social and environmental challenges through market-based solutions. The fund sits at the intersection of social innovation and commercial venture capital, seeking companies that can achieve significant scale while maintaining measurable social impact. Barcelona's strong tradition of cooperative and social enterprise provides Ship2B with an unusually rich sourcing environment for founders with both commercial ambition and mission orientation.

44. Sofinnova Capital XI (Paris, France) – Seed/A – 500 Million Euros (actual close: 650 million euros)

Sofinnova Capital XI is the flagship fund from Sofinnova Partners, Europe's oldest and most distinguished life sciences venture firm, founded in Paris in 1972. The eleventh fund closed at 650 million euros in November 2025, significantly exceeding its initial target, and attracted commitments from sovereign wealth funds, leading pharmaceutical companies, insurance groups, and family offices across Europe, North America, Asia, and the Middle East. The fund backs early-stage biopharmaceutical and medical technology companies addressing urgent unmet clinical needs across Europe and the United States. Early portfolio investments include Actithera, a radiopharmaceuticals startup, and Elevara Medicines, a developer of treatments for inflammatory diseases. Sofinnova Partners manages over four billion euros in assets across its platform and has backed more than 500 companies since inception, making it the most experienced life sciences venture investor in Europe by almost any measure.

45. Step Fund I (Milan, Italy) – Pre-Seed – 30 Million Euros

Step Fund I is a Milan-based pre-seed vehicle representing the growing confidence of the Italian startup ecosystem. Italy has historically been underrepresented in European venture capital relative to the size of its economy, and Step Fund I is part of a new generation of Italian institutional funds addressing that gap. The fund backs technology founders in B2B software, fintech, and climate technology, with particular emphasis on companies that can leverage Italy's deep manufacturing and industrial heritage as a commercial foundation.

46. TIN Capital V (Amsterdam, Netherlands) – Series A/B – 200 Million Euros

TIN Capital is a well-established Amsterdam fund deploying capital at Series A and B into European technology companies. The fifth fund reflects a strong track record across four prior vehicles and a team that has developed deep expertise in backing Dutch and broader Benelux companies through their most important commercial scaling phases. TIN's portfolio historically concentrates in enterprise software, data infrastructure, and marketplace technology, sectors where Amsterdam's exceptional talent pool and proximity to major European corporate headquarters creates sustained deal flow.

47. Twin Track Ventures (London, UK) – Pre-Seed – 5.5 Million Euros

Twin Track Ventures is one of the most distinctive funds on this list. Founded by Nicola Sinclair, a British air force veteran, Twin Track is a London-based pre-seed vehicle with an exclusive mandate to back dual-use technology companies: startups whose products and services are designed to succeed commercially while also serving defence needs. The fund's approach reflects a growing conviction across the European investment community that the traditional separation between civilian and defence technology is dissolving, and that the best dual-use companies will be able to access both commercial enterprise markets and government procurement simultaneously. Twin Track has already secured commitments from institutional LPs and is tracking toward a full target of ten million pounds by 2026.

48. U2V Fund I (Berlin, Germany) – Pre-Seed – 60 Million Euros

U2V Fund I is a Berlin-based university-to-venture specialist fund, investing in spinouts and technology transfers emerging from Germany's leading technical universities including TU Berlin, TU Munich, and KIT Karlsruhe. The fund addresses a critical structural gap in the German ecosystem: while Germany produces world-class academic research across engineering, materials science, and computer science, the translation of that research into commercial companies has historically been slower and less systematic than in the UK, US, or Israel. U2V is designed to accelerate that translation by providing the earliest institutional capital alongside strategic company-building support.

49. Unconventional Ventures II (Copenhagen, Denmark) – Pre-Seed – 52 Million Euros

Unconventional Ventures is a Copenhagen-based fund with a distinctive mandate to back founders from underrepresented groups, including women, immigrants, older founders, and entrepreneurs with disabilities. The fund's second vehicle builds on a first fund that demonstrated strong financial performance alongside its inclusion goals, providing evidence that expanding the founder pipeline beyond the traditional demographic produces genuinely better investment returns. Denmark's progressive institutional culture and strong public-private partnership infrastructure makes Copenhagen an exceptional base for this kind of mandate.

