Why the European Deep Tech Ecosystem Is Quietly Becoming a Global Force

The European deep tech ecosystem has reached $690 billion in enterprise value and now captures 32 percent of all venture capital on the continent. Understanding where capital is flowing, which sectors are surging, and what structural gaps remain is essential for founders, investors, and policymakers who want to compete at the frontier of science-driven innovation.

|

$690bn Total enterprise value of

European deep tech |

$20.3bn VC invested in 2025 — all-time

high |

32% Share of all European VC, up

from 15% in 2015 |

125 Unicorns and $1bn+ exit

outcomes |

The European deep tech ecosystem is not emerging — it has already arrived. At $690 billion in combined enterprise value, with 125 companies that have achieved unicorn status or a $1 billion-plus exit, and with science-based startups now attracting nearly a third of all European venture capital, this is a mature, compounding asset class that is reshaping how the continent thinks about innovation, sovereignty, and long-term growth. The quiet part is simply that most of the world has not been paying attention.

The numbers tell a story that cuts against several prevailing narratives. Deep tech funding in Europe has proven more durable than regular technology investment: while regular tech remains 54 percent below its 2021 peak, deep tech is just 4 percent off that same high. Defence, space, quantum computing, and computational biology are attracting capital at record levels. The ecosystem that once struggled to retain its best founders is now generating a flywheel — successful companies cycling operators, capital, and credibility back into the next generation of startups.

This analysis examines the full picture: the talent base, the capital flows, the seven sectors drawing the most investment, the misconceptions that continue to mislead, and the four structural challenges that will determine whether Europe builds truly generation-defining companies or continues exporting its breakthroughs to US acquirers.

