40+ New Unicorn Startups: Every Billion-Dollar Company Minted in 2026 (Full List)

A comprehensive, research-backed guide to every venture-backed startup that has crossed the $1 billion valuation mark in 2026 — covering AI, healthcare, robotics, crypto, and beyond.

What Is a Unicorn Startup and Why Does the 2026 Class Matter?

A unicorn startup is a privately held company that has reached or surpassed a $1 billion valuation before going public or being acquired. The term, coined by venture capitalist Aileen Lee in 2013, was once used to describe the rarest of outcomes in the startup world. Today, with artificial intelligence reshaping entire industries and capital flowing toward technology at an unprecedented pace, the number of new unicorns being minted has accelerated dramatically.

The 2026 class of unicorn startups is especially significant. Nearly 40 companies have crossed the billion-dollar threshold in just the first three months of the year alone. While AI dominates the list, the diversity of sectors represented tells a richer story: humanoid robotics companies, crypto-native banks, women's health platforms, home energy storage businesses, and even a company that mines raw materials in space have all joined the ranks.

This guide breaks down every newly minted unicorn startup of 2026 in detail. Each entry includes the company's core mission, founding date, total funding raised, lead investors, and the valuation milestone that earned it a spot on this list. The goal is to give founders, investors, and technology professionals a clear picture of where venture capital is going, which sectors are attracting the most attention, and what patterns define the most-funded companies right now.

1000+ Angel Investors

A massive list of angel investors who are actively looking to fund early-stage startups. Whether you’re launching your first business or scaling up, these investors could be your next big backer.

AI and Machine Learning Unicorns of 2026

Artificial intelligence dominates the 2026 unicorn class. From foundational model labs and AI chip designers to generative video platforms and coding assistants, the sheer breadth of AI-related companies achieving billion-dollar valuations reflects the scale of the current technology cycle. Investors are not just backing broad AI infrastructure; they are funding highly specialized tools designed to make AI faster, more interpretable, and more accessible to domain experts.

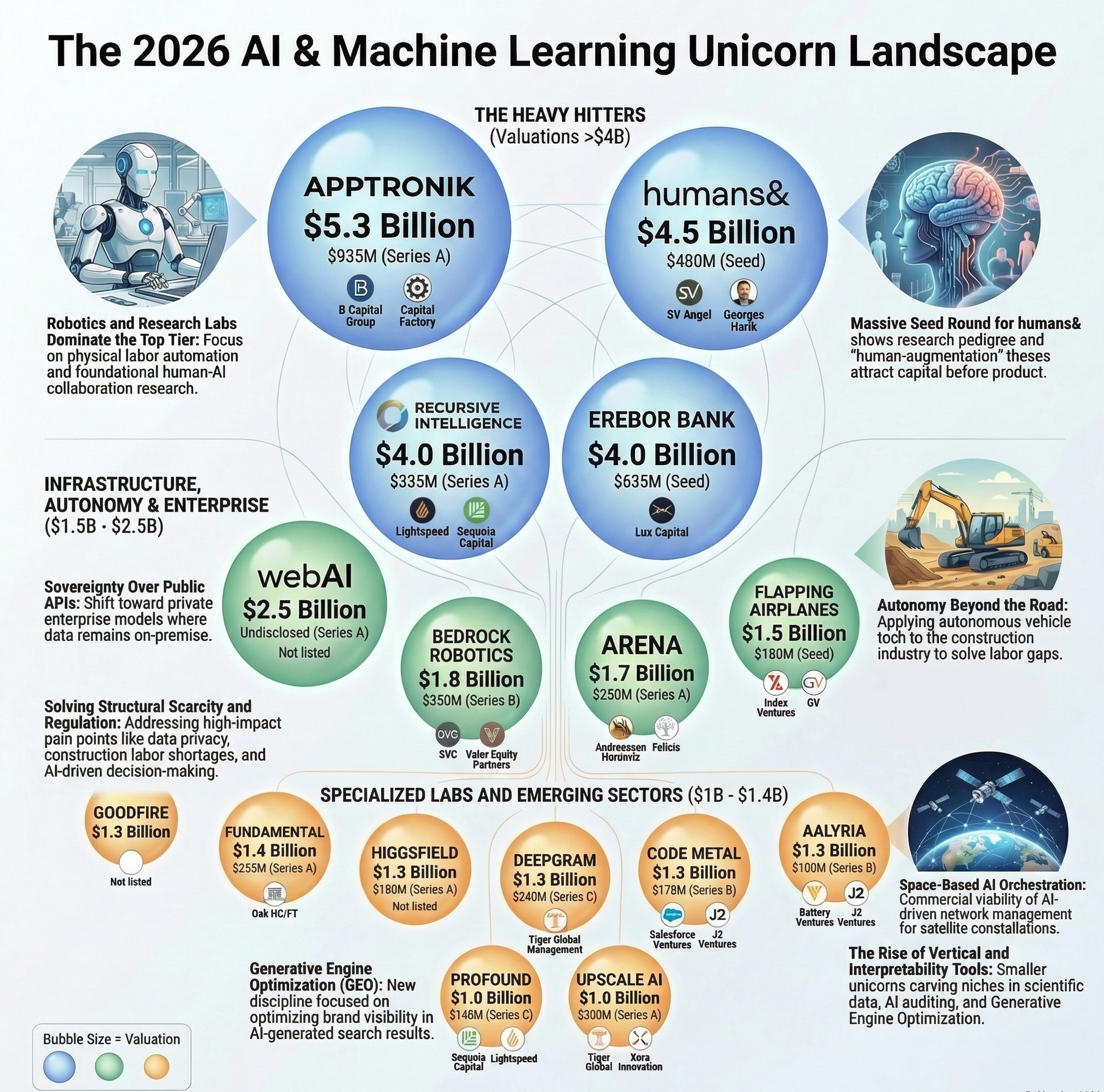

Apptronik — $5.3 Billion

Apptronik, founded in 2016, is one of the most capitalized humanoid robotics companies in the world. The Austin-based startup builds full-bodied humanoid robots designed to perform physical labor tasks in industrial, logistics, and manufacturing environments. Its most recent funding round, a $935 million Series A led by B Capital Group and Capital Factory, brought total funding to $935 million and valued the company at $5.3 billion.

The timing of this milestone is notable. As labor shortages persist across manufacturing and warehousing, companies like Apptronik are positioning humanoid robots as a practical, deployable solution rather than a distant science fiction concept. Apptronik has existing partnerships with major logistics and manufacturing operators, which gives its development roadmap commercial validation beyond investor optimism.

Key Takeaway: Humanoid robotics is no longer a fringe sector. Apptronik's $5.3 billion valuation signals that investors are now treating deployable, general-purpose robots as near-term commercial infrastructure.

humans& — $4.5 Billion

humans& is an AI research lab focused on creating AI systems that genuinely collaborate with human workers rather than replace them. The company raised a $480 million seed round led by SV Angel and investor Georges Harik, achieving a $4.5 billion valuation at the earliest stage of its lifecycle. The scale of this seed round is exceptional and reflects the enormous premium that investors are placing on foundational AI research teams in 2026.

Unlike many AI labs focused solely on raw model performance, humans& has built its identity around the human-AI collaboration thesis: the idea that the most commercially valuable AI systems will be those that augment skilled workers rather than automate them entirely. This positioning has attracted both strategic and financial capital from some of the most active names in venture.

