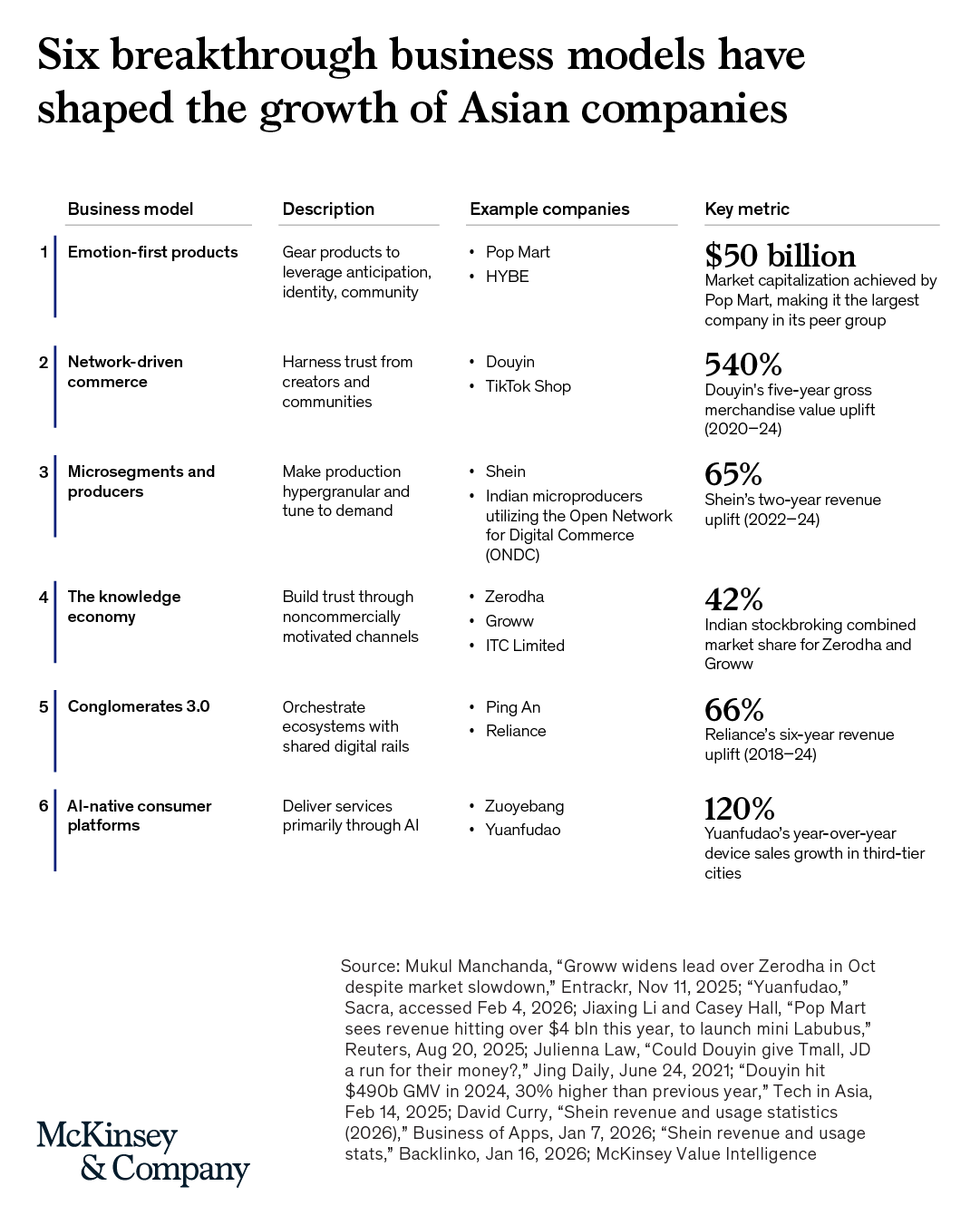

Six Breakthrough Business Models From Asia Reshaping Global Commerce

Asia has become the world's most productive testing ground for next-generation business architecture. Six repeating archetypes, built on trust, emotional resonance, and AI acceleration, are producing compound annual growth rates far above their underlying markets. This guide examines each model in depth, with the mechanisms, case studies, and transferable lessons global leaders need.