What Deep Tech Actually Means — and Why Definitions Matter

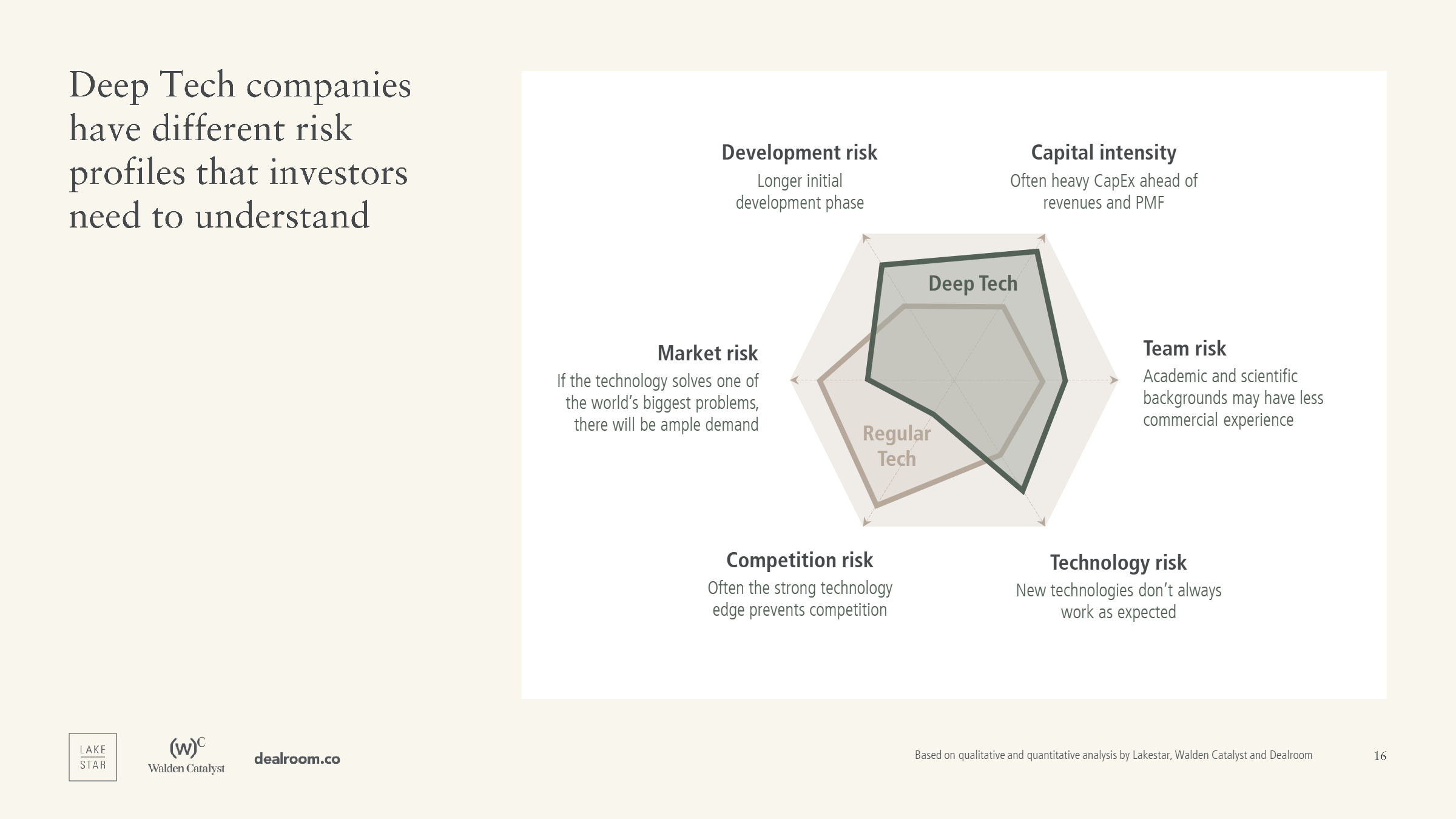

Deep tech is defined by a single distinguishing feature: it involves novel scientific or engineering breakthroughs making their way into commercial products for the first time. This distinguishes it sharply from software-first, or "shallow tech," companies that build on existing infrastructure, commoditised tools, and rapidly replicable code. A deep tech company is building something that did not exist before — not a new interface over an existing database, but a new class of material, a new mode of computation, or a new biological mechanism translated into a therapeutic.

The distinction has become substantially more consequential in the past two years, as generative AI tools have eroded the defensibility of pure software businesses. If an AI model can replicate the core functionality of a software product within weeks of its launch, the moat that software businesses traditionally relied on becomes dramatically thinner. In February 2026, commentary from a major US technology company's earnings call suggesting that AI agents make traditional SaaS products obsolete wiped $300 billion from listed software company valuations in a single session. Deep tech faces no equivalent threat. Generative AI cannot manufacture a next-generation semiconductor, commission a fusion pilot plant, or synthesise a novel compound — each requires investment that becomes a source of defensibility no amount of better code can replicate.

Deep tech progress moves in waves that define eras and create — and destroy — generational companies. The personal computer wave reached one billion users in 36 years. Smartphones did it in 32. The internet in 25. Generative AI in three months. The present moment is characterised by a convergence of disciplines: quantum computing, photonics, advanced materials, computational biology, and autonomous systems are all maturing simultaneously, driven by decades of publicly funded basic research now crossing the threshold from laboratory validation into commercial application.

The European Opportunity: Talent, Capital, and Market Demand

Scientific Talent

Europe's scientific talent base is extraordinary by any objective measure. The continent produces 1.5 million STEM graduates per year — more than double the output of the United States — and is home to 2.15 million researchers in full-time equivalent terms. Approximately 40 percent of EU doctoral students are in science and technology fields. Europe accounts for 19.2 percent of the world's top-10 percent most-cited scientific papers, nearly on par with the US, and generates 21.8 percent of international patent applications, second only to Asia. Thirty percent of the world's top deep tech universities by subject ranking are European institutions.