Key Takeaway: The humans& seed round demonstrates that in 2026, pedigree and research vision can attract hundreds of millions of dollars before a product ships. The human-AI collaboration framing is becoming a distinct and fundable category.

Recursive Intelligence — $4 Billion

Founded in 2025, Recursive Intelligence designs AI-powered chips optimized for machine learning inference and training workloads. The company raised a $300 million Series A round at a $4 billion valuation, with backing from Lightspeed Venture Partners and Sequoia Capital. Total funding to date sits at approximately $335 million.

The company represents a growing conviction among investors that the semiconductor layer of the AI stack is as strategically important as the model layer. As demand for AI compute continues to outpace supply, startups offering differentiated chip architectures are attracting outsized attention from both financial investors and potential strategic acquirers.

Key Takeaway: AI chip design startups are commanding valuations that rival established foundational model companies, reflecting a market-wide understanding that compute scarcity is a structural feature of the AI era, not a temporary bottleneck.

Erebor Bank — $4 Billion

Erebor Bank occupies an unusual space in this list: it is a licensed bank, not a software company. Founded in 2025 by Palmer Luckey, the creator of the Oculus VR headset and founder of defense technology company Anduril, Erebor specializes in serving crypto businesses and digital asset clients. The company raised a $635 million seed round from investors including Lux Capital, resulting in a $4 billion valuation before it had processed a single transaction publicly.

The thesis behind Erebor is straightforward: crypto companies, from exchanges to custody providers to blockchain infrastructure operators, have historically struggled to maintain banking relationships with traditional financial institutions. Erebor is designed to fill that gap by providing regulated banking services that are purpose-built for the compliance and operational needs of crypto businesses.

Key Takeaway: Erebor Bank's $635 million seed round is one of the largest in history for a financial institution at formation stage. It reflects a growing institutional conviction that regulated banking infrastructure for digital assets is a long-term structural need, not a speculative niche.

webAI — $2.5 Billion

webAI enables organizations to build and operate their own private enterprise AI models, keeping data and model weights on their own infrastructure rather than sending it to third-party API providers. Founded in 2019, the company raised an undisclosed Series A round that valued it at $2.5 billion.

As data privacy regulations tighten globally and enterprises grow more cautious about the security implications of sending sensitive data to external AI providers, the market for on-premise and private cloud AI deployment has grown significantly. webAI addresses this directly, positioning itself as the infrastructure layer for enterprises that want the capabilities of large language models without the data residency risks.

Key Takeaway: Enterprise demand for private AI deployment is creating a substantial market distinct from the public API economy. webAI's $2.5 billion valuation reflects investor confidence that data sovereignty concerns will sustain this category for years.

Arena — $1.7 Billion

Arena builds AI tools that help business leaders make faster and better decisions by synthesizing large volumes of operational data into actionable recommendations. Founded in 2022, the company raised a $150 million Series A at a $1.7 billion valuation, with backing from Andreessen Horowitz and Felicis. Total capital raised stands at $250 million.

The decision intelligence category, which Arena occupies, sits at the intersection of analytics, AI, and executive workflows. Rather than positioning itself as a general-purpose business intelligence tool, Arena targets the specific moment when a leader needs to choose between competing strategic options and wants an AI-driven analysis to support that choice.

Key Takeaway: Decision intelligence, not just data visualization, is the next frontier of enterprise AI. Arena's funding trajectory suggests that investors see enormous willingness-to-pay at the executive layer of the enterprise stack.

Bedrock Robotics — $1.8 Billion

Bedrock Robotics builds AI-powered autonomy systems for construction equipment, allowing bulldozers, excavators, and other heavy machinery to operate with minimal human involvement. Founded in 2024 by a former Waymo engineer, the company raised a $270 million Series B from investors including 8VC and Valor Equity Partners, bringing total funding to $350 million at a $1.8 billion valuation.

The construction industry faces some of the most persistent labor shortages of any sector in the economy. Bedrock's autonomy stack targets this pain point directly, promising the ability to run 24-hour construction cycles with significantly reduced headcount. The company's Waymo lineage gives it credibility in the autonomous vehicle technology community, and its early partnerships with construction firms suggest real-world deployment is not far off.

Key Takeaway: Autonomous construction equipment is emerging as a commercially viable category faster than many expected. Bedrock Robotics' $1.8 billion valuation at Series B reflects confidence in near-term revenue, not distant potential.

Fundamental — $1.4 Billion

Fundamental is an AI laboratory building foundational models designed to analyze exceptionally large and complex datasets, with initial applications in scientific research and enterprise data environments. Founded in 2024, it raised a $255 million Series A, the bulk of which came from healthcare and technology-focused investor Oak HC/FT, achieving a $1.4 billion valuation.

What distinguishes Fundamental from many other foundation model labs is its focus on structured and scientific data rather than natural language. This positions the company to serve industries like biomedical research, materials science, and financial services, where the data is dense, domain-specific, and highly valuable.

Key Takeaway: Not all foundation model companies are building the next ChatGPT. Fundamental's targeted approach to scientific and structured data represents a maturing thesis: vertical foundation models can command large valuations without competing directly with general-purpose AI providers.

Goodfire — $1.3 Billion

Goodfire develops interpretability tools that help AI researchers and engineers understand what is actually happening inside large AI models. Sometimes called AI mechanistic interpretability research, this field attempts to decode the internal representations and reasoning patterns of neural networks. The company raised a $150 million Series B at a $1.3 billion valuation.

As AI systems become more capable and more widely deployed in high-stakes contexts, regulators and enterprises alike are demanding better explanations for AI behavior. Goodfire's tools are positioned as essential infrastructure for any organization that needs to audit, verify, or certify the behavior of AI models. This creates a natural enterprise sales motion tied directly to compliance and governance needs.

Key Takeaway: AI interpretability is transitioning from a research curiosity to a compliance necessity. Goodfire's billion-dollar valuation suggests investors believe regulators and enterprise buyers will create sustained commercial demand for tools that explain AI decision-making.

Higgsfield — $1.3 Billion

Higgsfield is a generative AI video startup founded in 2023 by a former executive from Snap. The company raised a $180 million Series A, reaching a $1.3 billion valuation. Higgsfield builds tools that allow creators, marketers, and production teams to generate and edit high-quality video content using AI prompts and reference material, dramatically reducing the time and cost associated with traditional video production workflows.

Generative video represents one of the fastest-evolving segments of the AI landscape. Unlike text or image generation, video synthesis requires temporal coherence and complex understanding of motion, lighting, and physics, making it a genuinely difficult technical problem. Higgsfield's founder background in social media products gives the company a consumer and creator-first design sensibility that differentiates it from more infrastructure-oriented video AI companies.

Key Takeaway: Generative video is following the same commercialization arc as generative image tools, but at a faster pace. Higgsfield's consumer-first approach positions it well for the creator economy market, where speed-to-market and ease of use drive adoption.

Deepgram — $1.3 Billion

Deepgram provides voice AI infrastructure that enables software applications to communicate with humans through speech. Founded in 2015, the company raised a $143 million Series C at a $1.3 billion valuation, bringing total funding to more than $240 million. Investors include Tiger Global Management.

The rise of voice interfaces in everything from customer service applications to enterprise productivity tools has created a large and growing addressable market for Deepgram's real-time transcription and voice understanding APIs. Unlike consumer voice assistants, Deepgram's products are designed to be embedded by developers into their own applications, making it infrastructure rather than a product end users interact with directly.