Source: McKinsey Strategy & Corporate Finance:

- 60%Projected Fortune 500 share based in Asia within a decade

- 52 ppMax CAGR advantage above the underlying market achieved by breakout Asian firms

- 540%Douyin five-year gross merchandise value uplift, 2020 to 2024

- $50BMarket cap reached by Pop Mart, the largest company in its peer group

Contents

- Why Asia Became the World's Business Model Laboratory

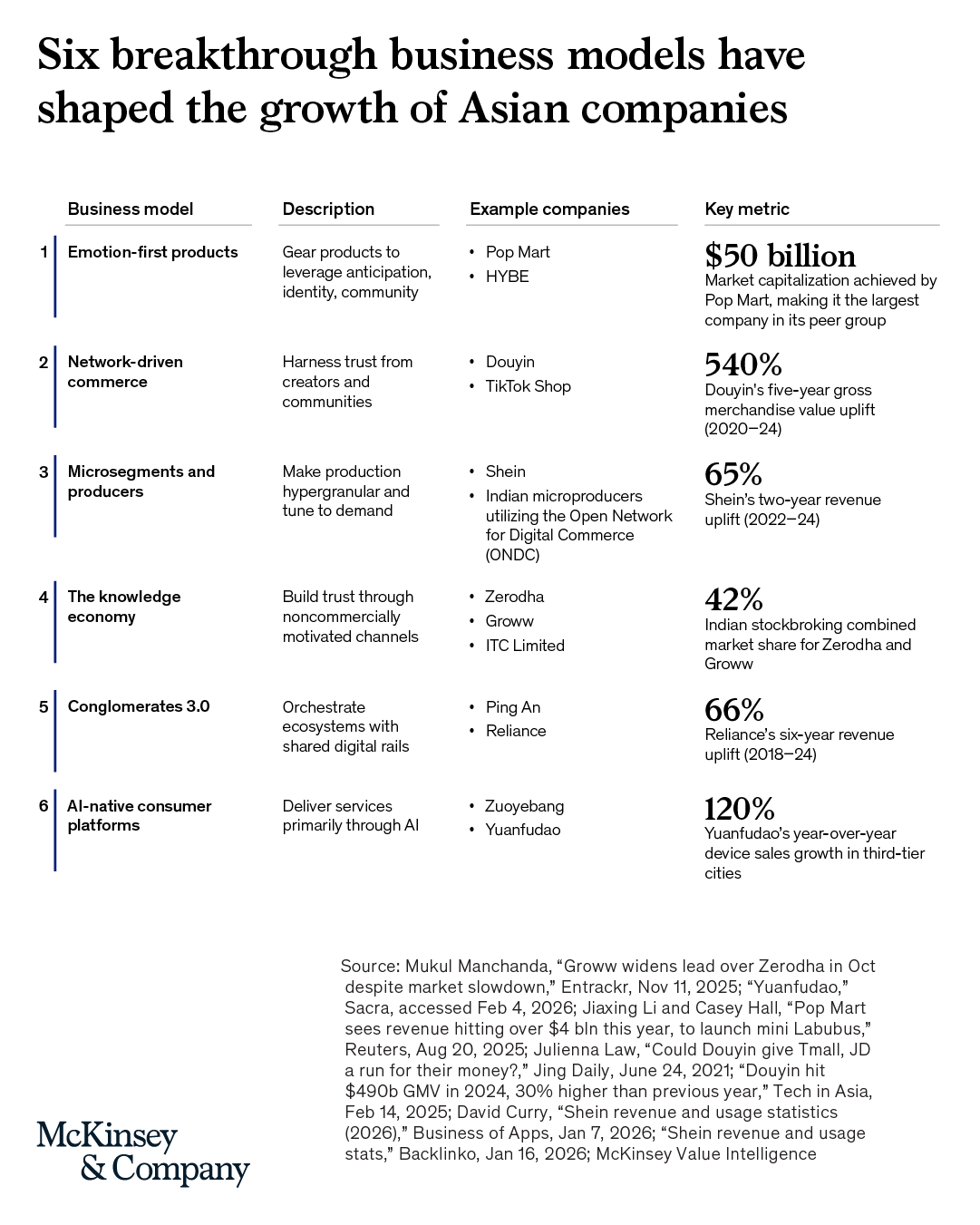

- Model 1: Emotion-First Products

- Model 2: Network-Driven Commerce

- Model 3: Microsegments and Microproducers

- Model 4: The Knowledge Economy

- Model 5: Conglomerates 3.0

- Model 6: AI-Native Consumer Platforms

- Comparison Table: All Six Models

- AI as a Cross-Cutting Accelerant

- Five Transferable Lessons for Global Leaders

Why Asia Became the World's Business Model Laboratory

Something unusual has been happening across Asian markets over the past five years. Companies operating in industries as different as toy retail, financial services, and education technology have been compounding at rates that make traditional growth benchmarks look modest. A stockbroking platform in India grew its active client base faster than any competitor in recorded history. A collectibles brand in China achieved a 180 percent trailing twelve-month revenue CAGR. A fashion retailer lists new styles at a pace that has redefined what the phrase "fast fashion" even means.