The Deep Tech Flywheel

The commercial talent ecosystem has matured considerably alongside the scientific base. The number of people working in tech in Europe has grown at a compound annual rate of 9.1 percent over the past decade, reaching 4.6 million in 2025. The "deep tech flywheel" — the feedback cycle by which successful companies produce experienced founders, operators, and investors who reinvest their knowledge and capital into the next generation — is now visibly turning. DeepMind offers the clearest case study: founded in London in 2010, acquired by Google in 2014, awarded the Nobel Prize in chemistry in 2024, with alumni going on to found companies that have collectively raised over $5 billion and created $23 billion in enterprise value.

|

Europe has the science. What it has lacked is the

industrial discipline to turn that science into enduring companies. That is

changing. A new cohort of founders is building for structural necessity, not

convenience. Simon King, Partner at Lakestar |

Market Opportunity and Public Capital

Geopolitical forces have made technological sovereignty a policy priority. Macroeconomic shocks — the COVID-19 pandemic, the Russian invasion of Ukraine, US tariff policy, and the acceleration of Chinese industrial capability — have demonstrated with painful clarity the cost of strategic dependency on foreign technology and supply chains. Governments have responded: the EuroHPC joint undertaking targeting EUR 7 billion to 2027, France's EUR 109 billion five-year AI and data centre investment programme, the EU Chips Act directing EUR 43 billion toward semiconductor production by 2030, Germany's EUR 35 billion space investment commitment, and an expected EUR 20 billion or more per year in European deep tech through expanded defence spending. Getting this right could unlock a USD 1 trillion economic growth opportunity by 2030.

The Capital Environment

European deep tech VC funding reached $20.3 billion in 2025, an all-time high share of 32 percent of all European venture capital — more than double the 15 percent share of 2015. The total enterprise value of VC-backed European deep tech companies has reached $690 billion, up from $73 billion in 2015. Deep tech has proven more resilient than regular tech: it is just 4 percent below its 2021 peak, while regular tech remains 54 percent below that same high.

The Funding Landscape: Where Capital Is Flowing

Countries and Cities

The UK attracted the most deep tech funding in 2025 at $5.2 billion, followed by France at $3.9 billion and Germany at $3.2 billion. Finland, Sweden, and Switzerland lead in terms of the proportion of total VC investment going to deep tech. At city level, Paris has become the top European hub at $3 billion, ahead of London at $2.2 billion and Munich at $1.8 billion. Munich has an explicit dominance in space, defence, and robotics, driven by the concentration of technical talent around TUM and UnternehmerTUM. Paris, Cambridge, London, Munich, Stockholm, and Zurich all rank in the global top 20 deep tech hubs when measured by a combination of VC investment, enterprise value, unicorns, university linkages, and patents.

The Seven Segments

Across the seven major segments, the funding story is one of broad acceleration with several remarkable standouts. Defence grew 125 percent year on year to $1.8 billion. Future of Compute — led by quantum computing — more than doubled to $2.5 billion. Computational Biology and Chemistry surged 88 percent to $1.1 billion. Novel Robotics grew 64 percent to $468 million. Novel AI grew 27 percent to $3.4 billion. Space Tech grew 22 percent to $1.3 billion. Novel Energy was the sole decliner at negative 41 percent to $700 million, reflecting concentration effects rather than diminished interest in the long-term thesis.

|

Segment |

2025 Funding |

Key Companies & Growth Drivers |

|

Novel AI +27% YoY |

$3.4bn |

Foundational models

(Mistral), vision and voice generation (Synthesia, ElevenLabs), AI-driven

engineering (PhysicsX), and world models. Growth driven by sovereign European

AI development and AI agent orchestration. |

|

Future of Compute +115% YoY |

$2.5bn |

Quantum computing hardware

and software (Quantinuum, IQM, Multiverse Computing), photonic chips (Q.ANT),

non-volatile memory. Europe controls a large portion of the global quantum

supply chain. |

|

Defence +125% YoY |

$1.8bn |

AI autonomy (Helsing),

surveillance drones (Quantum Systems), air defence systems. Now 43% of all

European deep tech funding, up from 20% in 2022. Structural shift, not a

cyclical spike. |

|

Space Tech +22% YoY |

$1.3bn |

Earth observation (ICEYE),

launch vehicles (Isar Aerospace), small satellite manufacturing (EnduroSat).