Key Takeaway: Voice AI infrastructure is a foundational layer of the agentic AI stack. As AI agents increasingly need to interact with humans verbally, companies like Deepgram that provide accurate, low-latency transcription and voice understanding are positioned to benefit from the broader AI application boom.

Code Metal — $1.3 Billion

Code Metal is an AI coding assistant platform built for professional software development teams, founded in 2023. The company raised a $125 million Series B, bringing total funding to over $170 million at a $1.3 billion valuation. Investors include Salesforce and J2 Ventures.

The AI coding assistant market is intensely competitive, with multiple well-funded startups and large technology companies offering similar tools. Code Metal's differentiation lies in its enterprise positioning: the platform is designed for large engineering organizations that need secure, auditable, and customizable AI coding support, rather than individual developers looking for autocomplete functionality.

Key Takeaway: Enterprise AI coding tools require more than good autocomplete. Code Metal's institutional backing and enterprise-first positioning reflects a market understanding that large engineering teams have compliance, security, and workflow needs that consumer-oriented tools do not meet.

Aalyria — $1.3 Billion

Aalyria, spun out of Google in 2021, builds AI-powered orchestration software for complex communication networks including satellite constellations, ground stations, and high-altitude platforms. The company raised a $100 million Series B, reaching a $1.3 billion valuation, with investors including Battery Ventures and J2 Ventures.

As satellite constellations proliferate and the demand for seamless, globally distributed connectivity grows, the software layer that manages routing and orchestration across these networks becomes increasingly critical. Aalyria's origins within Google give it access to deep technical expertise in network optimization and machine learning systems.

Key Takeaway: Space-based network infrastructure is becoming a commercially viable layer of the global communications stack. Aalyria's Google pedigree and specialized focus on AI-driven network orchestration make it a natural beneficiary of the satellite connectivity boom.

Profound — $1 Billion

Profound helps companies optimize their presence in AI-powered search environments, a practice sometimes called Generative Engine Optimization or GEO. Founded in 2024, the company raised a $96 million Series C at a $1 billion valuation, with total funding of approximately $148 million from investors including Sequoia Capital and Lightspeed Venture Partners.

As AI Overviews, conversational search assistants, and AI-generated responses increasingly intercept the search traffic that traditional SEO was designed to capture, companies need new strategies to ensure their content appears in AI-generated answers. Profound is building the analytics and optimization tools that help marketers understand how their brands appear in AI search results and how to improve that visibility.

Key Takeaway: GEO is emerging as a distinct and commercially significant discipline alongside traditional SEO. Profound's growth trajectory suggests that brands are already investing in AI search visibility, not just waiting to see how the landscape evolves.

Flapping Airplanes — $1.5 Billion

Flapping Airplanes is an AI research lab founded in 2025 that raised $180 million in seed funding at a $1.5 billion valuation, with backing from Index Ventures and GV. The lab focuses on fundamental AI research and the development of new model architectures.

The name may be unconventional, but the investor pedigree is serious. Seed-stage AI research labs are achieving valuations that would have been reserved for Series B or Series C companies just a few years ago. This compression of the valuation timeline reflects the speed at which AI capabilities are developing and the premium investors place on teams that can push the frontier forward.

Key Takeaway: Research-stage AI labs are attracting institutional seed funding at valuations that reflect expected future impact rather than current revenue. The concentration of talent and ideas in these early-stage labs represents an important part of the AI innovation ecosystem.

Upscale AI — $1 Billion

Upscale AI provides AI computing infrastructure, founded in 2025, that helps enterprises access and manage GPU resources efficiently. The company raised a $200 million Series A at a $1 billion valuation, bringing total funding to $300 million, with investors including Tiger Global Management and Xora Innovation.

The scarcity and cost of GPU compute remains one of the primary constraints on AI adoption by enterprises. Upscale AI addresses this by offering a managed infrastructure layer that helps companies optimize their AI workloads across available compute, reducing both cost and latency for AI-heavy applications.

Key Takeaway: GPU compute management is becoming an enterprise software category in its own right. As AI workloads multiply, the ability to efficiently allocate and manage compute resources will become as important as the models themselves.

2026 Unicorn Comparison Table: Valuation, Sector, and Funding at a Glance

The table below provides a structured comparison of selected 2026 unicorn startups, organized by valuation, to help readers quickly assess the landscape across different sectors and funding stages.

|

Company |

Valuation |

Founded |

Sector |

Last Round |

Notable Investors |

|

Apptronik |

$5.3B |

2016 |

Humanoid Robotics |

Series A ($935M) |

B Capital, Capital Factory |

|

Erebor Bank |

$4B |

2025 |

Crypto/Fintech |

Seed ($635M) |

Lux Capital |

|

Recursive Intelligence |

$4B |

2025 |

AI Chip Design |

Series A ($300M) |

Lightspeed, Sequoia |

|

humans& |

$4.5B |

2024 |

AI Research |

Seed ($480M) |

SV Angel, Georges Harik |

|

webAI |

$2.5B |

2019 |

Enterprise AI |

Series A (undisclosed) |

N/A |

|

Rain |

$1.9B |

2021 |

Crypto Wallet |

Series C ($250M) |

Lightspeed, ICONIQ Capital |

|

Bedrock Robotics |

$1.8B |

2024 |

Construction AI |

Series B ($270M) |

8VC, Valor Equity |

|

Gecko |

$1.8B |

2013 |

AI & Robotics |

Series D ($125M) |

Founders Fund, Cox Enterprises |

|

Arena |

$1.7B |

2022 |

AI Decision Platform |

Series A ($150M) |

Andreessen Horowitz, Felicis |

|

Pomelo Care |

$1.7B |

2021 |

Maternity Health |

Series C ($92M) |

a16z, First Round Capital |

|

Oxide |

$1.6B |

2019 |

Cloud Infrastructure |

Series C ($200M) |

US Innovative Tech Fund, Eclipse |

|

Varda |

$1.6B |

N/A |

Space Mining |

Series D ($250M) |

Founders Fund, Khosla, Lux Capital |

|

Render |

$1.5B |

2018 |

Cloud Hosting |

Series C1 ($100M) |

General Catalyst, Bessemer |

|

Flapping Airplanes |

$1.5B |

2025 |

AI Research |

Seed ($180M) |

Index Ventures, GV |

|

Skyryse |

$1.1B |

2016 |

Aviation OS |

Series C ($300M) |

Autopilot, Fidelity, Venrock |

|

Positron |

$1B |

2023 |

AI Semiconductors |

Series B ($230M) |

Valor Equity, Jump Trading |

|

TRM Labs |

$1B |

2018 |

Crypto Fraud Prevention |

Series C ($70M) |

Bessemer, PayPal Ventures |

|

Midi Health |

$1B |

2021 |

Women's Health |

Series D ($100M) |

GV, Emerson Collective |

|

Lunar Energy |

$1B |

2020 |

Home Energy Storage |

Series D ($102M) |

B Capital, Prelude Ventures |

Note: This table covers a representative selection of 2026 unicorns across sectors. The full list continues to be updated throughout the year as additional companies cross the $1 billion threshold.

