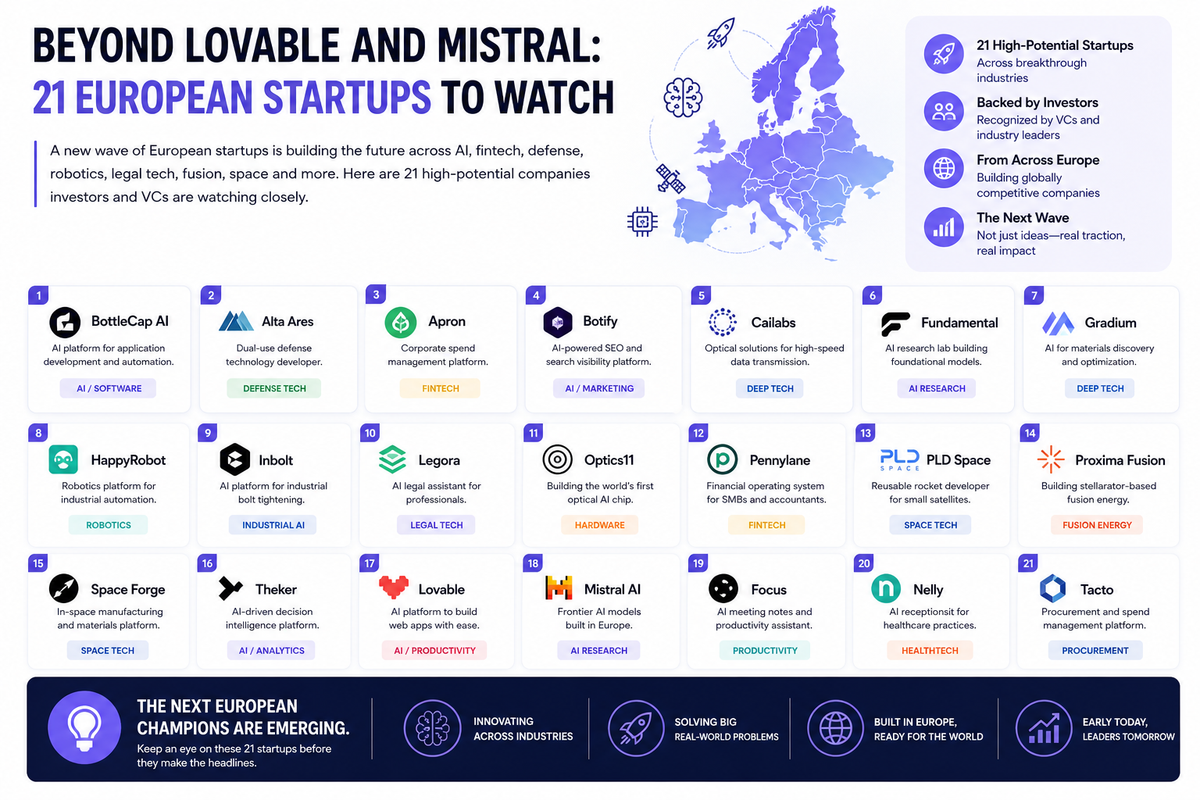

Beyond Lovable and Mistral: 21 European Startups Investors Are Quietly Watching

Europe's startup ecosystem runs far deeper than its most celebrated names. From Prague to Paris, Madrid to Munich, a new generation of founders is building companies that top investors believe deserve a much wider audience.

Introduction

Europe Has More Cards to Play Than Headlines Suggest

When conversations turn to European tech, two names tend to dominate: Lovable, the AI-powered software builder that recently hit nine digits in annual recurring revenue, and Mistral AI, the Paris-based lab that has emerged as one of the most credible challengers to OpenAI in the global model race. Both are extraordinary stories, and both deserve their recognition. But a continent of 44 countries and hundreds of millions of people produces rather more ambition than two companies can contain.

