What Nobody Is Telling AI Founders in 2026

🚀 AI Funding Trends 2026

In This Edition:

- 🤖 AI Is Eating the Boring Work First

- 📊 AI Funding Trends 2026

- 🤫 What Nobody Is Telling AI Founders

- ⚠️ The Silent Startup Killers

- 📈 Series A vs Series B Valuation Growth in AI

- 💰 The $0 to $100K MRR Playbook

- 📩 The Cold Email That Closed $250K

AI Is Eating the Boring Work First

57 startups. $316M. 15 countries. The pattern is clear: the biggest early-stage bets are going to AI that replaces friction, not AI that creates features.

- Vertical specificity wins funding. MeltPlan ($14M) doesn't do "construction AI." It does takeoffs, compliance, and cost estimation — three steps that kill preconstruction timelines. Specific beats broad at seed stage, every time.

- The front desk is the new frontier. Patientdesk.ai ($1M, YC W26) answers dental phones 24/7, books appointments, and verifies insurance. The insight isn't dental — it's that every service business has a broken front desk bleeding revenue every night it goes unstaffed.

- Distribution channels are the moat, not the model. General Magic ($7M) runs insurance workflows over SMS and iMessage. No new app. No onboarding friction. The channel is the product. Founders building standalone apps should ask: does this need its own surface, or does it belong inside a channel people already live in?

- Hardware lock-in is a real pain to bet on. Callosum ($10M) lets AI models run across heterogeneous chips instead of locking into massive GPU clusters. The infrastructure play isn't glamorous — but infrastructure that saves enterprise compute costs doesn't need to sell a vision. It sells a bill.

- Real-world data is the new training edge. RLWRLD ($26M) trains robotics foundation models inside actual factories and warehouses — not simulation. Founders building AI in controlled environments are optimizing for demos. Founders building in the mess are optimizing for deployment.

- Human-AI hybrid care is finding serious capital. Oska Health ($13M) pairs AI with human coaches for chronic disease management between doctor visits. The hybrid model matters: pure AI faces regulatory drag; pure human scales poorly. The combination ships faster and closes payers.

- Workflow-native beats standalone. Kinfolk ($7M) runs HR operations inside Slack and Teams — updating HRIS records, drafting documents, managing lifecycle changes. No new interface to learn. No change management budget needed. Execution happens where the team already works.

Curious who’s leading the biggest bets right now? Click below to explore deeper investor signals, valuation moves, and funding context. 👇

🚀 AI Funding Trends 2026

🚀 AI Funding Trends 2026

The race to public markets is accelerating. Anthropic is moving fast — CFO hired, law firm engaged, bankers in the room. OpenAI is not.

Here's what founders miss about this moment:

- Capital structure is strategy. Anthropic's enterprise focus makes its financials legible to public markets. OpenAI's sprawl — hardware, robotics, BCI, space — makes scrutiny dangerous.

- The "Dara moment" is real. Vision-driven founders often hit a ceiling before IPO. Boards swap them for operators. It happened at Uber. It may happen at OpenAI.

- Competitor IPOs create pressure. Anthropic going public forces OpenAI's hand — and forces your investors' hands too.

The lesson for founders: market timing is a weapon. Move before your competitor defines the narrative.

What Nobody Is Telling AI Founders in 2026

Gen Z Is Rewriting the AI Playbook — Before 30

The Forbes 30 Under 30 AI list just dropped. The signal is loud.

$1.5B raised. 97% founders. Most still under 28.

Here's what separates this cohort from the rest:

- They picked vertical, not horizontal. Decagon owns customer service. Legora owns legal. Moonlake owns 3D world-building. No one tried to build everything.

- They went enterprise early. Duolingo. Hertz. 300 law firms. These aren't demo users — they're paying contracts with real retention pressure.

- They dropped out with conviction. Stanford exits aren't reckless — they're calculated bets made after early traction, not before.

- They moved before the market was obvious. Accounting automation. Interactive 3D AI. Legal tech. Each felt niche. Each is now a category.

The pattern is clear: niche fast, prove retention, raise big.

Breadth is the enemy of traction at early stage.

The Silent Startup Killers No One Talks About

Your Startup Didn't Die Last Month. It Died 90 Days Ago.

Most founders miss the moment of failure. It's never the fundraise that fell through. Never the competitor that launched. It happens quietly — in the decisions made months earlier.