Healthcare and Life Sciences Unicorns of 2026

Healthcare remains one of the most active sectors for new unicorn formation. The 2026 class includes companies addressing psychiatric care, maternity health, digestive disease research, women's health, and patient navigation. Many of these companies use AI and data analytics as core components of their products, but they are fundamentally healthcare businesses, not pure technology plays. This distinction matters to investors assessing clinical outcomes, regulatory pathways, and reimbursement models.

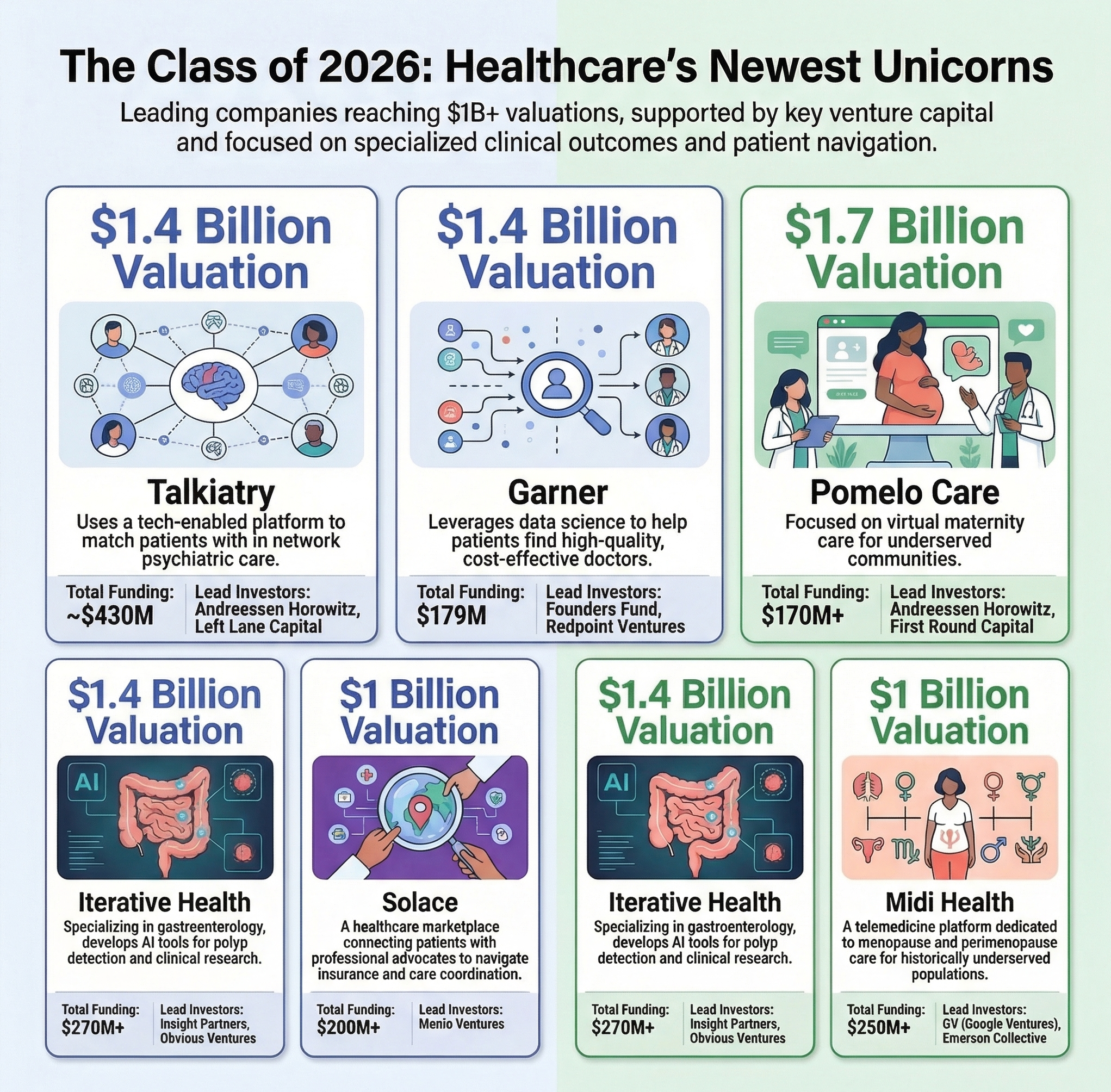

Talkiatry — $1.4 Billion

Talkiatry is working to expand access to psychiatric care by matching patients with in-network psychiatrists and therapists through a tech-enabled platform. Founded in 2019, the company raised a $210 million Series D, bringing total funding to nearly $430 million at a $1.4 billion valuation. Investors include Andreessen Horowitz and Left Lane Capital.

Mental health access remains deeply unequal in the United States, with long wait times and out-of-network costs creating significant barriers for many patients. Talkiatry's model attempts to address both supply and demand-side constraints: it recruits and supports psychiatrists with back-office tools and compliance systems, allowing clinicians to see more patients, while simultaneously providing patients with easier appointment booking and insurance verification.

Key Takeaway: Talkiatry's $430 million in total funding reflects the scale of the mental health access problem and the commercial opportunity for platforms that can sustainably connect patients with in-network providers at scale.

Iterative Health — $1.4 Billion

Iterative Health is a medical research company focused on gastroenterology and the digestive system. Founded in 2017, it raised a $75 million Series C at a $1.4 billion valuation, with total funding exceeding $270 million from investors including Insight Partners and Obvious Ventures.

The company develops AI-powered tools that assist gastroenterologists in detecting polyps and other gastrointestinal abnormalities during colonoscopies, as well as clinical research software that helps pharmaceutical companies run trials in digestive disease. This dual focus on clinical decision support and research infrastructure creates a defensible position across the care pathway.

Key Takeaway: Iterative Health's combination of AI diagnostic tools and clinical research software creates a recurring revenue model that spans both the hospital and the pharmaceutical industry, providing resilience across market cycles.

Pomelo Care — $1.7 Billion

Pomelo Care provides virtual maternity care services to pregnant women and new mothers, particularly those in underserved communities. Founded in 2021, the company raised a $92 million Series C at a $1.7 billion valuation, with total funding exceeding $170 million from Andreessen Horowitz and First Round Capital.

Maternal mortality rates in the United States remain higher than in most comparable high-income countries, with stark racial and geographic disparities. Pomelo uses a combination of virtual visits, remote monitoring, and care coordination to reach patients who lack access to high-quality obstetric care in their local communities. Payers, including Medicaid managed care organizations, are important customers for this model because preventing high-cost complications from poor prenatal care aligns directly with their financial incentives.

Key Takeaway: Pomelo Care represents a category of healthcare unicorns that are solving both a public health problem and a commercial opportunity: reducing the cost of preventable maternal complications is one of the clearest value propositions in healthcare.

Garner — $1.4 Billion

Garner uses data science to help patients find high-quality, cost-effective doctors within their insurance network. Founded in 2019, the company raised a $118 million Series D, bringing total funding to $179 million at a $1.4 billion valuation. Investors include Founders Fund and Redpoint Ventures.

Healthcare quality varies dramatically between physicians and facilities, but most patients lack the data to make informed choices. Garner aggregates clinical outcome data, patient satisfaction metrics, and cost information to produce actionable doctor recommendations. The company distributes its service through employers and health plans, which benefit from directing employees toward higher-quality, lower-cost providers.

Key Takeaway: Garner's data-driven approach to doctor selection addresses a fundamental information asymmetry in healthcare. Its employer channel strategy provides scalable distribution without requiring direct-to-consumer marketing spend.