The startups that get written about most are often the ones that have already made it through the hardest early stages. They have the funding, the brand recognition, and the user numbers to generate their own gravity. Below that layer, however, sits a dense and remarkably serious cohort of companies that top-tier venture investors are tracking just as closely. Some are pre-launch. Some are already unicorns. Many are building in sectors that rarely attract the same breathless coverage as consumer AI apps but that carry arguably higher long-term stakes: nuclear fusion, counter-drone defense systems, in-space semiconductor manufacturing, AI infrastructure for enterprises, and photonics for satellite communication.

To surface this cohort, investors at some of Europe's most respected venture firms were each asked to recommend two startups: one from their own portfolio, and one outside it. The result is a list of 21 companies across different stages, sectors, and geographies that insiders believe deserve a much wider audience. What follows is not a ranking. It is a map of where serious people are placing serious bets — and why.

21 European startups by sector — how the investment landscape breaks down

AI infrastructure dominates the selection, accounting for more than a third of the 21 startups. Defense, space, and energy collectively represent the deep tech cluster that has attracted the most new capital in Europe since 2022.

The macro context

Why European Deep Tech Is Having Its Moment Right Now

Several forces have converged to make this an unusual period for European deep tech investment. The war in Ukraine delivered a blunt message to governments and militaries across the continent: decades of underinvestment in defense technology had left serious gaps in capability, and catching up would require both public funding and private innovation. Defense tech went from being a sector that many European VCs refused to touch for ethical or reputational reasons to one that has become a genuine priority. Counter-drone systems, fiber-optic sensing for subsea infrastructure, and satellite communications now attract capital that would previously have gone exclusively to software.

In parallel, Europe's push for strategic autonomy in space and energy has created openings for startups that might have struggled to find funding five years ago. Fusion energy, once the punchline of a decades-long joke, is now the subject of serious government-backed investment — Bavaria alone recently committed hundreds of millions of euros to a single fusion startup. These are not the investment patterns of a continent hedging its bets. They are the patterns of a continent that has decided it wants to win.

The AI layer running through all of this is equally significant. Unlike the first generation of European AI companies, which largely focused on applying existing models to specific verticals, the current cohort includes companies building their own foundation models, their own training data infrastructure, their own deployment tooling, and their own domain-specific AI agents. The talent is here, the research institutions are here, and increasingly, so is the capital. What has changed is the ambition.

Defense, security & physical infrastructure

Defense, Security, and Physical Infrastructure

Alta Ares

Recommended by Julien Codorniou, General Partner, 20VC

The rise of drone warfare has rewritten the rules of modern conflict faster than almost any military planner anticipated. Small, commercially available drones have proven devastating on battlefields from Ukraine to the Middle East, and the asymmetry of the threat is stark: defending against a drone that costs a few hundred dollars with a missile that costs hundreds of thousands is not a sustainable equation. Alta Ares is building AI-powered counter-drone interceptor systems specifically designed to address that cost imbalance, developing interceptors capable of detecting and neutralizing drone incursions at a fraction of the cost of conventional air defense.

As European militaries scramble to modernize and governments pour fresh funding into defense technology, Alta Ares sits at an intersection that is attracting significant attention from both the military establishment and the venture capital community. Defense tech has gone from pariah to priority in European venture circles, and this company is among the early beneficiaries of that structural shift. Julien Codorniou of 20VC singled it out as a lesser-known European AI startup that could define the next generation of affordable air defense systems.

Cailabs

Recommended by Flavia Levi, Investment Manager, Join Capital (investor)

The science of light has been central to technological progress for more than a century, but Cailabs is doing something with photonics that goes well beyond conventional optics. The Rennes-based startup has built a platform rooted in advanced photonics research, applying it to faster and more resilient data transmission for aerospace, defense, and industrial applications. Its technology is capable of handling conditions that would defeat conventional systems, making it particularly relevant for satellite communications and other demanding environments.

Backed by both public and private investors, Cailabs has secured a total of 57 million euros and is currently deploying fifty optical ground stations to meet surging demand for laser communications with satellites. As low-Earth orbit becomes more congested and data transmission requirements grow exponentially, the ability to build reliable optical ground infrastructure at scale becomes a genuine strategic advantage. Flavia Levi of Join Capital identified this as one of the most compelling deep tech bets in the European satellite communications space.