The real killers:

- Expertise blinds. Deep industry knowledge filters out signals that outsiders catch immediately. The more you "know," the less you see.

- The 90-day clock is real. No validation by day 90? The company is already dead. The bank account just hasn't caught up yet.

- Assumptions compound. Every untested hypothesis is debt. Every delayed user conversation is interest. Most startups are insolvent before they're broke.

- Competence is a trap. Building feels productive. Selling feels uncomfortable. Founders optimize for the wrong metric.

- "Soon" means never. Perfect timing is fear wearing a calendar.

The fix isn't motivation. It's scheduled destruction.

Poke holes in the business every 72 hours. Kill weak assumptions before the market does. Test before comfort. Ship before perfect.

The market has no patience for founders who confuse planning with progress.

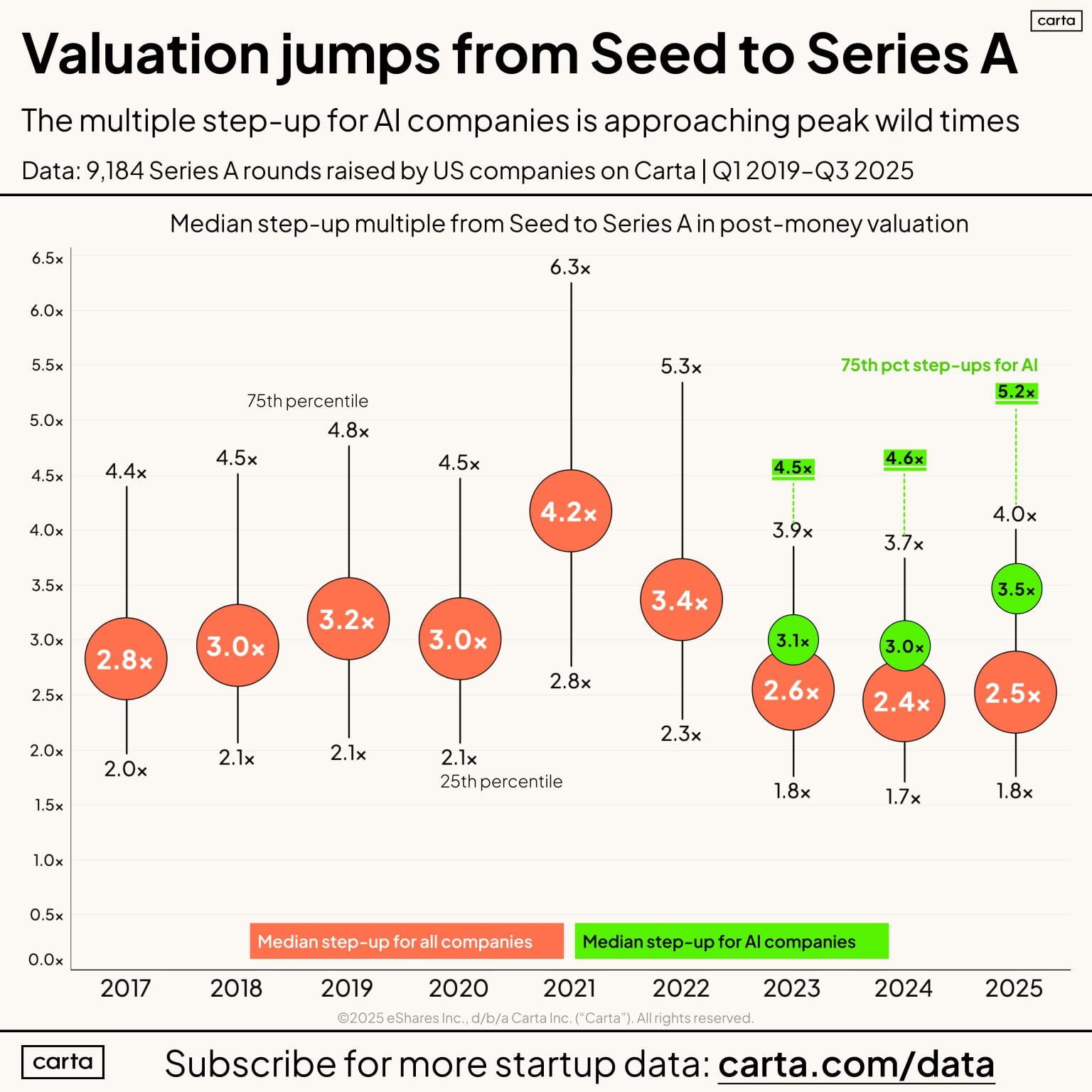

Series A vs Series B Valuation Growth in AI

Series A vs Series B Valuation Growth in AI — The Gap Is Wider Than You Think.