Midi Health — $1 Billion

Midi Health is a telemedicine platform focused on menopause and perimenopause care, serving a population that has historically been underserved by both primary care and specialist medicine. Founded in 2021, the company raised a $100 million Series D, bringing total funding to more than $250 million at a $1 billion valuation. Investors include GV and Emerson Collective.

Menopausal health has seen growing clinical and commercial attention in recent years as research on hormone therapy has been updated, stigma has reduced, and consumer demand for dedicated care has increased. Midi combines virtual consultations with dedicated clinicians who specialize in menopause and perimenopause, along with pharmacy integration for prescription management.

Key Takeaway: Women's health, and menopausal care specifically, is generating significant venture investment in 2026. Midi Health's Series D at a $1 billion valuation reflects a mainstream investor recognition that this population represents a large, underserved market with strong willingness-to-pay.

Solace — $1 Billion

Solace is a healthcare marketplace that connects patients navigating complex medical situations with professional patient advocates. Founded in 2022, the company raised a $130 million Series C at a $1 billion valuation, with total funding exceeding $200 million from investors including Menlo Ventures.

The American healthcare system is notoriously difficult for patients to navigate, particularly those dealing with chronic conditions, insurance disputes, or care coordination across multiple specialists. Solace's advocates work on behalf of patients to resolve claims issues, coordinate appointments, and ensure patients understand and can access the care they are entitled to receive.

Key Takeaway: Patient advocacy as a commercial service reflects the growing complexity of healthcare navigation. Solace's marketplace model has the potential to scale through employer benefits platforms, making it a natural addition to the growing suite of workplace health benefits.

Fintech and Crypto Unicorns of 2026

Financial technology and cryptocurrency companies account for a meaningful portion of the 2026 unicorn class. While some of these companies are straightforward fintech plays, others blur the line between financial infrastructure and technology platform, reflecting the maturation of the crypto asset class as an institutional category.

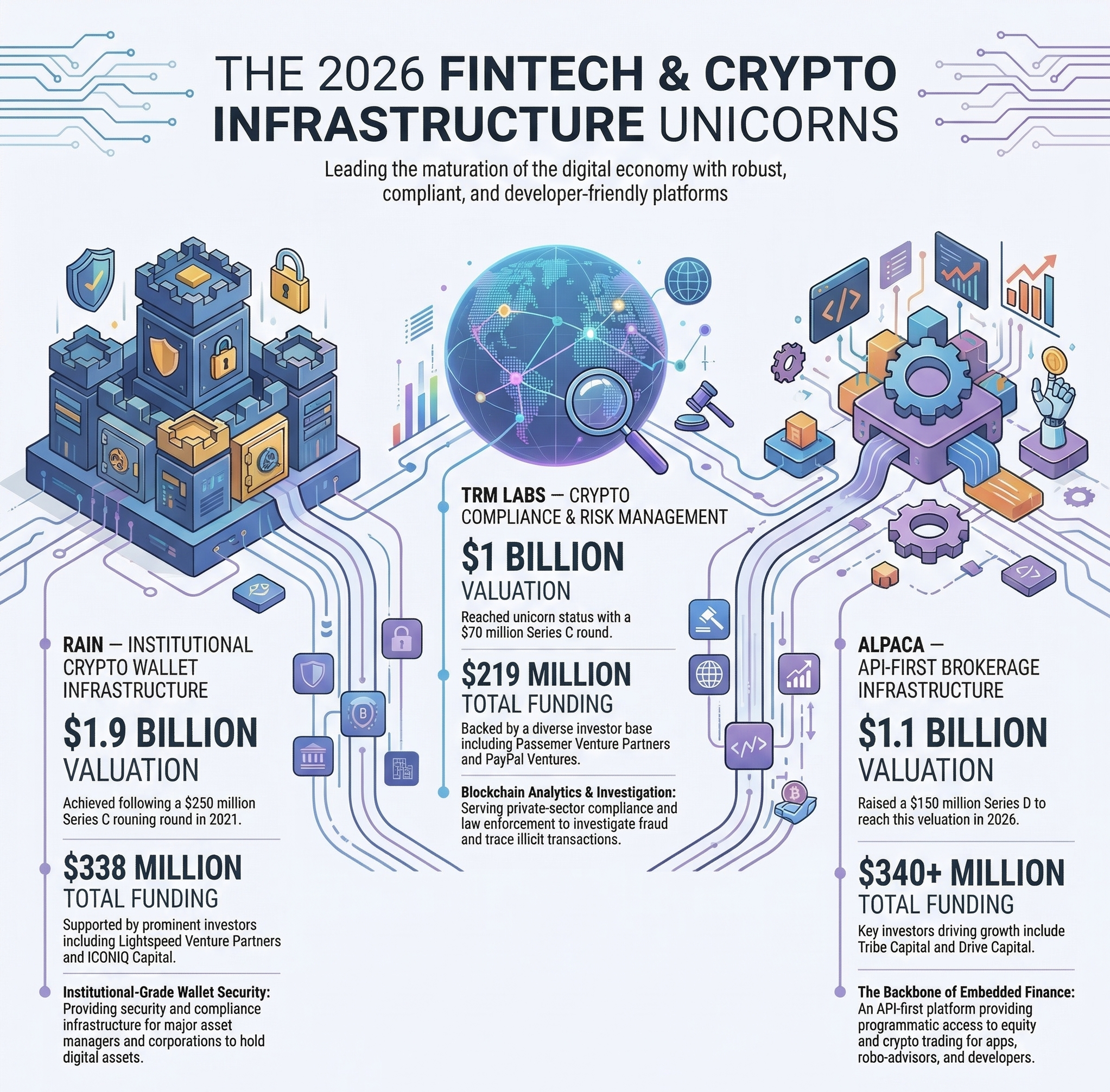

Rain — $1.9 Billion

Rain is a crypto wallet company founded in 2021 that raised a $250 million Series C at a $1.9 billion valuation, bringing total funding to $338 million. Investors include Lightspeed Venture Partners and ICONIQ Capital.

Crypto wallet infrastructure is becoming an increasingly institutional category as major asset managers, banks, and corporations seek to hold and transact in digital assets. Rain's focus on institutional-grade wallet security and compliance positions it to serve this growing segment of the market.

Key Takeaway: Crypto wallet infrastructure is no longer just a retail product. Rain's institutional investor base and Series C scale signal a maturing market where custody and transaction infrastructure attract serious financial capital.

TRM Labs — $1 Billion

TRM Labs helps crypto businesses investigate fraud, trace illicit transactions, and comply with anti-money laundering regulations. Founded in 2018, the company raised a $70 million Series C at a $1 billion valuation, with total funding of approximately $219 million from investors including Bessemer Venture Partners and PayPal Ventures.

As cryptocurrency adoption grows and regulatory pressure on the industry increases globally, compliance infrastructure has become a critical need for exchanges, custodians, and other crypto businesses. TRM Labs occupies a defensible niche by serving both private-sector compliance teams and law enforcement agencies with blockchain analytics and investigation tools.

Key Takeaway: Crypto compliance infrastructure is a growing category within the fintech unicorn class. TRM Labs' dual customer base of private-sector compliance teams and government agencies provides a defensible and diversified revenue model.