What connects these stories is not geography alone. Asia does have genuine structural advantages: large digital populations, government-built payment infrastructure, super-app ecosystems that collapse the cost of adding a new service, and regulators who have often treated digitalization as a national priority rather than a threat to manage. But the truly transferable insight is the set of business model archetypes that emerged from this environment, because each one reflects a deliberate strategic choice, not a consequence of context that cannot be replicated elsewhere.

McKinsey research published in March 2026 identified six such archetypes that have repeatedly surfaced across Asian markets and sectors. Together they represent a coherent new vocabulary for growth architecture. Each one is examined below, with the specific mechanisms that drive its economics, the companies that have executed it most convincingly, and the concrete lessons that businesses in any market can extract and apply.

"The strategic question for global leaders is no longer whether these models will spread but how quickly they can be adapted to unlock the next wave of disproportionate, sustainable growth." McKinsey Strategy and Corporate Finance Practice, March 2026

The Four Structural Conditions That Enabled Rapid Experimentation

Scale and speed of digital adoption. Asian markets combine massive user bases with unusually high rates of digital participation. A new livestream format or product concept can reach tens of millions of users almost immediately, compressing the feedback loop so that business model hypotheses get tested at national scale within days rather than quarters.

Public-private digital infrastructure. India's Unified Payments Interface enables real-time payments for hundreds of millions of people. The Open Network for Digital Commerce gives the smallest merchants access to national demand. China's digital identity infrastructure, Singapore's Government Tech Stack, and Indonesia's QRIS payment network each lower onboarding friction and raise digital participation across the income spectrum.

Super-app ecosystems. Apps hosting hundreds or thousands of mini apps embed payments, identity, logistics, messaging, and credit in a single interface. Once a user's payment method and identity are stored, the incremental cost of trying a new product within the same ecosystem approaches zero, giving ecosystem builders a compounding structural advantage.

Regulation as catalyst. In several Asian markets, regulators have designed frameworks that encourage rapid digitalization while establishing clear rules for data use and identity security. This has enabled fast and responsible scaling across healthcare, financial inclusion, and logistics, effectively lowering risk for digital investment and allowing companies to build at speed.