Optics11

Recommended by Flavia Levi, Investment Manager, Join Capital (investor)

Subsea infrastructure has become one of the most geopolitically sensitive categories of physical assets on the planet. Undersea cables carry the vast majority of global internet traffic, and energy grids increasingly depend on offshore infrastructure that is difficult to monitor and expensive to repair. Optics11 has developed fiber-optic sensing systems capable of monitoring equipment in underwater and similarly hostile conditions, providing early warning of disruption, damage, or interference before it becomes catastrophic.

The Amsterdam-based startup's technology has attracted the attention of the European Investment Bank, which has provided venture debt to support its work protecting subsea infrastructure. Its potential applications span offshore wind farms, transatlantic data cables, and energy grid monitoring. Flavia Levi of Join Capital views Optics11 as a company building essential defensive infrastructure for the physical layer of the digital economy — a category that geopolitical developments have made urgently important.

AI infrastructure, foundation models & data

AI Infrastructure, Foundation Models, and the Data Layer

BottleCap AI

Recommended by Julien Codorniou, General Partner, 20VC (investor)

The name is deliberately cheeky, a reference to a running internet joke about Europeans and bottle caps. But there is nothing playful about the pedigree behind BottleCap AI. The Prague-based startup was co-founded by a trio that includes an entrepreneur who previously sold his VR company Beat Games to Meta in 2019 and two experienced AI researchers. That combination of commercial track record and technical depth is exactly what investors look for when a startup announces it intends to build its own foundation models.

BottleCap has adopted a dual-track strategy: building efficiency-focused foundational large language models while simultaneously releasing consumer and enterprise applications built on top of them. Its first public product is Pulse, an AI-powered news application available on iOS. The logic is sound — building proprietary models without a distribution strategy is a capital-intensive gamble; building applications on someone else's models creates a dependency. BottleCap is trying to do both at once, making it one of the more ambitious and differentiated lesser-known European AI startups in the current cycle.

Fundamental

Recommended by Jonathan Userovici, General Partner, Headline (investor)

For all the noise around large language models, the enterprise data problem has remained stubbornly unsolved. Most large organizations are sitting on vast repositories of structured and unstructured data that are extremely difficult to query, cross-reference, and draw meaningful insights from using conventional tools. Fundamental's foundation model, Nexus, is specifically designed to change that, helping enterprises extract actionable intelligence from the kind of heterogeneous, large-scale datasets that defeat general-purpose LLMs.

The company emerged from stealth in February following a remarkable debut: a 255 million dollar Series A that valued it at 1.4 billion dollars before it had publicly launched. That kind of pre-commercial validation rarely happens without serious investor conviction, and Jonathan Userovici of Headline — who recommended it — believes it has a differentiated technical approach to a problem that virtually every large enterprise on earth needs solved. In the growing market of European AI startups focused on big data analysis, Fundamental has staked out the most ambitious early valuation.

Gradium

Recommended by Jonathan Userovici, General Partner, Headline

AI agents are proliferating rapidly, but most of them are still primarily text-based. For the next generation of agents to feel genuinely natural in customer-facing, real-time applications, they need voices that are expressive, multilingual, and low-latency enough to work in live conversation. Gradium, a spinout of the prestigious French AI lab Kyutai, has built AI voice models specifically designed for that challenge, enabling real-time text-to-speech across multiple languages at a quality that competes directly with the best in the global market.

The Paris-based startup is positioning itself as a direct rival to ElevenLabs, the American voice AI company. Gradium's French research heritage and Kyutai lineage give it credible technical foundations, and it has already demonstrated market confidence with a 70 million dollar seed round — one of the largest seed raises in European AI history. Jonathan Userovici of Headline sees the voice layer of AI infrastructure as a durable market that will outlast the current hype cycle around agent-based AI systems.