Alpaca — $1.1 Billion

Alpaca is an API-first brokerage platform that provides programmatic access to equity and crypto trading for developers and financial technology companies. Founded in 2013, it raised a $150 million Series D at a $1.1 billion valuation, with total funding exceeding $340 million from investors like Tribe Capital and Drive Capital.

The rise of embedded finance and the proliferation of fintech applications requiring brokerage access have created strong demand for developer-first trading infrastructure. Alpaca serves the growing ecosystem of apps, robo-advisors, and automated trading systems that need reliable, compliant, and flexible market access without building a full brokerage operation in-house.

Key Takeaway: API-first brokerage infrastructure is the backbone of the embedded finance movement. Alpaca's developer-first positioning means it benefits from the growth of every fintech application that needs trading functionality.

Enterprise Software and Cloud Infrastructure Unicorns of 2026

Enterprise software and cloud infrastructure remain foundational categories for new unicorn formation. The 2026 class includes companies building private cloud data centers, accounting automation tools, cloud hosting platforms optimized for AI workloads, and workforce management software. These businesses tend to have more predictable revenue models than research-stage AI companies, which contributes to investor confidence in their valuations.

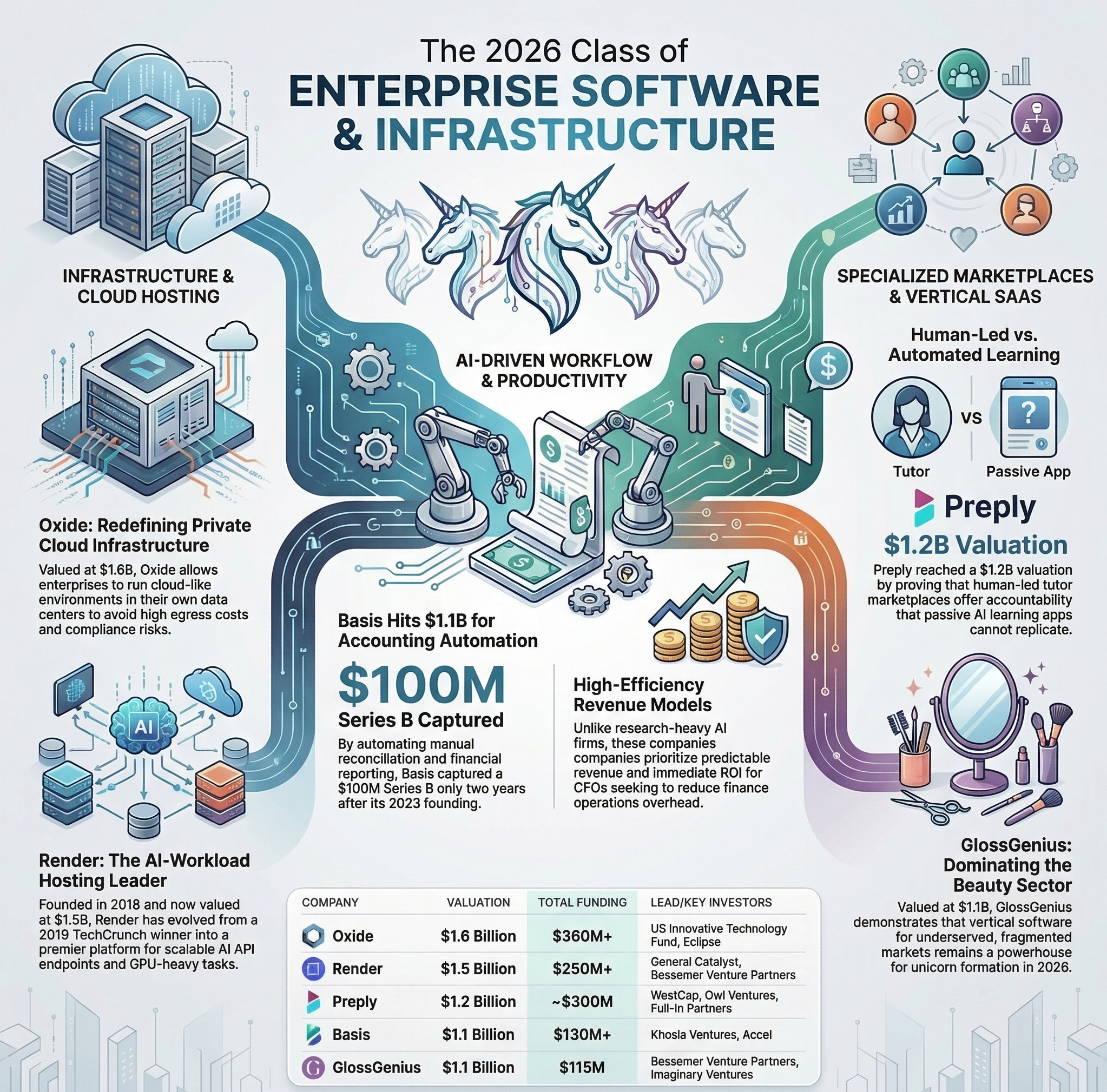

Oxide — $1.6 Billion

Oxide builds private cloud infrastructure that allows companies to run cloud-like computing environments inside their own data centers. Founded in 2019, the company raised a $200 million Series C, bringing total funding to more than $360 million at a $1.6 billion valuation. Investors include the US Innovative Technology Fund and Eclipse.

The market for on-premise cloud infrastructure is driven by regulatory requirements, latency sensitivity, and cost management for large-scale workloads. Oxide targets enterprises that want the developer experience and operational efficiency of public cloud without the data egress costs, latency, or compliance risks of hosting sensitive workloads outside their facilities.

Key Takeaway: Private cloud infrastructure is capturing renewed investment attention as enterprises confront the cost and compliance limitations of public cloud at scale. Oxide's hardware-software integration approach creates strong switching costs and long customer relationships.

Render — $1.5 Billion

Render is a cloud application hosting platform founded in 2018, designed specifically for modern web applications and AI-powered workloads. The company raised a $100 million Series C1 round, bringing total funding to more than $250 million at a $1.5 billion valuation. Investors include General Catalyst and Bessemer Venture Partners. Render won the TechCrunch Startup Battlefield competition in 2019.

Render has built a strong reputation in the developer community for its simplicity and reliability. As AI workloads become a larger proportion of total cloud computing demand, platforms that can handle the specific requirements of AI applications, including GPU availability, fast inference, and scalable API endpoints, are gaining preference over generic cloud providers.

Key Takeaway: Developer-first cloud hosting platforms are benefiting directly from the AI application boom. Render's positioning at the intersection of developer experience and AI workload support gives it a natural growth vector as AI application development accelerates.

Basis — $1.1 Billion

Basis automates accounting workflows for enterprises using AI, reducing the time and manual effort required for financial reporting, reconciliation, and compliance tasks. Founded in 2023, the company raised a $100 million Series B at a $1.1 billion valuation, with total funding exceeding $130 million from Khosla Ventures and Accel.

Accounting automation is one of the most clearly defensible applications of AI in the enterprise context, with obvious ROI and strong buyer intent from CFOs seeking to reduce headcount costs in finance operations. Basis sits at the intersection of AI capability and financial workflow, a combination that has proven commercially attractive to investors.

Key Takeaway: AI-powered accounting automation is capturing genuine enterprise budgets, not just proof-of-concept interest. Basis's Series B trajectory suggests that finance teams are willing to pay premium prices for reliable AI-driven workflow automation.