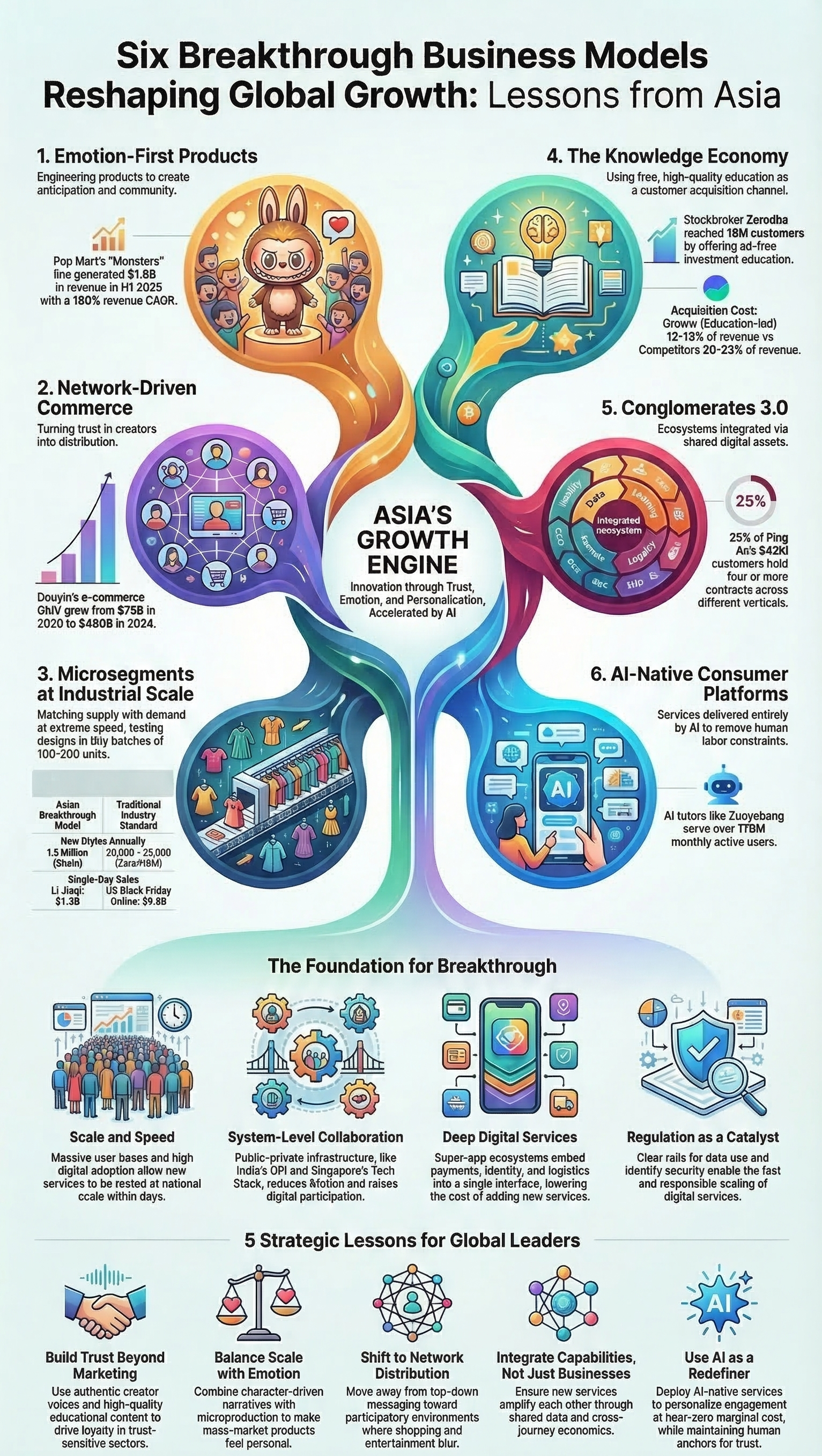

1. Emotion-First Products

Engineering anticipation, identity, and community as core economic drivers

The first archetype represents a fundamental reorientation of product strategy. In most traditional development frameworks, emotion is treated as a brand-building output, something advertising and design add on top of a functional core. Emotion-first product companies reverse this logic entirely. They engineer emotional mechanisms into the product architecture itself and treat those mechanisms as the primary driver of revenue, retention, and margin.

The specific mechanics vary by category but share common elements: engineered scarcity, drop calendars that create anticipation, fan rituals that establish community identity, collection loops that sustain engagement over time, live cocreation events, and richly developed intellectual property that serves as connective tissue across all of these elements.

Pop Mart and the Blind-Box Economy

Pop Mart is the clearest current example at industrial scale. Its blind-box collectibles, particularly the Monsters line featuring the Labubu character, translate the mechanics of anticipation directly into commercial outcomes. In the first half of 2025, Pop Mart generated 1.9 billion dollars in revenue, with its Monsters IP accounting for more than a third of that total. Its trailing twelve-month revenue CAGR reached 180 percent, and the company grew to a market capitalization of fifty billion dollars, making it the largest in its peer group. The Labubu character has demonstrated that a single well-constructed IP can become a multiproduct growth engine spanning physical collectibles, digital content, licensing, and event experiences.

HYBE and the K-Pop Community Architecture

HYBE, the agency best known for representing BTS, demonstrates that the emotion-first model scales beyond physical products into entertainment ecosystems. The company surpassed 1.6 billion dollars in revenue in 2023 by building communities that span offline concerts, digital content, livestreams, and direct fan-to-artist interaction through its proprietary Weverse platform. Fans participate in structured rituals, cocreate content, and experience a genuine sense of belonging that translates into highly predictable recurring spending across merchandise, digital items, albums, and tickets.

Key Points: Emotion-First Products

- Engineered scarcity and drop mechanics create measurable anticipation that drives purchase conversion without traditional advertising spend.

- Collection loops sustain engagement over time, reducing churn and increasing lifetime value without discounting.

- IP developed around community identity scales across physical, digital, and experiential revenue streams simultaneously.

- Emotional engagement metrics such as content velocity and ritual participation are leading indicators of revenue predictability.

- The model is sector-agnostic: finance, beauty, food, and consumer electronics brands have all applied its core mechanics successfully.

2. Network-Driven Commerce

Turning creator trust into a primary distribution channel and complete retail system

The second archetype has evolved far beyond what Western markets currently recognize as influencer marketing. In Asia, creator-led commerce has matured into a complete retail system with its own conversion mechanics and customer relationship logic. The central asset is trust, specifically the trust that creators and community figures have built with their audiences, and the commerce layer is designed to preserve and leverage that trust rather than erode it.