Roofline

Recommended by Floriane de Maupeou, Principal, Serena Data Ventures

The AI hardware landscape has fragmented dramatically over the past three years. Nvidia remains dominant, but a growing roster of specialized chips from AMD, Intel, Cerebras, and Groq means that AI practitioners increasingly face a complex decision about which hardware to target when deploying models. Each chip type requires different optimization, and the cost of getting it wrong is significant. Roofline builds software that bridges that gap, allowing users to deploy AI models efficiently across different types of chips without having to rebuild their stack for each new hardware environment.

A university spinout with strong research credibility, Roofline has the technical foundations to address what is a deeply specialized problem, and the timing is favorable: as the hardware layer continues to diversify, the need for hardware-agnostic deployment tooling will only grow. Floriane de Maupeou of Serena Data Ventures views it as an infrastructure play sitting at a genuine choke point in the AI deployment stack — one that every enterprise building on AI will eventually need to navigate.

Macrodata Labs

Recommended by Floriane de Maupeou, Principal, Serena Data Ventures (investor)

The quality of any AI model is ultimately a function of the quality of the data it was trained on. As foundation models have scaled to hundreds of billions of parameters, the complexity of managing, curating, and validating training data has grown correspondingly. Macrodata Labs, which operates with a deliberately understated "coming soon" landing page, is building tooling designed to help other companies create rigorous, reliable training datasets at scale — a picks-and-shovels play in a gold rush market.

The startup is not building the data itself. It is building the infrastructure for data creation, which positions it as a foundational enabler of the broader AI ecosystem. Every AI company needs training data; increasingly few of them have the internal expertise to manage the process well. Floriane de Maupeou of Serena Data Ventures sees this as one of the most structurally important bets in the European AI supply chain — a company that may never be as famous as the models it helps build, but that could prove essential to many of them.

Multiverse Computing

Recommended by TechCrunch's Julie Bort

Running large AI models on proprietary hardware is expensive, slow, and often impractical for organizations that handle sensitive data. Multiverse Computing has developed a technology that takes proven open-weight models from providers including OpenAI, Meta, DeepSeek, and Mistral AI and compresses them significantly, reducing the cost and computational requirements of running those models without meaningfully sacrificing their performance.

Co-founded by CTO Roman Orus, a professor at the Donostia International Physics Center in the Basque Country, Multiverse Computing brings serious academic credibility to a problem with significant commercial appeal. The Spanish startup has raised 250 million dollars — making it one of the better-capitalized European AI companies outside the foundation model giants — and is targeting enterprises that want to run powerful AI on their own hardware rather than relying entirely on cloud infrastructure. TechCrunch's Julie Bort highlighted it as a practical, deployable AI efficiency startup at exactly the right moment.

Cala

Recommended by TechCrunch's Anna Heim

AI agents are proliferating rapidly, but most of them share a fundamental limitation: they lack the structured contextual knowledge needed to reason reliably about complex, domain-specific situations. Cala is building what it calls the knowledge layer for AI agents — a knowledge graph infrastructure that gives agents the grounded, relational understanding they need to perform at a higher level of accuracy and consistency than retrieval-augmented generation alone can provide.

The startup was founded by Elisenda Bou-Balust, a Spanish AI expert whose previous company Vilynx built AI for video understanding and was acquired by Apple in 2020. That exit signals both technical credibility and commercial viability, and it has undoubtedly opened doors for Cala as it builds in what TechCrunch's Anna Heim identifies as one of the most structurally important gaps in the current AI ecosystem. As agent-based AI moves from demonstration to production deployment, the knowledge layer problem will only become more pressing — and more valuable to solve.

"Every strong model starts with great data — and the startups building that data infrastructure may prove as valuable as the models themselves."

AI agents, vertical tools & GEO

AI Agents, Vertical Tools, and Generative Engine Optimization

HappyRobot

Recommended by Pablo Ventura, General Partner, Kfund

Building AI agents that look impressive in demos is no longer difficult. Building ones that generate measurable returns on investment when deployed in production is a different matter entirely. HappyRobot has oriented itself specifically around that second challenge, focusing on AI agents for complex operational use cases with a clear emphasis on deployability and demonstrable ROI. The startup is backed by both Andreessen Horowitz and Y Combinator — two validators that rarely overlap and whose combined endorsement speaks to the quality of the underlying work.