Munich leads. Debris removal and in-orbit servicing are next-stage growth

areas. |

|

CompBio & Chemistry +88% YoY |

$1.1bn |

AI-driven drug discovery

(Isomorphic Labs), materials discovery (CuspAI), foundational biology models

(Bioptimus). Shift to in silico design is compressing pharma development

timelines. |

|

Novel Robotics +64% YoY |

$468m |

Cognitive robotics and

humanoids (Neura Robotics), general-purpose robotic intelligence (Genesis AI,

Flexion Robotics). Wide industrial unlock expected within two to three years

as VLA models mature. |

|

Novel Energy -41% YoY |

$700m |

Nuclear fusion (Proxima

Fusion, Marvel Fusion, Renaissance Fusion), small nuclear reactors. Decline

reflects concentration effects. European energy sovereignty thesis remains

compelling long-term. |

One structural shift deserves particular attention: defence, security, and resilience now accounts for 43 percent of all European deep tech VC funding, up from 20 percent in 2022. This is a structural re-architecture of European industrial strategy — moving from hardware-heavy arsenals toward software-defined capabilities including AI autonomy, drone systems, autonomous command and control, space sovereignty, and advanced manufacturing. Europe's total defence spending is projected to reach nearly EUR 970 billion by 2030.

On quantum and photonics, Europe holds a globally enviable position — capturing 89 percent of global VC funding in quantum cryptography and 49 percent in quantum computing software. The gap with the US requires an important qualification: more than 50 percent of the US deep tech total went to just three foundational AI model companies. Strip that out, and the rest-of-deep-tech gap narrows to roughly 2:1, which is meaningful but far more competitive than headline numbers suggest.

EXCLUSIVE RESEARCH REPORT

The Full Data Is Hidden Inside 242 Pages Most Founders Have Never Read

The 2026 European Deep Tech Report contains complete segment-by-segment funding breakdowns, full country and city rankings, the Deep Tech Compass investor criteria from Seed to Series C, a ready-to-use data room template, and the only verified analysis comparing deep tech fund returns against traditional tech portfolios. The summary above covers the surface. The report goes far deeper.

What you get inside the full report:

✓ Complete funding data for all 7 deep tech segments, with YoY growth and deal-level examples

✓ The Deep Tech Compass: exactly what investors want to see at Seed, Series A, and Series B

✓ Grant funding map: EIC, ERC, EIT, and Horizon Europe pathways plotted by TRL stage

✓ Verified IRR data comparing deep tech fund returns to traditional tech benchmarks (2003-2020)

✓ European city and country rankings with per-capita funding analysis across 43 countries

HOW TO GET YOUR FREE COPY

Visit deeptech.report/2026 and enter your work email address. The full 242-page PDF is delivered instantly, free of charge, with no paywall and no credit card required. Over 12,000 founders, investors, and policymakers have already downloaded it.

No spam. Unsubscribe at any time. Data handled in line with GDPR.

The Late-Stage Funding Gap: Europe's Most Pressing Structural Problem

The most consequential structural problem in the European deep tech ecosystem is the near-total absence of growth-stage capital sourced from within Europe. Seventy percent of late-stage funding for European deep tech startups comes from non-European investors — primarily from the United States. For rounds of $15 million and above, only 54 percent is funded from within Europe, compared to 80 percent in the equivalent US market. Closing just that domestic share gap to match US levels would require an additional $4 billion per year flowing from European sources into European companies.