The data is in. 9,184 Series A rounds. All US startups. 2019–Q3 2025.

The valuation jump from Seed to Series A tells the whole story.

Here's what the numbers show:

- Non-AI founders face a harder market than pre-2021. Multiples have compressed. The window is tighter. The bar is higher.

- AI startups are getting 3.5x step-ups at Series A. The most in-demand AI companies? Closer to 5x.

- The biggest multiple expansion happens between Seed and A. Every subsequent round — A to B, B to C — expands by a smaller factor.

- Round sizes are bigger than ever. Post-money comparisons account for this. The dilution math has changed.

- For investors, entry price still wins. Premium valuations at Seed compress returns downstream.

The strategic implication for founders: the Seed-to-A transition is the highest-leverage moment in the entire fundraising journey.

Nail the narrative here. The valuation ceiling is highest — and the market is actively rewarding AI positioning right now.

Miss this window and every subsequent round gets harder to justify.

The $0 to $100K MRR Playbook (Step-by-Step Breakdown)

$700K/Month Across 4 Apps. The Playbook Is Simpler Than You Think.

Tibo didn't get lucky. He ran the same 12-step system — four times — until four separate products crossed $100K/month each.

The pattern that made it repeatable:

- Ship in days, not months. Use boilerplates, no-code, shortcuts. A 90% failure rate means speed is survival — not quality.

- Talk to 5–10 real users before anything else. Not friends. Not family. The exact person with the exact pain.

- Route support to your DMs until $10K MRR. Fixes in 10 minutes create customers for life.

- Don't scale before stickiness. Broad acquisition with low retention is just burning cash faster.

- One or two channels will drive everything. Go broad to find them. Then go all-in and kill the rest.

The meta insight: builders are the shyest founders. They build instead of talk. That single habit is what separates a product from a business.

Complaints aren't churn signals. They're commitment signals. The user who complains wants to stay.

Speed of learning beats speed of building — every time.

The Cold Email That Closed $250K

47 Words. $250K Deal. Here's Why Less Sells More.

The cold email that closed a quarter-million dollars wasn't clever. It wasn't personalized. It was 47 words.

Most founders write emails that feel like sales pitches. That's the problem.

The moment a prospect senses persuasion — they're gone.

What actually works:

- Lead with the offer, not the story. A strong front-end offer does the selling before the conversation even starts.

- Casual copy outperforms polished copy. Formal language signals "sales mode." Conversational language signals "real person."

- Short emails get read. Long emails get skimmed then deleted. Brevity is credibility.

- Follow-ups aren't about pressure. Structure them to stay visible without feeling desperate.

- Personalization is overrated. A razor-sharp offer beats a researched icebreaker every time.

The real bottleneck isn't the email — it's the offer. Weak offers need long emails to compensate. Strong offers need almost nothing.

Founders spend weeks perfecting outreach copy and minutes thinking about what they're actually offering. That's backwards.

Fix the offer first. Then write 47 words around it.

🔥WEB PICKS

- Nvidia x Groq at GTC. A new inference-focused processor — with OpenAI locked in as anchor customer via a $20B licensing deal. The inference war just escalated.

- Google is selling TPUs to Meta. A multibillion-dollar chip deal that puts Google directly in Nvidia's lane. The accelerator market is no longer a monopoly.

- Why Claude Code is winning. SemiAnalysis broke down Claude Code's role as an agentic inception point — and concluded Anthropic will outgrow OpenAI from here. Worth reading in full.

- The best AI chip explainer online right now. MatX founder Reiner Pope on Cheeky Pint: GPUs vs CPUs, what's broken, what comes next. Required watching for any founder building on AI infrastructure.

- Cut your token bill 40–60% immediately. Corey's model routing guide is the most actionable cost-reduction framework out right now — three tiers, one model per task type, zero compromise on output quality.