The Livestream Commerce Scale Opportunity

Douyin's e-commerce gross merchandise value grew approximately sevenfold in five years, from an estimated 75 billion dollars in 2020 to 490 billion dollars in 2024. Conversion rates and average order values from livestream sessions frequently exceeded those of traditional static product pages. Southeast Asia followed a similar trajectory: TikTok Shop's regional GMV grew nearly fourfold in a single year, from 4.4 billion dollars in 2022 to approximately 16.3 billion dollars in 2023.

The reason conversion rates are higher in creator-led commerce is architectural. Livestream hosts sell in local dialects, embed cultural context, answer questions in real time, and demonstrate product expertise in a way that feels more like advice from a trusted friend than an advertisement. The format collapses the purchase funnel from weeks to minutes. On the first day of the 2023 Singles' Day shopping festival, Chinese influencer Li Jiaqi drove an estimated 1.3 billion dollars in gross merchandise value in a single day, more than thirteen percent of total online Black Friday sales in the United States for the same year.

Key Points: Network-Driven Commerce

- Livestream commerce compresses the purchase funnel from weeks to minutes by combining awareness, education, and purchase in a single session.

- Trust architecture, not celebrity status, drives conversion: transparent claims, live Q&A, and cultural fluency matter more than raw reach metrics.

- Commission structures should be built on SKU-level contribution margins post-returns, not gross revenue, to ensure channel profitability.

- Creator-led commerce performs best when it feels like community support rather than advertising.

- The model is applicable across categories: financial products, health and wellness, home goods, and apparel have all proven viable in creator-led formats.

3. Microsegments and Microproducers

Matching supply to demand at extreme granularity without sacrificing unit economics

The microproduction archetype is built on a single insight: the cost of variety has collapsed. Advances in supply chain digitalization, demand sensing, and AI-powered pattern recognition have made it possible to deliver personalized or small-batch products at unit costs previously associated only with mass production. Companies that rebuilt their operating models around this reality early have achieved growth rates that conventional competitive analysis cannot fully explain.

Shein and the Industrial-Scale Microproduction Model

Shein's revenue grew from approximately 23 billion dollars in 2022 to 38 billion dollars in 2024, a compound annual growth rate of roughly 29 percent, while remaining profitable throughout. The mechanism is a production model that tests new designs in batches of 100 to 200 units, versus the 300 to 500 unit minimums typical of competitors such as Zara. Designs that perform well are reordered rapidly; those that do not are discontinued with minimal inventory exposure. Concepts move from design to production in as few as five days. The company lists between 2,000 and 10,000 new stock-keeping units per day, offering up to 1.3 million new styles annually, compared to approximately 20,000 to 25,000 for H&M and Zara each.

India's ONDC and the Microproducer Infrastructure Play

India's Open Network for Digital Commerce demonstrates how digital infrastructure can enable microproducers at any scale to reach national demand. Monthly transactions on the network increased threefold in the first year of launch, from approximately five million in 2022 to fifteen million in 2023. With more than 700,000 sellers on the network, ONDC shows how local artisans, home businesses, and small retailers can access shared identity, payment, and logistics rails that would be prohibitively expensive to build independently.

Key Points: Microsegments and Microproducers

- Reducing minimum production batch sizes dramatically lowers inventory risk and enables faster iteration based on real demand signals.

- AI-powered demand sensing and pattern recognition are the critical enabling technologies for real-time trend identification at this granularity.

- The model is not limited to fashion: food, publishing, financial products, and consumer electronics have all demonstrated viable applications.

- Shared digital infrastructure, as demonstrated by ONDC, makes the model accessible to producers of any size without large capital investment.

- Speed from concept to production is the primary competitive variable; supply chain digitalization investment should be evaluated against this metric specifically.

4. The Knowledge Economy Model

Using free, high-quality education to build trust and dramatically reduce customer acquisition costs

In most industries, education is treated as either a cost center under the label of corporate social responsibility, or a marketing channel where educational content is thinly veiled product promotion. A distinct category of Asian companies has found a third path: treating genuinely useful, non-commercial education as a strategic acquisition and retention asset with measurable unit economics advantages over conventional digital advertising.

Zerodha, Groww, and the Organic Acquisition Advantage

Zerodha became India's largest stockbroker in 2019, just ten years after launching, without running a single traditional advertising campaign. Its growth engine was Varsity, a comprehensive, advertisement-free educational platform covering every aspect of financial markets. By creating a genuine educational resource with no visible commercial agenda, Zerodha captured a disproportionate share of high-value customers who arrived with both the knowledge to use the platform and the trust formed through months of educational interaction. The company has since accrued more than sixteen million total customers including seven million active users.