50. Vendep Capital IV (Amsterdam, Netherlands) – Seed/A

Vendep Capital is a long-standing Amsterdam seed and Series A fund with a strong track record across four successive vehicles. The fourth fund continues a consistent strategy of backing B2B software companies in the Netherlands and broader Benelux region, with particular strength in SaaS companies serving enterprise and mid-market customers. Vendep's operator network of limited partners provides portfolio companies with immediate access to commercial relationships across major Dutch and international enterprise organizations.

Key Takeaways

|

Sofinnova

Capital XI at 650 million euros is the largest dedicated life sciences

early-stage fund in Europe and its oversubscription reflects sustained

institutional confidence in European biotech. |

|

Twin

Track Ventures represents the formalization of dual-use technology investing

as a distinct VC category, anticipating the convergence of commercial and

defence technology markets. |

|

Inclusion-focused

funds like Unconventional Ventures II are proving that expanding the founder

pipeline produces superior financial returns alongside social impact. |

|

Amsterdam

continues to generate successive institutional-scale vehicles across multiple

stages, confirming its position as one of Europe's most consistent venture

ecosystems. |

Section 7: Sector Comparison – Investment Stage and Fund Size by Sector

The table below provides a structured comparison of the six sectors covered across the 50 funds on this list, showing typical investment stage, representative fund size, geographic concentration, and key examples from the cohort. This is designed to help founders quickly identify which funds are most likely to be relevant to their stage and sector.

|

Sector |

Typical

Stage |

Avg Fund

Size |

Key

Geographies |

Representative

Funds |

|

Technology / B2B |

Pre-Seed to Series A |

80-250M EUR |

London, Berlin, Amsterdam, Warsaw |

6 Degrees Capital III, Daphni Blue, Future Tech Poland |

|

Impact / Social |

Pre-Seed to Series B |

25-70M EUR |

Amsterdam, Munich, Copenhagen, Barcelona |

Ananda Impact V, Rubio Impact III, Ship2B Ventures II |

|

Life Sciences / Biotech |

Pre-Seed to Seed/A |

60-650M EUR |

Paris, Copenhagen, Edinburgh, Luxembourg |

Sofinnova Capital XI, BioInnovation Institute, Epidarex IV |

|

Climate / FoodTech |

Pre-Seed to Series B |

70-350M EUR |

Berlin, Copenhagen, Amsterdam, Lisbon |

FoodLabs Fund, Footprint Fund I, Future Energy Ventures II |

|

Fintech / Consumer |

Pre-Seed to Series A |

21-150M EUR |

London, Amsterdam, Vilnius, Dublin |

Cocoa Ventures II, Vendep Capital IV, Aniel Capital |

|

Deep Tech / Defence |

Pre-Seed to Series A |

15-100M EUR |

Berlin, London, Luxembourg, Copenhagen |

PROTOTYPE Capital III, Twin Track Ventures, Balnord I |

The table above reveals several important patterns. Life Sciences and Biotech has by far the widest fund size range on the list, driven by the outlier scale of Sofinnova Capital XI and BioInnovation Institute, both of which operate at the top end of what is possible in European early-stage investing. At the other extreme, Impact and Deep Tech funds tend to be smaller and more concentrated, reflecting both the higher risk tolerance required for novel thesis-driven investing and the more limited number of institutional limited partners with specific mandates in those sectors.

Climate and FoodTech funds show the strongest mid-range clustering, with several vehicles in the 70 to 350 million euro range, reflecting the maturation of climate investing as an institutional asset class in Europe. Technology and B2B remains the most geographically distributed sector, with credible institutional funds now operating across the UK, Germany, Netherlands, France, Poland, Portugal, and the Nordics simultaneously.

Section 8: Notable Startups Backed by These Funds

The funds in this guide are not abstract capital allocation vehicles. They are backing real companies building real products. The following startups offer a snapshot of the kind of innovation that active European pre-seed and seed investment is producing in 2025 and 2026.

Formo (Berlin, Germany) – Precision Fermentation Dairy

Formo is a Berlin-based biotech company that uses precision fermentation to produce animal-free dairy proteins that can be used in cheese, yogurt, and other dairy products. The company is backed by FoodLabs and represents one of the most technically sophisticated approaches to alternative protein production in Europe. Formo's technology uses engineered microorganisms to produce casein and whey proteins that are molecularly identical to those produced by cows, enabling the creation of dairy products with the same taste and texture profiles as conventional dairy but without any animal involvement.