The deeper problem is the conversion gap. European deep tech startups convert from one funding round to the next at roughly half the rate of their US counterparts — a gap that is partly caused by the capital scarcity itself. Companies that cannot raise follow-on rounds cannot reach the commercial milestones that would justify follow-on rounds. When forced to raise later-stage capital internationally, they take money from investors whose primary point of reference is the US market, which gradually pulls the geographic centre of mass of the business away from Europe. Closing the full conversion rate gap would require an additional $20 billion per year.

|

Key Data Point Of the 22 VC-backed European

deep tech companies that completed an IPO or SPAC merger above $500 million

in valuation since 2015, 18 listed on US exchanges and just four on European

exchanges. The exit liquidity that funds the next generation of investors is

flowing out of Europe. |

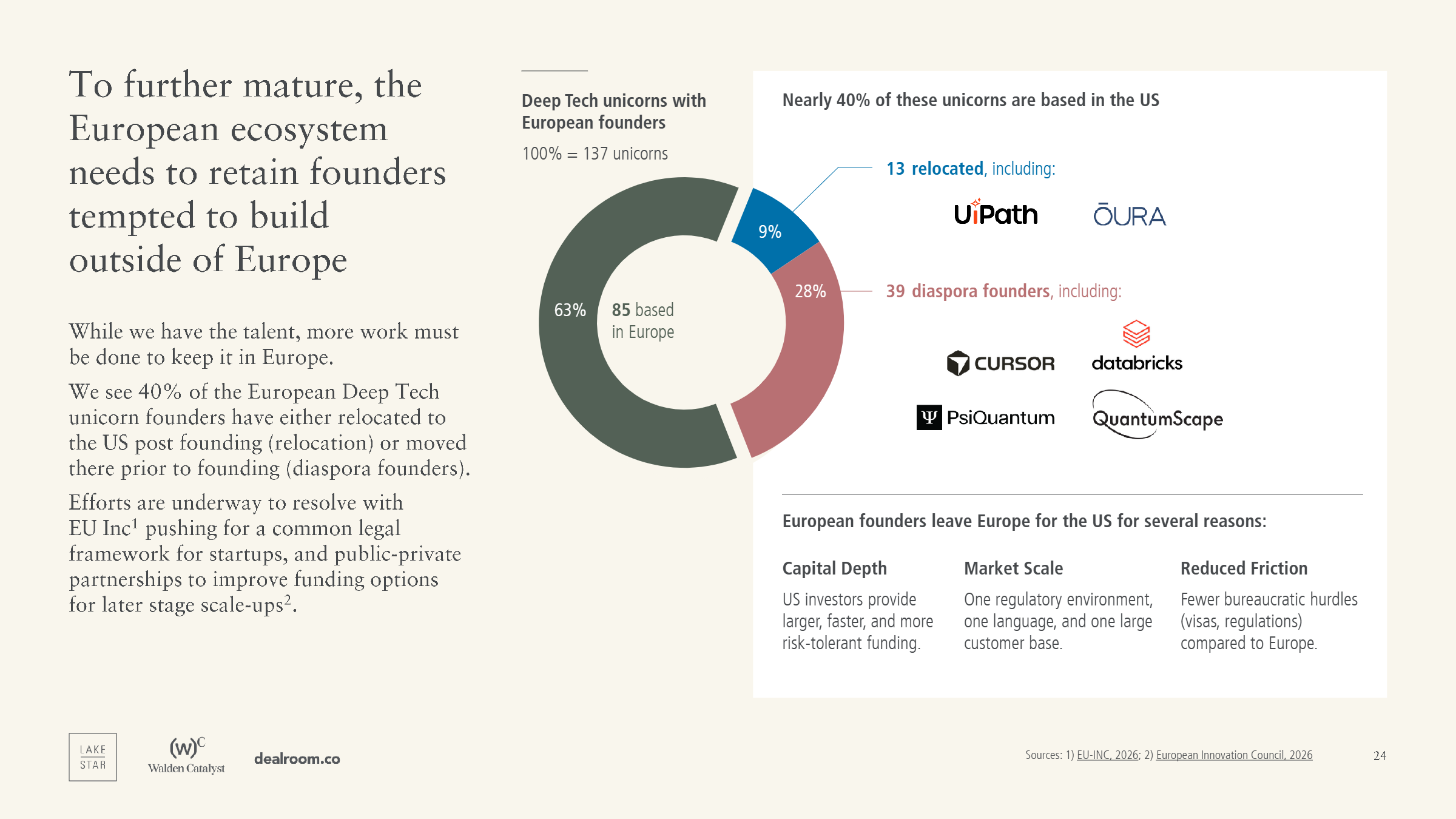

The exit landscape compounds the problem. European deep tech exits are broadly flat and driven more than 80 percent by M&A rather than public listings. By value, the majority of that M&A is captured by US acquirers. Forty percent of European deep tech unicorn founders are now US-based, either having relocated after founding or moved before starting their company. The December 2025 selection of EuroCTP as the EU's first Consolidated Tape Provider for equities is the most significant European capital markets infrastructure development in years — but structural reform needed to make European public markets attractive to high-growth deep tech companies goes considerably further.

Where Deep Tech Founders Come From

Research spinouts account for 33 percent of new European deep tech startups since 2015, with the highest concentration in photonics and quantum technology. The typical European deep tech founder has a technical background, at least a master's degree, is 35 years old, and has either prior startup experience or has worked inside a large corporate in an industrial, consulting, or technology capacity. Just under a quarter have startup experience; a further 21 percent come from blue-chip industrial or corporate environments.

The DeepMind alumni network has become the clearest living demonstration of what a mature deep tech flywheel produces. Founded in London in 2010, acquired by Google in 2014, awarded the Nobel Prize in chemistry in 2024, the company has generated alumni who have collectively founded companies with over $5 billion in cumulative fundraising and $23 billion in enterprise value. Mistral, Isomorphic Labs, and Advanced Machine Intelligence are each now worth more than DeepMind's original acquisition price. This compounding dynamic — where one successful company becomes the seed of ten more — is what European deep tech has lacked at scale historically, and is now beginning to demonstrate.