HappyRobot is headquartered in the United States, but its three co-founders and a significant part of its team are Spanish, making it part of the quietly growing wave of European-founded companies that have chosen to scale in the American market while drawing on European talent. Pablo Ventura of Kfund recommended it as an example of Spanish technical talent achieving genuine global recognition in one of the most competitive areas of current AI agent development.

Botify

Recommended by Claire Houry, General Partner, Ventech (investor)

Search engine optimization is undergoing one of the most significant structural shifts in its history. As AI-powered overviews replace traditional blue-link results and tools like ChatGPT, Perplexity, and Google's AI Mode become primary discovery surfaces for millions of users, brands face an urgent need to understand how they appear in generative AI responses rather than just in conventional search rankings. This new discipline has acquired its own acronym — generative engine optimization, or GEO — and Botify was in this space before most of its competitors had identified it as a space worth entering.

A participant in TechCrunch's Disrupt New York back in 2016, Botify has reinvented itself to meet this new reality and counts Macy's and The New York Times among its customers. Competitors including Otterly.AI and Profound have entered the GEO market more recently, but Botify brings years of existing customer relationships and established infrastructure. Claire Houry of Ventech sees a company with the institutional knowledge and client base to defend its position as this category scales into what could become a multi-billion dollar market.

Legora

Recommended by Par-Jorgen Parson, Partner, Northzone

The legal technology sector has become one of the most intensely contested arenas in enterprise AI. Legora is the Swedish-born challenger that has recently decided to compete not just on product but on brand, enlisting actor Jude Law as the face of a campaign that explicitly positioned it against main rival Harvey with the tagline "law just got more attractive." It is an unusual move for a B2B software company, and it generated exactly the attention the company was looking for, sparking a widely-shared debate in legal tech circles.

Beyond the marketing flourish, Legora's underlying business is serious. The company has reached a valuation of 5.55 billion dollars — making it one of Stockholm's most valuable AI startups — and has relocated its headquarters to New York while retaining its Swedish roots. Par-Jorgen Parson of Northzone recommended it as a company that has demonstrated both strong product execution in AI legal technology and the brand savviness to compete for mindshare in a market growing fast enough to support multiple scaled winners.

Fintech for small business

Fintech and Financial Infrastructure for Small Business

Apron

Recommended by Jan Hammer, Partner, Index Ventures (investor)

Invoice management is not a glamorous problem, but for small business owners it is a persistent and time-consuming one. Tracking which invoices have been sent, which have been paid, which are overdue, and which suppliers need to be chased involves the kind of administrative overhead that compounds painfully as a business grows. Apron has built a platform specifically designed to simplify that process, helping small businesses manage their payables without the complexity of enterprise-grade financial software.

Jan Hammer of Index Ventures highlighted the durability of the European SMB fintech opportunity: there are millions of small businesses globally, and their owners are consistently willing to pay for tools that genuinely save them time. Apron raised 15 million dollars in 2023 and has continued to expand its capabilities since. In a market where many fintech companies have targeted larger enterprises for higher average contract values, Apron is betting that the aggregate value of serving millions of smaller customers — combined with the switching costs of an embedded financial workflow tool — is equally compelling.

Pennylane

Recommended by Jan Hammer, Partner, Index Ventures

When Pennylane launched in France in 2021 with an accounting-focused proposition for small businesses, it was entering a crowded space. Since then, it has done something that most fintech startups fail to execute: it has expanded its scope without losing its core user base. Having achieved unicorn status in 2024, the French company is now pursuing an ambition to build what it describes as a unified financial operating system for European small and medium businesses, covering everything from accounting and invoicing to cash flow management and financial reporting.