Klim (Berlin, Germany) – Regenerative Agriculture Platform

Klim is a Berlin-based platform that connects European farmers with carbon credit buyers and provides the data infrastructure and agronomic support farmers need to transition to regenerative agricultural practices. The company is backed by FoodLabs and addresses one of the most critical bottlenecks in European agricultural decarbonization: the gap between farmers who want to adopt more sustainable practices and the market infrastructure needed to reward them financially for doing so.

Voltrac (Spain) – Autonomous Electric Tractors

Voltrac is a Spanish agritech startup that develops autonomous electric tractor platforms designed specifically for small-scale and family farms that cannot economically justify conventional large-scale agricultural automation. The company received investment from FoodLabs in 2025 and has positioned itself at the intersection of the agricultural labor shortage, the transition to electric farm equipment, and the broader push to make precision agriculture accessible to farmers operating at smaller scales.

Actithera (Europe) – Radiopharmaceuticals

Actithera is one of the early portfolio companies from Sofinnova Capital XI and works in the growing field of radiopharmaceuticals, which uses radioactive isotopes attached to targeting molecules to deliver radiation directly to cancer cells while minimizing damage to surrounding healthy tissue. The field has attracted enormous interest from major pharmaceutical companies following the success of Novartis's Lutathera product, and Actithera is developing next-generation approaches that improve precision and broaden the range of cancers that can be treated.

Synuca Therapeutics (Aarhus, Denmark) – Neuropharmacology

Synuca Therapeutics is a Danish biotech company that emerged from the BioInnovation Institute's Venture House cohort in 2026 and is backed by a combination of BII and the Lundbeck Foundation. The company is developing novel therapeutic approaches to neurological and psychiatric conditions, drawing on Denmark's extraordinary concentration of neuroscience expertise concentrated around Aarhus University and the Copenhagen University Hospital network. Synuca's funding marks the first deployment from BII's new innovation partnership with Lundbeckfonden.

Infinite Roots (Hamburg, Germany) – Mycelium-Based Alternative Proteins

Infinite Roots, formerly known as Mushlabs, is a Hamburg-based alternative protein company that uses mycelium -- the root-like network of fungi -- as the primary ingredient for meat alternatives. The company raised 58 million euros in a Series B round led by Dr. Hans Riegel Holding with participation from FoodLabs, Redalpine, and several strategic investors. Infinite Roots's technology produces a high-protein, high-fiber ingredient with a naturally meat-like texture that can be used as a direct replacement in burgers, nuggets, and other processed meat formats.

Key Takeaways

|

Precision

fermentation companies like Formo represent the most technically advanced

segment of European alternative protein investing and are producing products

that can directly substitute for conventional animal-derived ingredients. |

|

Agritech

companies like Klim and Voltrac are addressing the practical commercial and

operational challenges that prevent sustainable agriculture adoption at

scale. |

|

Radiopharmaceuticals

represent one of the fastest-growing segments of European biotech investment,

driven by proven clinical validation and strong pharmaceutical company

acquisition interest. |

|

BioInnovation

Institute's portfolio companies are raising follow-on capital from

third-party investors at a five-to-one ratio relative to BII's own

investment, confirming the quality of the deal flow generated by the

incubator model. |

Section 9: Six Sector Deep Dives – Trends Shaping European VC in 2026

Technology and B2B: The AI Enterprise Transition

The dominant theme across European B2B technology investing in 2026 is the transition from AI experimentation to AI implementation. Enterprise software companies that were pitching artificial intelligence as a roadmap item two years ago are now under pressure to demonstrate deployed production systems with measurable outcomes. This has created a sharp divide between companies that built their product architectures with AI-native assumptions and those that are retrofitting legacy codebases. European B2B investors are concentrating capital in the former category, backing companies where the AI integration creates genuine competitive moat rather than cosmetic enhancement.

The sector is also seeing a significant shift in buyer behavior across European enterprise customers. German, French, and Nordic industrial companies that were historically skeptical of cloud software are now actively deploying AI-augmented tools for manufacturing optimization, supply chain management, and quality control. This is creating commercial opportunities for enterprise software companies that would have been difficult to access three years ago.