GlossGenius — $1.1 Billion

GlossGenius provides appointment scheduling, payment processing, and business management software for salon and beauty service businesses. Founded in 2015, the company raised a $44 million Series D at a $1.1 billion valuation, with total funding of approximately $115 million from Bessemer Venture Partners and Imaginary Ventures.

The beauty and personal services sector is large, fragmented, and composed predominantly of small businesses with limited technology adoption. GlossGenius has built a vertically integrated software platform that handles the full operational stack for these businesses, from client booking to payroll, creating strong retention and an embedded payments revenue stream.

Key Takeaway: Vertical software for the beauty industry demonstrates that non-AI, non-crypto companies can still achieve unicorn valuations in 2026 when they build defensible platforms for large, underserved markets. GlossGenius's embedded payments model creates durable revenue beyond software subscriptions.

Preply — $1.2 Billion

Preply is a language learning marketplace that connects students with professional tutors for live online lessons. The company raised a $150 million Series D at a $1.2 billion valuation, led by WestCap, with total funding of nearly $300 million from investors including Owl Ventures and Full-In Partners.

Language learning has proven to be a resilient and growing market, with both individual learners and corporate training programs representing significant demand. Preply's tutor marketplace model creates a two-sided network with high engagement and measurable learning outcomes, differentiating it from passive language learning apps.

Key Takeaway: Human-led language instruction retains strong commercial value even in an era of AI-powered language tools. Preply's live tutoring model addresses the accountability and interactive feedback that self-directed learning products cannot replicate.

Space, Energy, and Physical Infrastructure Unicorns of 2026

Some of the most intriguing companies in the 2026 unicorn class are those operating at the physical frontier: companies that mine raw materials in orbit, manufacture home battery storage systems, develop wireless tracking technology, and build cloud infrastructure hardware. These businesses tend to require larger capital investments and longer development timelines than pure software companies, but the technological moats they create are correspondingly deeper.

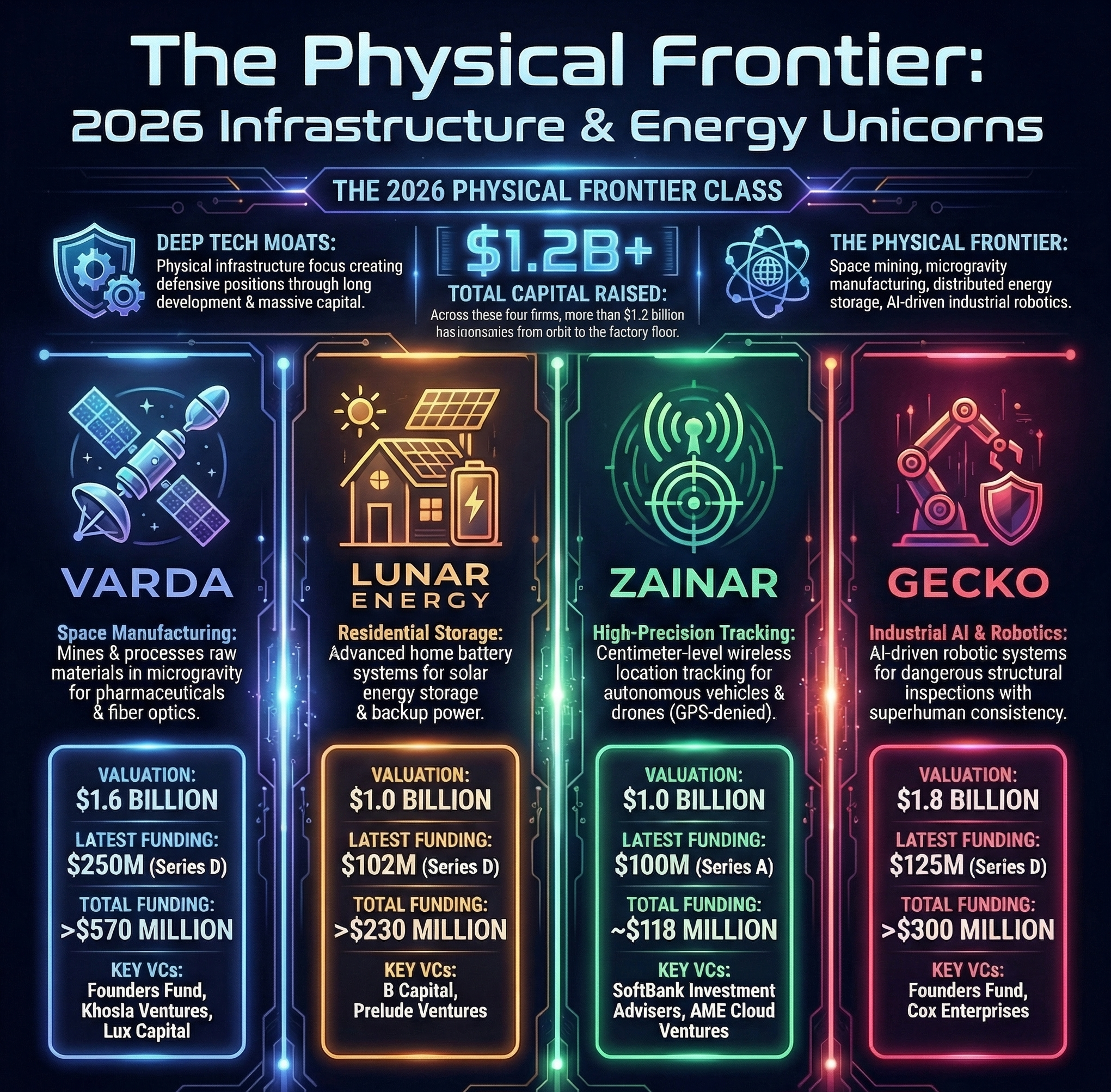

Varda — $1.6 Billion

Varda is a space manufacturing company that mines and processes raw materials in microgravity conditions for commercial use on Earth. The company raised a $250 million Series D at a $1.6 billion valuation, with total funding exceeding $570 million from Founders Fund, Khosla Ventures, and Lux Capital.

Microgravity manufacturing offers unique properties for certain materials, including pharmaceuticals and fiber optics, that cannot be replicated in Earth-based production environments. Varda has already demonstrated the ability to manufacture pharmaceutical compounds in orbit and return them to Earth, a milestone that validates the commercial viability of its model.

Key Takeaway: Varda's successful in-orbit manufacturing demonstrates that space as an industrial environment is no longer theoretical. The company's investor base, which includes multiple top-tier funds, reflects confidence that commercial demand for microgravity-manufactured products will scale.

Lunar Energy — $1 Billion

Lunar Energy makes battery systems for homeowners to store solar energy generated on their properties. Founded in 2020, the company raised a $102 million Series D, bringing total funding to more than $230 million at a $1 billion valuation. Investors include B Capital and Prelude Ventures.

Home energy storage is a growing market driven by the proliferation of residential solar installations, rising electricity prices, and increasing grid instability in many parts of the United States. Lunar Energy's systems are designed to integrate seamlessly with existing solar installations and provide backup power during outages, making them attractive to homeowners in markets with frequent disruptions or high peak electricity pricing.

Key Takeaway: Home battery storage is transitioning from a luxury product to a mainstream component of residential energy management. Lunar Energy's $230 million in total funding reflects investor confidence in the growth of distributed energy infrastructure.