Jan Hammer of Index Ventures, who recommended it separately from Apron, sees the European SMB fintech opportunity as large enough to sustain multiple winners, particularly given the fragmentation of existing solutions across different European markets. Pennylane's French-first approach has given it deep penetration in one of Europe's largest business markets, and its expansion strategy signals it is now testing whether that product can travel across borders with the same effectiveness. For a company that started in accounting, the ambition it has assembled around itself is considerable.

Robotics, manufacturing & physical AI

Robotics, Physical AI, and Industrial Automation

Inbolt

Recommended by Claire Houry, General Partner, Ventech

Factory automation has been a fixture of industrial investment for decades, but the current wave is different in a significant way: it is bringing AI perception and adaptability to production lines that previously required rigid, preprogrammed robotic systems. Inbolt combines AI and robotics to expand what automation can do on manufacturing floors, enabling robots to handle tasks that require visual recognition, real-time adjustment, and contextual decision-making rather than just repeated mechanical motion.

The startup is already active in more than seventy factories across the automotive industry, electronics, and home goods production — a deployment scale that is unusual for a company still in its growth phase and that speaks to the practical robustness of its systems. Claire Houry of Ventech, who recommended it, sees physical AI for European manufacturing as one of the most consequential and underappreciated applications of the current generation of AI research. Unlike software-only AI companies, Inbolt's installed base creates switching costs and recurring revenue streams that provide a more defensible competitive moat.

Theker

Recommended by Pablo Ventura, General Partner, Kfund (investor)

Robots as a service is a model that has struggled to achieve mainstream adoption partly because the hardware is expensive, the maintenance requirements are significant, and most operators lack the technical expertise to keep sophisticated robotic systems running smoothly. Theker approaches this challenge with a managed service model designed to lower the barrier to entry for companies that want robotic automation without taking on the full capital and operational burden of ownership.

What makes Theker particularly interesting is its backer: the startup is supported by Zara owner Inditex through a dedicated investment fund managed by Mundi Ventures, giving it both a major anchor customer relationship and access to the operational scale of one of the world's largest fashion retailers. Theker's AI-enabled robots have obvious applications in Inditex's logistics operations, but the company is also developing use cases in waste management and food and beverage production. Pablo Ventura of Kfund, who is an investor, views the combination of a well-capitalized backer and a diversified use case portfolio as a strong foundation for growth in European robotics as a service.

Energy, fusion & the clean tech frontier

Energy, Fusion, and the Clean Tech Frontier

Flower

Recommended by Par-Jorgen Parson, Partner, Northzone (investor)

The promise of renewable energy has always been complicated by one stubborn reality: the sun does not always shine, and the wind does not always blow. Managing the variability of wind and solar generation has become one of the defining infrastructure challenges of the energy transition, and solutions that can smooth out that variability have significant economic value. Flower uses AI combined with battery energy storage systems to make renewable energy generation more predictable and grid-stable, turning intermittent sources into reliable supply.

The Swedish company has recently raised over 60 million euros in debut bond financing — a milestone signaling it has reached the scale where institutional debt markets are taking notice. Par-Jorgen Parson of Northzone, who recommended it as an investor, sees Flower as a company positioned at one of the most durable intersections in the modern economy: the urgent need to integrate renewable energy into existing grid infrastructure without sacrificing reliability. As more European countries push toward ambitious clean energy targets, the demand for exactly what Flower provides is structurally guaranteed to grow.

Proxima Fusion

Recommended by Daria Saharova, Managing Partner, World Fund

Nuclear fusion has been described as the energy technology of the future for so long that cynicism about its timeline has become reflexive. But the funding patterns around fusion have shifted dramatically, and Proxima Fusion is one of the primary reasons the European component of that shift is credible. The Munich-based startup, a spinout from the Max Planck Institute for Plasma Physics, is pursuing the stellarator approach to fusion — a technically demanding but theoretically more stable path than the tokamak designs favored by most competitors globally.