In 2024, Groww overtook Zerodha as market leader, reaching more than twelve million active users and approximately 27 percent market share. Public filings indicate roughly 80 percent of customers find Groww organically, and its customer acquisition costs represent only 12 to 13 percent of revenue. Competing platform AngelOne, using more conventional digital advertising, spends 20 to 23 percent of revenue on acquisition for a smaller total share of customers. That differential compounds over time as educational content continues attracting new users without proportional additional spend.

ITC's e-Choupal and Agricultural Knowledge Networks

The knowledge economy model is not limited to financial services. India's ITC Limited has operated its e-Choupal initiative for more than twenty years, connecting directly with farmers across 35,000 villages by publishing transparent daily commodity prices and sharing practical agronomy advice. The network currently serves four million customers, and farmers who adopted the program's recommended practices saw their incomes double. This is not corporate social responsibility in the conventional sense; it is a procurement and loyalty strategy that uses knowledge access to build supply relationships competitors cannot replicate with price alone.

Key Points: The Knowledge Economy Model

- Genuinely useful, non-commercial educational content generates organic customer acquisition that compounds in cost efficiency over time.

- Customer acquisition costs in this model are often 40 to 60 percent lower than equivalent digital advertising-driven acquisition.

- The model is most powerful in high information-asymmetry categories: finance, healthcare, agriculture, utilities, and insurance.

- Educational content that avoids overt product promotion generates significantly higher trust transfer to the adjacent commercial offering.

- Knowledge platforms create proprietary data on customer learning journeys that informs product development and personalization strategy.

5. Conglomerates 3.0

Ecosystem orchestration through shared digital rails rather than shared capital or brand

Traditional conglomerates justified their multi-business structure through pooled capital, shared management expertise, and common brand equity. The Conglomerate 3.0 model adds a more powerful form of integration: shared digital infrastructure in the form of identity, payments, data, and loyalty that creates genuine incentives for customers to prefer the ecosystem over any single-category competitor. Value in this model comes from the connections between businesses, not just from the businesses themselves.

Ping An and Systematic Cross-Selling at Scale

Ping An's ecosystem spans financial services, healthcare, auto services, and smart-city solutions, all integrated through a unified identity and data platform. A quarter of its retail customers hold four or more contracts across different verticals. Cumulative patent applications reached approximately 55,000 by 2024, driven largely by AI and digital capabilities that allow customers to move between services seamlessly, with each interaction enriching the data set powering personalized recommendations and risk assessments. Approximately 72 percent of Ping An customers have been with the company for five years or more, and the year-over-year retention rate sits at approximately 95 percent. The company served 242 million customers at the end of 2024, up 11 percent since 2020.

Reliance and the Multi-Vertical Digital Ecosystem

India's Reliance has applied similar logic at national scale across telecommunications, digital content, e-commerce, payments, and offline retail. Its shared digital assets enable cross-vertical bundling and personalized loyalty that gives customers reasons to engage across the full ecosystem. Reliance nearly doubled its annual revenues over eight years, reaching more than 100 billion dollars, to become one of the largest companies in the world. Thailand's CP Group demonstrates the model translates across cultural and regulatory contexts, using shared logistics, data, and loyalty networks to scale across agri-food, retail, and adjacent categories.

Key Points: Conglomerates 3.0

- Value derives from the connections between business units, not just from individual unit performance.

- Unified identity, payments, and data infrastructure reduce marginal customer acquisition cost for every new vertical added.

- Cross-contract customer metrics, such as share holding four or more products, are the most relevant leading indicators of ecosystem health.

- Retention rates above 90 percent are achievable when personalization is powered by cross-service behavioral data rather than single-category history.

- The model requires deliberate redesign of processes for cross-journey economics; siloed unit optimization will undermine ecosystem value creation.

6. AI-Native Consumer Platforms

Delivering services primarily through AI to break free from human labor constraints

The sixth archetype is qualitatively different because it does not augment existing service delivery with technology; it removes the constraint that human labor imposes on scalability. AI-native consumer platforms deliver services primarily or entirely through AI, which changes the fundamental cost structure. Services that previously had a near-linear relationship between revenue growth and headcount growth can now decouple those variables almost entirely.

AI Tutoring at Population Scale

Across China, India, and South Korea, AI tutors have become mainstream. Platforms such as Yuanfudao and Zuoyebang offer millions of personalized practice sessions daily. Zuoyebang alone reports more than 170 million monthly active users. These systems adjust difficulty, explanation style, and content sequencing based on individual student behavior, approximating one-to-one tutoring quality at near-zero marginal cost per session. Yuanfudao, valued at more than fifteen billion dollars in 2020, continues to expand: device sales grew 120 percent year over year in third-tier Chinese cities, demonstrating that AI-native education is a mass-market product, not a premium urban one.