ZaiNar — $1 Billion

ZaiNar provides wireless location tracking technology for physical assets including vehicles, drones, and industrial equipment. Founded in 2017, the company raised a $100 million Series A at a $1 billion valuation, with total funding of approximately $118 million from SoftBank Investment Advisers and AME Cloud Ventures.

The proliferation of autonomous and semi-autonomous physical systems requires reliable, high-precision location infrastructure that GPS alone cannot always provide, particularly in indoor or GPS-denied environments. ZaiNar's wireless tracking technology addresses this gap, offering centimeter-level accuracy using existing wireless infrastructure.

Key Takeaway: Wireless asset tracking is foundational infrastructure for the autonomous systems economy. ZaiNar's technology is positioned to benefit from the growing deployment of drones, autonomous vehicles, and industrial robots across multiple industries.

Gecko — $1.8 Billion

Gecko is an AI and robotics company founded in 2013 that raised a $125 million Series D at a $1.8 billion valuation, with total funding exceeding $300 million from Founders Fund and Cox Enterprises.

Gecko applies AI-driven robotic systems to industrial inspection and maintenance tasks in environments that are difficult or dangerous for human workers, including energy infrastructure, structural inspection, and industrial facilities. The combination of machine vision, robotic mobility, and AI processing allows Gecko's systems to detect defects and anomalies with greater consistency than human inspectors.

Key Takeaway: Industrial AI robotics for inspection and maintenance addresses a genuine safety and cost challenge in critical infrastructure sectors. Gecko's long operating history gives it an advantage in the safety certifications and regulatory approvals that new entrants must navigate.

Patterns and Themes Driving the 2026 Unicorn Class

Looking across the full list of 2026 unicorns, several patterns emerge that are worth examining for anyone trying to understand where venture capital is flowing and why.

The AI Layer Cake

Investors are funding AI companies at every layer of the technology stack simultaneously. This includes chips and compute infrastructure, foundational model labs, application layer tools, and the governance and interpretability tools needed to audit AI behavior. The breadth of this investment suggests that the market is treating AI not as a single product category but as a general-purpose technology that requires infrastructure investment at multiple levels.

Healthcare's Persistent Appeal

Healthcare companies continue to generate unicorn outcomes at a rate that rivals pure technology. The 2026 class includes companies in psychiatric care, maternity health, digestive disease, women's health, and patient navigation. What unites these companies is a common challenge: the existing healthcare system leaves large populations underserved, and technology-enabled models can reach these populations more cost-effectively than traditional care delivery.

The Crypto Infrastructure Maturation

Several 2026 unicorns are building infrastructure for the crypto industry rather than speculative products. Compliance tools, banking services, and wallet infrastructure are attracting institutional venture capital. This reflects a broader maturation of the crypto industry as a regulated sector requiring the same compliance and financial infrastructure as any other part of the financial system.

Physical World Applications

A striking feature of the 2026 class is the number of companies applying AI and advanced technology to physical-world problems: construction site automation, humanoid robots, space manufacturing, home energy storage, industrial inspection robotics, and wireless asset tracking. The shift from purely digital applications to physical-world deployments represents a significant evolution in the types of problems that venture-backed startups are tackling.

Founder Age and Speed

Research from venture capital firm Antler published in early 2026 noted that the average age of AI unicorn founders has dropped significantly in recent years. Young founders are achieving unicorn valuations faster than any previous generation, driven by their ability to build leaner teams and iterate more quickly using AI-powered development tools. This pattern is visible across the 2026 class, where several companies have achieved billion-dollar valuations within one to two years of founding.

Key Takeaway: The 2026 unicorn class is defined by three intersecting forces: the AI revolution creating investable companies at every layer of the stack, persistent healthcare demand creating a large addressable market for technology-enabled care delivery, and the maturation of crypto into a regulated financial infrastructure sector.

Frequently Asked Questions About 2026 Unicorn Startups

What is the difference between a unicorn, a decacorn, and a hectocorn?

A unicorn is a privately held startup valued at $1 billion or more. A decacorn is valued at $10 billion or more, and a hectocorn is valued at $100 billion or more. The 2026 class includes companies ranging from exactly $1 billion to $5.3 billion in the data covered here, making them all unicorns. Some AI companies founded earlier, such as OpenAI, Anthropic, and xAI, have reached decacorn or hectocorn status.

How is a startup valuation determined at the time of a funding round?

Startup valuations are negotiated between founders and investors as part of each funding round. The post-money valuation is calculated by dividing the investment amount by the ownership percentage the investor receives. These valuations reflect investor expectations about future revenue and growth rather than current financial performance, which is why seed-stage companies can achieve billion-dollar valuations based on team quality and market opportunity alone.

Which sectors are producing the most new unicorns in 2026?

Artificial intelligence and machine learning produce the largest share of new unicorns in 2026, followed by healthcare and life sciences, fintech and crypto infrastructure, and enterprise software. Physical-world technology including robotics, energy storage, and space applications represents a growing share of the unicorn class compared to previous years.

Do all unicorn startups eventually go public or get acquired?

Not all unicorns achieve a successful exit. Some remain private for many years, some are acquired by larger companies, some go public through IPOs or direct listings, and some fail entirely. Achieving a unicorn valuation is a milestone in a company's fundraising history, not a guarantee of eventual commercial success. The gap between valuation and revenue can be substantial, particularly for early-stage companies that have raised large seed or Series A rounds.

What is Generative Engine Optimization and why is Profound valued at $1 billion?

Generative Engine Optimization, or GEO, refers to the practice of optimizing content and digital presence to appear in AI-generated search responses, including Google's AI Overviews, ChatGPT, and similar platforms. As these AI systems intercept an increasing share of search traffic, traditional SEO strategies that focus on ranking web pages in blue-link results are becoming less effective. Profound provides analytics and optimization tools that help marketers understand and improve their brands' visibility in AI search environments.

Conclusion: What the 2026 Unicorn Class Tells Us About the Next Decade

The nearly 40 unicorn startups minted in the first three months of 2026 represent more than a list of impressive valuations. They offer a window into where the technology economy is heading: toward AI systems that work across every industry, healthcare models that use data to close access gaps, crypto infrastructure that meets institutional compliance standards, and physical-world applications that were unimaginable a decade ago.

For founders, the 2026 class provides a map of the areas where investors have the most conviction. AI infrastructure at every layer, vertical healthcare platforms serving underserved populations, developer-first software tools, and physical-world robotics are all attracting significant capital. Companies that can demonstrate early commercial traction in these areas are finding receptive investor audiences even at early stages of development.

For investors, the class illustrates both the opportunity and the risk of the current moment. Seed-stage AI research labs are achieving valuations that would have required years of revenue in previous cycles. Some of these bets will produce transformative returns; others will not. The discipline of identifying which teams, technologies, and business models can translate early funding into durable revenue will define the returns of 2026 vintages for years to come.

For everyone else, the 2026 unicorn class is a reminder that the technology transformation underway is broader and deeper than any single trend. It is reshaping how humans receive medical care, how buildings get constructed, how satellite constellations are managed, how companies protect their financial systems, and how the energy needs of homes are met. The billion-dollar companies being built today are building the infrastructure of the economy that will exist in ten years.

Data sources: PitchBook, Crunchbase, TechCrunch. This post will be updated throughout 2026 as additional companies achieve unicorn status.