The gender inclusion challenge remains a significant unresolved problem. Companies with at least one female founder attracted only 14 percent of European deep tech VC funding in 2025 — with no meaningful improvement over eight years. The pipeline of female founders entering deep tech remains limited, the investor community writing the largest cheques remains overwhelmingly male, and the structural interventions needed are still nascent at best.

The Common Misconceptions About Deep Tech Investing

Several persistent beliefs about deep tech as an asset class mislead both founders navigating fundraises and investors allocating capital. The data from the 2026 analysis addresses six of these misconceptions directly.

|

Misconception |

Verdict & Evidence |

|

Do deep tech companies need more capital? Yes — but the

capital builds moats AI cannot replicate. |

YES Capital is invested in

physical assets, IP, and production infrastructure that generative AI cannot

displace. Markets are now rewarding this defensibility. |

|

Do they take longer to generate revenue? True early on,

false at later stages. |

MIXED Time to first $1m revenue is

~4.3 years — broadly similar to regular tech. Capital required is

approximately 2x higher at every revenue milestone. |

|

Do deep tech companies fail more often? No —

conversion rates are broadly equivalent. |

NO Around 5% of deep tech

startups reach Series C from seed — in line with regular tech cohorts from

the same period. |

|

Do they take longer to exit? No — exit

timelines peak at six to seven years. |

NO Exit timelines for both deep

tech and regular tech companies peak at six to seven years from founding. The

profiles are similar. |

|

Do they have larger exits? Inconclusive —

Europe needs more of them. |

UNCLEAR While large outcomes exist,

the majority of M&A value flows to US acquirers. Europe needs deeper

public market and strategic buyer liquidity. |

|

Does deep tech investing deliver top returns? Yes — it has

outperformed traditional tech funds. |

YES Analysis of 115 deep

tech-focused funds shows an average weighted net IRR of 16-17%, vs 10% for

traditional tech funds over the same 2003-2020 period. |

Four Challenges Europe Must Solve

Despite the scale of the opportunity and the momentum behind European deep tech, four structural challenges continue to limit the ecosystem's ability to produce and retain globally competitive companies. Progress on each has been widely acknowledged — but remains modest in practice.