Virtual Humans and AI-Generated Commerce Hosts

Virtual humans, AI-generated digital entertainers designed to look and behave like human celebrities, attract millions of followers and produce content monetized through merchandise, live events, and brand collaborations. In commerce, AI-generated hosts can maintain consistent personas across unlimited simultaneous sessions, adapt scripts based on real-time audience sentiment, and answer product questions instantly. For brands, this delivers consistent message control and unlimited output capacity. The balance is delicate, however: brands that overweight AI interaction without sufficient human anchors report declining trust scores that are difficult to reverse.

Key Points: AI-Native Consumer Platforms

- Near-zero marginal cost per interaction is the defining economic advantage, enabling personalization at scale that was previously cost prohibitive.

- AI tutors and AI-generated commerce hosts have both demonstrated the ability to match human-delivered conversion in specific high-volume contexts.

- The model is most powerful for interactions that are high in volume, consistent in structure, and where personalization adds measurable value.

- Human anchors remain essential; fully AI-native experiences without credible human signals show measurable trust erosion over time.

- Compute infrastructure investment is a critical prerequisite; companies that do not secure capacity early may find themselves constrained as demand scales.

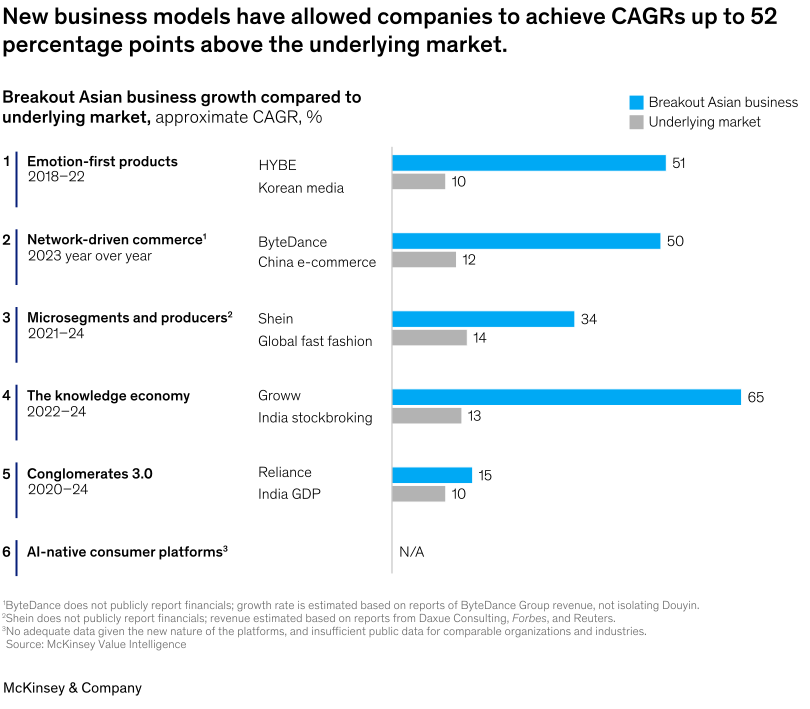

Comparative Overview: All Six Business Model Archetypes

The table below synthesizes each archetype across the dimensions most relevant to a leadership team evaluating which models to prioritize. CAGR figures reflect breakout company performance relative to their underlying market as documented in the McKinsey research. Adoption complexity reflects organizational and technical investment required to begin implementing the model at meaningful scale.

| Business Model | Core Mechanism | Lead Example | Key Metric | CAGR vs Market | AI Role | Best-Fit Sectors | Adoption Complexity |

|---|---|---|---|---|---|---|---|

| Emotion-First Products | Scarcity, drops, IP narratives, collection loops | Pop Mart, HYBE | $50B market cap for Pop Mart | 51% vs 10% | Accelerant: creative cycle compression, personalized fan engagement | Consumer goods, entertainment, gaming, beauty | Medium |

| Network-Driven Commerce | Creator trust as distribution channel, livestream conversion | Douyin, TikTok Shop | 540% GMV uplift over five years | 50% vs 12% | Accelerant: personalized host scripts, real-time sentiment adaptation | Retail, fashion, FMCG, financial products | Medium |

| Microsegments and Microproducers | Small-batch production, rapid demand sensing, SKU proliferation | Shein, ONDC sellers | 65% two-year revenue uplift for Shein | 34% vs 14% | Core enabler: trend detection, design generation, inventory forecasting | Fashion, food, publishing, consumer electronics | High |