Impact and Social: From Measurement to Accountability

Impact investing in Europe has passed through a critical maturation phase over the past three years. The first generation of impact funds faced persistent skepticism about whether impact measurement was credible, consistent, and commercially relevant. The second and third generation funds represented on this list -- including Ananda, Rubio, and Ship2B -- have addressed this skepticism by building sophisticated quantitative impact measurement frameworks into their investment processes and demonstrating that they can achieve competitive financial returns alongside measurable social outcomes.

The European regulatory environment has also accelerated this maturation. The EU's Sustainable Finance Disclosure Regulation and the emerging corporate sustainability reporting standards are creating mandatory frameworks that make impact measurement a compliance requirement for institutional investors rather than an optional extra. This is bringing mainstream capital toward funds that have already built the infrastructure to meet those requirements.

Life Sciences and Biotech: Europe's Scientific Advantages

European life sciences venture capital is experiencing one of its strongest cycles in a generation. The combination of world-class academic research institutions, a large and sophisticated pool of scientific talent, increasingly active translational infrastructure through institutions like BioInnovation Institute, and strong institutional demand from sovereign wealth funds and pharmaceutical company venture arms has created exceptional conditions for fund formation and company creation.

The radiopharmaceuticals and cell therapy sectors are particularly active, driven by growing clinical validation data and strong interest from major pharmaceutical acquirers. Europe's academic medical centres and biobank infrastructure provide European life sciences startups with access to patient data and clinical trial infrastructure that is increasingly difficult to access in the United States due to regulatory complexity and cost.

Climate and FoodTech: Urgency Drives Innovation

Climate tech captured approximately 22 percent of European venture capital in 2025, a proportion that has grown consistently over the preceding five years. The FoodTech subset of climate investing has benefited both from the climate urgency narrative and from growing consumer and institutional buyer interest in sustainable food systems. The funds on this list that focus on climate and food -- FoodLabs, Footprint, Future Energy Ventures -- are deploying capital into companies across the full spectrum of the food system, from farm-level efficiency tools to alternative protein production to renewable energy infrastructure for food processing.

Fintech and Consumer: Regulation as Opportunity

European fintech has entered a more mature phase after the extraordinary growth of the 2018 to 2021 period. The consumer neobank wave has consolidated around a small number of scaled winners including Revolut, N26, and Monzo, leaving the market more concentrated at the top. New fintech investment is concentrating in B2B financial infrastructure, embedded finance, and regulatory technology -- areas where European regulatory complexity creates durable competitive moats for companies that invest in deep compliance and legal infrastructure. Lithuania's fintech licensing environment and Ireland's regulatory framework continue to attract international fintech founders seeking European market entry.

Deep Tech and Defence: Europe's Strategic Imperative

Defence and dual-use technology has emerged as one of the most rapidly growing segments of European venture capital over the past two years, driven by geopolitical pressure following Russia's invasion of Ukraine and a growing consensus that European strategic autonomy requires a much more robust domestic defence technology industrial base. European defence tech startups raised 8.7 billion dollars in 2025, a figure that would have seemed implausible just five years earlier when most European VC funds maintained explicit mandates against investing in defence-related companies. The funds on this list that operate in this space -- Twin Track Ventures, Balnord, PROTOTYPE Capital -- represent the institutionalization of European defence tech investing.

Key Takeaways

|

AI

implementation in European enterprise software has shifted from roadmap

aspiration to commercial requirement, accelerating investment in AI-native

B2B companies. |

|

Impact

investing has matured from a niche to a mainstream institutional category,

driven by EU regulatory requirements and demonstrated competitive financial

returns. |

|

European

life sciences is in an exceptional cycle, driven by strong academic

infrastructure, growing translational investment, and active pharmaceutical

acquirer interest. |

|

Defence

and dual-use technology has gone from a restricted investment category to one

of the fastest-growing segments of European VC in just three years. |

🚀 1000+ Angel Investors

A massive, curated list of angel investors actively funding early-stage startups.

Whether you're building your first product or scaling fast — this is your shortcut to reaching the right backers.

- ✔️ 1000+ verified angel investors

- ✔️ Early-stage & seed-focused

- ✔️ Save months of investor research

- ✔️ Built for founders, freelancers & creators

Limited-time access. Get in front of investors before everyone else does.

Section 10: How Founders Should Approach These Funds

Understanding which funds are active is only the first step. Knowing how to approach them effectively, how to qualify fit before reaching out, and what signals experienced fund managers are looking for in early-stage companies is equally important. The following guidance is drawn from publicly available information about the investment processes of the funds on this list.