Having already secured a 130 million euro Series A, Proxima recently took its most dramatic step yet: securing 460 million dollars from the state of Bavaria to support the construction of what it plans to be Europe's first commercial fusion power plant, beginning with a demonstration stellarator near Munich. Daria Saharova of World Fund recommended it as one of Europe's strongest nuclear fusion startup contenders, and the commitment from Bavaria suggests that at least one government has decided the odds of commercial fusion energy are worth taking seriously with real money.

Space & the new space economy

Space, Satellites, and the New Space Economy

PLD Space

Recommended by TechCrunch's Anna Heim

Europe's dependence on American and Russian launch capabilities has been a source of strategic anxiety for European governments and space agencies for years, and the disruption of existing arrangements in recent years has added urgency to that concern. PLD Space is one of the companies trying to solve it from the ground up. The Spanish startup successfully launched Miura 1, a suborbital rocket, in 2023 — becoming one of the very few European commercial space companies to have actually put hardware into the sky. It is now developing Miura 5, a reusable orbital launcher designed for small satellite payloads.

In March, PLD Space secured a 209 million dollar Series C led by Mitsubishi Electric, bringing its total funding to more than 350 million dollars and cementing its position as one of the most credibly funded European space startups. TechCrunch's Anna Heim highlighted it as a company that has cleared the most difficult hurdle in the launch business: proving that its technology actually works. With a reusable orbital vehicle in development and serious institutional backing, PLD Space represents Europe's best near-term hope for launch autonomy in the small satellite segment.

Space Forge

Recommended by Daria Saharova, Managing Partner, World Fund (investor)

Manufacturing semiconductors in space sounds like science fiction, but the underlying physics is compelling: the microgravity and high-vacuum environment of low Earth orbit enables the creation of materials with properties that are extremely difficult or impossible to achieve on Earth. Space Forge is building the commercial infrastructure to exploit that environment, with a specific focus on producing semiconductor components in orbit and returning them to Earth for use in high-performance computing and other applications where material quality is critical.

The Cardiff-based startup recently achieved a significant milestone, generating plasma in low Earth orbit using its Forgestar-1 platform — a proof-of-concept demonstration that the underlying manufacturing process can function in the space environment. It raised 30 million dollars in a Series A in 2025 and has the tailwinds of both growing semiconductor demand and increasing political emphasis on supply chain diversification working in its favor. Daria Saharova of World Fund, who is an investor, sees in-space manufacturing moving from speculative to operational faster than most outside observers realize.

Where these 21 startups are headquartered across Europe

Spain leads the geographic spread with five companies, reflecting a decade of deepening technical talent in Madrid and Barcelona. France follows with four, anchored by its world-class AI research ecosystem. Two US-headquartered companies on the list have European founding teams, illustrating the transatlantic dimension of European startup ambition.

Patterns & themes

Three Investment Themes That Cut Across These 21 Companies

Six investment themes unifying the 21 featured startups

Several startups appear in more than one cluster, reflecting the convergence of AI with hardware, defense with space infrastructure, and financial tooling with AI automation. The clusters reveal the underlying logic of European deep tech investment rather than simple sector categorisation.

From Inbolt's factory robots to Flower's grid management, the most capital-efficient AI bets are not pure software plays but companies where AI enables something physical that was previously impossible or uneconomical to achieve at scale.

Alta Ares, Optics11, Cailabs, PLD Space, and Space Forge all benefit from European governments deciding that strategic autonomy is worth paying for, creating durable government-backed demand alongside commercial markets.

Macrodata Labs, Roofline, Fundamental, Gradium, and Cala are all building infrastructure for AI rather than end-user applications — a layer that scales with every new model and every new agent that gets deployed commercially.

What is striking about this cohort is how rarely any of these companies are trying to out-ChatGPT ChatGPT. European AI companies have learned, sometimes the hard way, that competing with American consumer AI incumbents on their home turf is a difficult proposition. The smarter bet — which most of these startups appear to have absorbed — is to find problems where European strengths, whether in physics research, aerospace engineering, defense procurement relationships, or deep institutional trust in financial services, give a natural competitive advantage that American counterparts do not automatically possess.