| The Knowledge Economy | Free non-commercial education as acquisition channel | Zerodha, Groww, ITC e-Choupal | 42% combined broking market share | 65% vs 13% | Accelerant: personalized learning paths, adaptive content delivery | Finance, healthcare, agriculture, utilities, insurance | Low-Medium |

| Conglomerates 3.0 | Shared digital rails: identity, payments, data, loyalty | Ping An, Reliance, CP Group | 66% six-year revenue uplift for Reliance | 15% vs 10% | Core enabler: cross-service personalization, predictive cross-sell | Financial services, telecoms, retail, healthcare | High |

| AI-Native Consumer Platforms | AI replaces human labor as primary service delivery mechanism | Zuoyebang, Yuanfudao, virtual human platforms | 120% YoY device sales growth for Yuanfudao | Insufficient public data | Fundamental: AI is the product, not an enhancement | Education, entertainment, customer service, financial advice | High |

AI as a Cross-Cutting Accelerant Across All Six Models

While the sixth archetype is explicitly AI-native, artificial intelligence plays a meaningful role in every one of the six models. The distinction between AI as the product and AI as an accelerant of a human-centered model is important for any company evaluating where to invest its technology capabilities.

In emotion-first products, generation tools compress creative cycles by enabling faster prototyping of character designs and campaign narratives. In the microsegments model, AI pattern recognition senses emerging micro-trends in real time, generates design variations at speed, and forecasts demand with the granularity required to make small-batch production decisions confidently. In the knowledge economy model, AI enables personalized learning paths that improve educational outcomes and deepen the trust relationship with learners before they become customers.

In network-driven commerce, personalized AI recommendations and automated follow-up sequences extend the reach and efficiency of creator relationships. In Conglomerate 3.0, cross-service data integration and predictive cross-selling algorithms are the technical foundation of the entire ecosystem value proposition. The common thread is that AI transforms personalization at scale from cost-prohibitive to practically ubiquitous.

Important Balance Point

AI cannot substitute for the trust between creators and communities, or between educators and learners. Every one of the six archetypes depends on a human trust relationship to some degree. The most effective AI deployments are those that identify precisely which interactions benefit from AI delivery and which require a human presence. Getting this balance right is one of the central strategic challenges in applying any of these models.

Five Transferable Lessons for Global Leaders

These archetypes evolved in a specific environment, but the strategic choices they represent are not tied to that environment. Leaders in any market can apply these five lessons.

Customer

Build trust through creators, community, and education. Free, high-quality educational content in information-asymmetric categories drives acquisition more effectively than advertising at a fraction of the cost.

Product

Create products that balance scale with emotional resonance. Microproduction is now economically viable. Personalization previously limited to luxury lines is achievable at mass-market price points.

Channel

Shift to network-driven distribution. Creators and community figures serve as trusted advisers. These channels convert because they feel intimate and relevant, even when delivered to millions simultaneously.

Operating Model

Share capabilities and assets across the entire business. Replace siloed unit optimization with cross-journey economics. Each new service should amplify the others through shared digital infrastructure.

Technology

Use AI and digital rails across all dimensions. Balance AI efficiency with credible human anchors. Maintain trust as the highest priority in any AI deployment decision across all six archetypes.

A Final Note on the Direction of Travel

The six archetypes described here are not theoretical constructs. Each one has been tested at significant scale by companies that have paid for the lessons embedded in these models through years of experimentation and operational iteration. The growth rates they have produced are empirically documented and reproducible in their structural logic outside the Asian context in which they emerged.

The consistent thread running through all six models is a move away from reach-based, broadcast-oriented, and feature-competitive strategies toward architectures built on trust, personalization, emotional resonance, and shared value creation. These are measurable variables that show up in customer acquisition costs, retention rates, average contract depth, and lifetime value. Companies that build their growth architecture around them tend to generate unit economics that are structurally superior to those competing on features or price alone.

Asia has offered a preview. The question for any leadership team is not whether these models represent a relevant strategic direction but which one, or which combination, aligns most closely with the trust assets, customer relationships, and technological capabilities the business already has, and what investment is required to build the rest.

Source: Content analysis based on McKinsey Strategy and Corporate Finance Practice research, March 2026, authored by Semyon Yakovlev (Senior Partner, Seoul) and John Davis (Associate Partner, Melbourne). All company metrics cited are sourced from the original McKinsey publication and its referenced primary sources. This analysis is provided for educational and strategic reference purposes only.