Stage Matching: The Most Important Filter

The single most common mistake founders make when approaching venture capital funds is mismatching their company's stage to the fund's mandate. The funds on this list span a range from pre-seed vehicles writing 200,000 euro initial checks all the way to growth funds deploying 20 to 50 million euro rounds. Approaching a growth fund with a pre-revenue prototype is as much a mismatch as approaching a pre-seed fund with a company already generating five million euros in annual revenue. Founders should review each fund's portfolio carefully before reaching out, looking specifically at the stage at which the fund made its first investment in portfolio companies rather than the stage at which those companies are operating today.

Geographic and Sector Fit

Several funds on this list have explicit geographic mandates. Aniel Capital focuses on the Baltic states. Armilar Venture Partners prioritizes Portuguese founders with Atlantic market access. Betacluster and Cofounder VC are specifically oriented around the Polish ecosystem. Approaching a geographically focused fund as a founder who is not based in or deeply connected to that geography is unlikely to be productive regardless of the quality of the business.

Sector fit is equally important. FoodLabs will not invest in a SaaS analytics company regardless of how compelling the metrics are. BioInnovation Institute funds life science and deep tech research-based startups. Twin Track Ventures requires genuine dual-use technology applications, not commercial businesses with speculative defence ambitions. Founders should read each fund's investment thesis carefully and be honest with themselves about whether their company genuinely fits that thesis.

What European Fund Managers Look For

Across the funds on this list, a consistent set of qualities emerges from publicly available information about what investors find compelling. The first is founder conviction: a deep, evidence-based belief in the problem being solved and the approach being taken, combined with genuine resilience to adversity and an ability to maintain clear strategic thinking under pressure. The second is market understanding: a granular, specific knowledge of the customer, their decision-making process, their budget constraints, and their alternative solutions, that goes well beyond general market size estimates.

The third quality is evidence of learning velocity: the ability to take a small amount of early capital and generate a disproportionate amount of insight about what works and what does not. Early-stage investors are not buying a guaranteed outcome; they are buying the founder's ability to navigate from an uncertain starting point to a much better strategic position over twelve to eighteen months. Demonstrating that kind of learning velocity, even from non-fundraising activities like early customer conversations, product experiments, or competitive analysis, is one of the most compelling signals a pre-seed founder can provide.

Key Takeaways

|

Stage

matching is the most common and most consequential mistake founders make when

approaching VC funds: verify the stage of the fund's first portfolio

investments, not their current portfolio companies. |

|

Geographic

and sector fit mandates are non-negotiable for focused funds: research each

fund's thesis carefully before reaching out. |

|

European

early-stage investors consistently prioritize founder conviction, granular

market understanding, and demonstrated learning velocity over polished pitch

decks. |

|

The

fundraising process for European startups typically involves 80 to 150

investor conversations and takes six to nine months: starting the process

early and being systematic about pipeline management is essential. |

Conclusion: The European Venture Capital Opportunity in 2026

The 50 funds profiled in this guide represent something genuinely significant in the history of European venture capital. For the first time, the continent has a broad, geographically distributed, institutionally credible network of early-stage investors across every major sector of the modern economy. From pre-seed biotech incubation in Copenhagen to growth equity in London, from dual-use defence tech in the Baltic Sea region to FoodTech acceleration in Berlin, from social impact investing in Amsterdam to university spinout commercialization in Edinburgh, the European VC ecosystem has developed the infrastructure to support founders at every stage, in every sector, and from almost every country on the continent.

That does not mean the work is done. Europe still has a structural deficit of growth-stage capital relative to the United States. Regulatory fragmentation continues to create friction for startups building across multiple European markets simultaneously. Talent retention remains challenging in some technical domains where US compensation packages are dramatically higher. And the concentration of the very largest VC funds in a small number of major cities still means that founders who are not in London, Paris, or Berlin may face meaningfully higher fundraising friction than their counterparts in those hubs.

But the direction is clear, the momentum is real, and the quality of the funds now operating across the European ecosystem is higher than it has ever been. For founders building genuinely important companies, the capital is there. For investors seeking exposure to the European opportunity, the fund managers are there. The task now is to close the gap between European ambition and European commitment -- and the 50 funds in this guide are deploying capital in precisely that direction.