|

01 |

The

Growth-Stage Funding Gap Beyond Series A, there is not enough European capital to

fund businesses locally. Companies raise smaller rounds, sell earlier than

they should, or take overseas capital that shifts their geographic centre of

mass away from Europe. Eighty-seven percent of dedicated deep tech investor

funds in Europe are under $300 million — too small to lead a Series B or

beyond. The yearly funding gap sits between $4 billion and $24 billion. The

Scaleup Europe Fund, targeting EUR 5 billion, is the EU's most significant

attempt to address this — but its first operational activities are only

expected in mid-2026. |

|

02 |

Fragmentation

Across 43 Countries Europe operates across 43 countries with fragmented

regulation, incompatible legal systems, inconsistent employee stock option

frameworks, and no talent clusters with the concentration of Silicon Valley.

Founders building pan-European companies face a compliance burden that US

counterparts never encounter. The EU Inc proposal — adopted by the European

Parliament in 2026 with 492 votes in favour — is the most significant step

toward reducing this friction. But the exact form of implementation remains

unclear, and the gap between political intent and operational reality in

European institutional reform has historically been wide. |

|

03 |

Researcher-to-Founder

Conversion Europe produces exceptional science but converting that

research excellence into commercially oriented startups requires a cultural

shift that has not happened at sufficient scale. Technology Transfer Offices

vary enormously in quality and founder-friendliness across European

institutions. The incentive structures at most universities still reward

publications over patents and spinouts. Commercially experienced operators —

product managers, revenue leaders, growth executives who have scaled

multibillion-dollar companies — remain in shorter supply in Europe than in

the US, and are still largely imported from American companies that have been

through the full cycle. |

|

04 |

Risk Appetite

in Corporates and Government European corporates and government procurement functions

remain systematically risk-averse when it comes to working with unproven

startups. The typical procurement process is designed around established

vendors with years of audited accounts — a standard that disqualifies most

early-stage deep tech companies by definition. Meanwhile, US strategic

acquirers are willing to pay a premium for European deep tech companies

precisely because European corporates have not moved to acquire them first.

The cultural shift required — where allocating a proportion of procurement

budgets to promising but unproven technology is seen as prudent risk

management — is beginning in defence, where existential stakes have

overridden institutional caution. |

The Stakes for the Next Five Years

The European deep tech ecosystem in 2026 sits at a crossroads that the data makes unusually legible. The scientific foundation has never been stronger. The capital environment has never been more active at the early stage. The geopolitical tailwinds driving demand for sovereign technology, local supply chains, and European-controlled critical infrastructure have never been more pronounced. The question is not whether Europe has what it takes to build the next generation of globally significant deep tech companies — the data is clear that it does. The question is whether the structural conditions will improve fast enough to keep those companies in Europe long enough to reach their full potential.

The funding gap, if left unaddressed, continues to create a systematic export of value: breakthroughs developed in European laboratories, with European public funding and European talent, ending up on the balance sheets of US acquirers at the precise moment they become commercially valuable. The Scaleup Europe Fund, the ELTIF 2.0 framework, the EU Inc legal infrastructure, and the expanded EIC mandate are all meaningful steps. But the gap between policy design and operational impact has a long track record in European institutional reform — and the companies that need that capital are making decisions about where to locate and raise right now, not in three years when the next fund cycle closes.

The founding generations of transformative technology companies are determined by windows of opportunity, not by long-run averages. The current convergence of mature quantum hardware, agentic AI systems, autonomous physical systems, and computational biology platforms represents a window of precisely that kind — one that will close as incumbents consolidate and capital concentrates around proven winners. European deep tech has the raw materials to claim a significant share of that window. Whether it does will depend less on the quality of the science than on the speed and coherence of the ecosystem built around it.

Analysis informed by the 2026 European Deep Tech Report | Lakestar | Walden Catalyst | Dealroom | Data cut-off February 2026