The fintech cluster around SMBs is another coherent pattern. Apron and Pennylane are both attacking the same basic problem from different angles: European small business owners are underserved by financial software that is either too simple or too enterprise-grade. The market is large, the incumbents are complacent, and the switching costs for an embedded financial workflow tool are meaningful once a business has reorganized its processes around it.

Disclosed funding by startup — bubble size reflects total capital raised

Proxima Fusion dwarfs most peers thanks to its 460 million dollar Bavarian state grant. Fundamental and Multiverse Computing represent the largest pure-AI funding rounds among European AI startups on this list. Several companies including Macrodata Labs and Cala have not yet disclosed funding publicly.

Frequently asked questions

Frequently Asked Questions

What makes a European AI startup worth watching in the current market?

The most credible European AI startups in the current market tend to share a few characteristics. They are typically building in areas where European research institutions have genuine depth, such as photonics, plasma physics, or industrial robotics. They have founding teams with demonstrated track records of execution, either through previous exits or through significant academic contributions. And they are addressing problems where regulatory familiarity, institutional relationships, or geographic proximity to European customers gives them a structural advantage that is difficult for American competitors to replicate simply by opening a European office.

Which sectors are attracting the most venture capital in European deep tech right now?

Defense technology, AI infrastructure, energy transition, and space represent the four areas seeing the most significant acceleration in European venture capital interest. The war in Ukraine catalyzed defense investment that had been constrained by ethical considerations for years. AI infrastructure has attracted capital because every enterprise on the continent needs to navigate the transition to AI-powered operations. Energy technology benefits from both regulatory mandates and economic incentives. Space has benefited from strategic concerns about launch autonomy and the rapid commercialization of low Earth orbit through satellite constellations and in-orbit manufacturing.

How do these lesser-known European startups compare to Lovable and Mistral AI?

Lovable and Mistral AI represent the very top of a much larger pyramid. Both have achieved the kind of scale, brand recognition, and commercial traction that brings mainstream media coverage and broad investor attention. The 21 startups described here are at earlier or more specialized stages. Some are building the infrastructure that companies like Mistral depend on. Others are applying AI to physical domains where consumer-facing visibility is inherently lower. None of them currently have nine-digit revenues, but several have already achieved valuations that suggest their investors believe they will eventually reach comparable scale.

Are there promising European AI startups outside of France and the UK?

The geographic distribution of this list reflects the true breadth of European technical talent. Spain has produced several companies here, including PLD Space, Multiverse Computing, and the Spanish co-founders of HappyRobot. The Czech Republic is represented by BottleCap AI. Sweden contributes Flower and Legora. Germany is home to Proxima Fusion. The Netherlands hosts Optics11. France has multiple entries including Gradium and Botify. This distribution is not an accident: deep tech talent is distributed across the continent, and the best investors have learned to look well beyond London and Paris for it.

What role do European research institutions play in producing these startups?

Several of the companies on this list are direct spinouts from European research institutions. Proxima Fusion emerged from the Max Planck Institute for Plasma Physics. Roofline was incubated at a university. Gradium spun out of Kyutai, a French AI research lab. Multiverse Computing was co-founded by a physics professor. This pattern reflects one of Europe's genuine structural strengths: a dense network of research universities and publicly funded scientific institutions that produce world-class technical talent and, increasingly, world-class commercial spinouts. Historically, that talent drained to American tech companies. The current generation is more likely to stay and build something in Europe.

Closing thought

The European startup ecosystem has spent years being measured against American benchmarks it was never designed to match. The venture pools are smaller, the exit markets less liquid, the risk appetite historically more conservative. What this list suggests is that something is changing at the level of ambition. These are not companies building modest European alternatives to American products. They are companies trying to invent new categories, solve problems that do not yet have solutions, and win markets that are genuinely global in scope. Whether the infrastructure around them — from capital availability to talent retention to regulatory support for deep tech — can keep pace with that ambition is the defining question for European innovation over the next decade. The founders, for their part, are not waiting for the answer.