Top 8 Startups from Y Combinator W26

8 Investor-Chased Startups, the Signals Behind the Frenzy, and What the Strongest Batch in YC History Means for Founders.

There is a room — virtual now, but its gravity has never been more real — where a single three-minute pitch can redirect millions of dollars and reshape entire industries. Y Combinator's Demo Day has served as the startup world's most reliable leading indicator since 2005. Not because every company that presents becomes a unicorn, but because the patterns visible across each batch consistently predict where venture capital, engineering talent, and market energy will concentrate over the following decade.

The Winter 2026 cohort was not a typical batch.

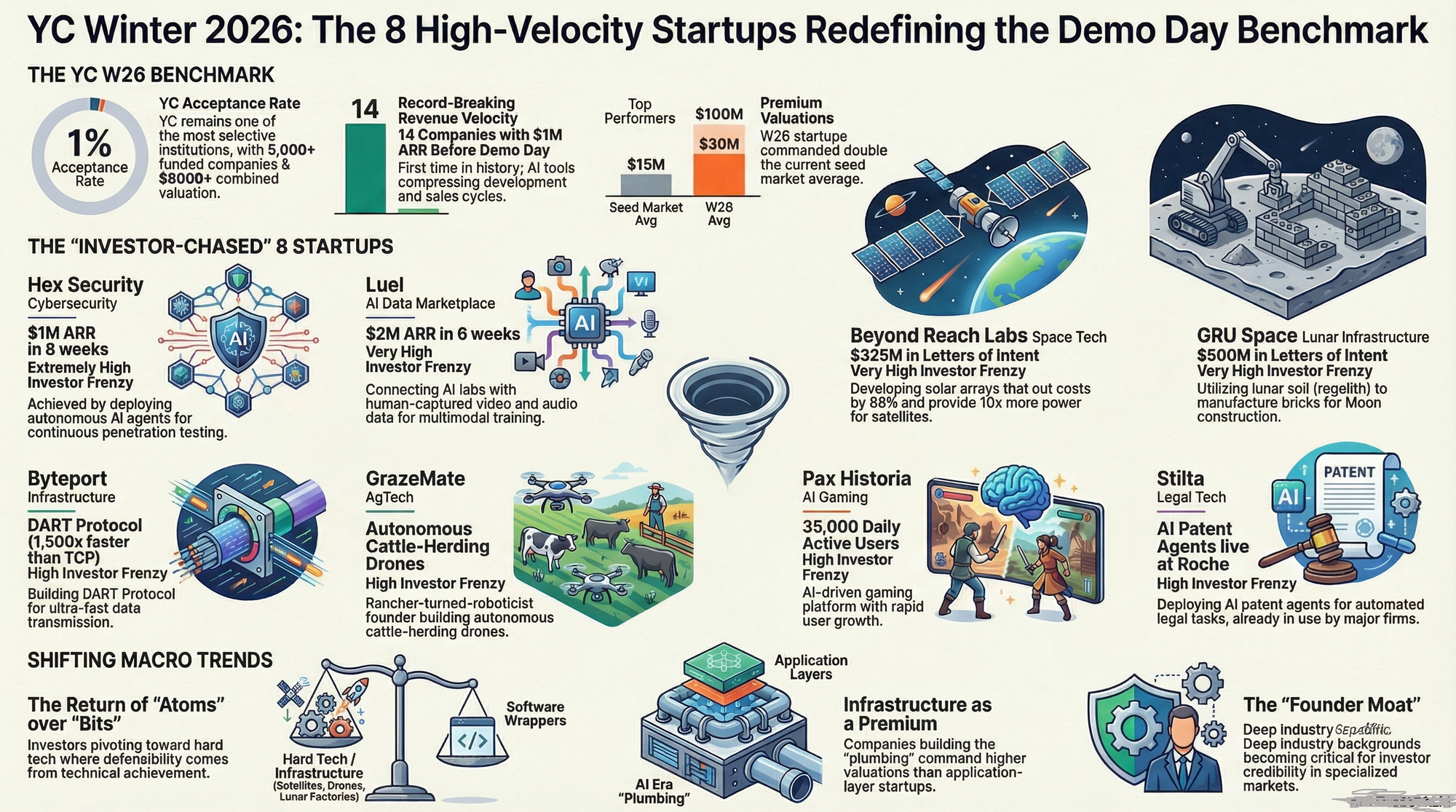

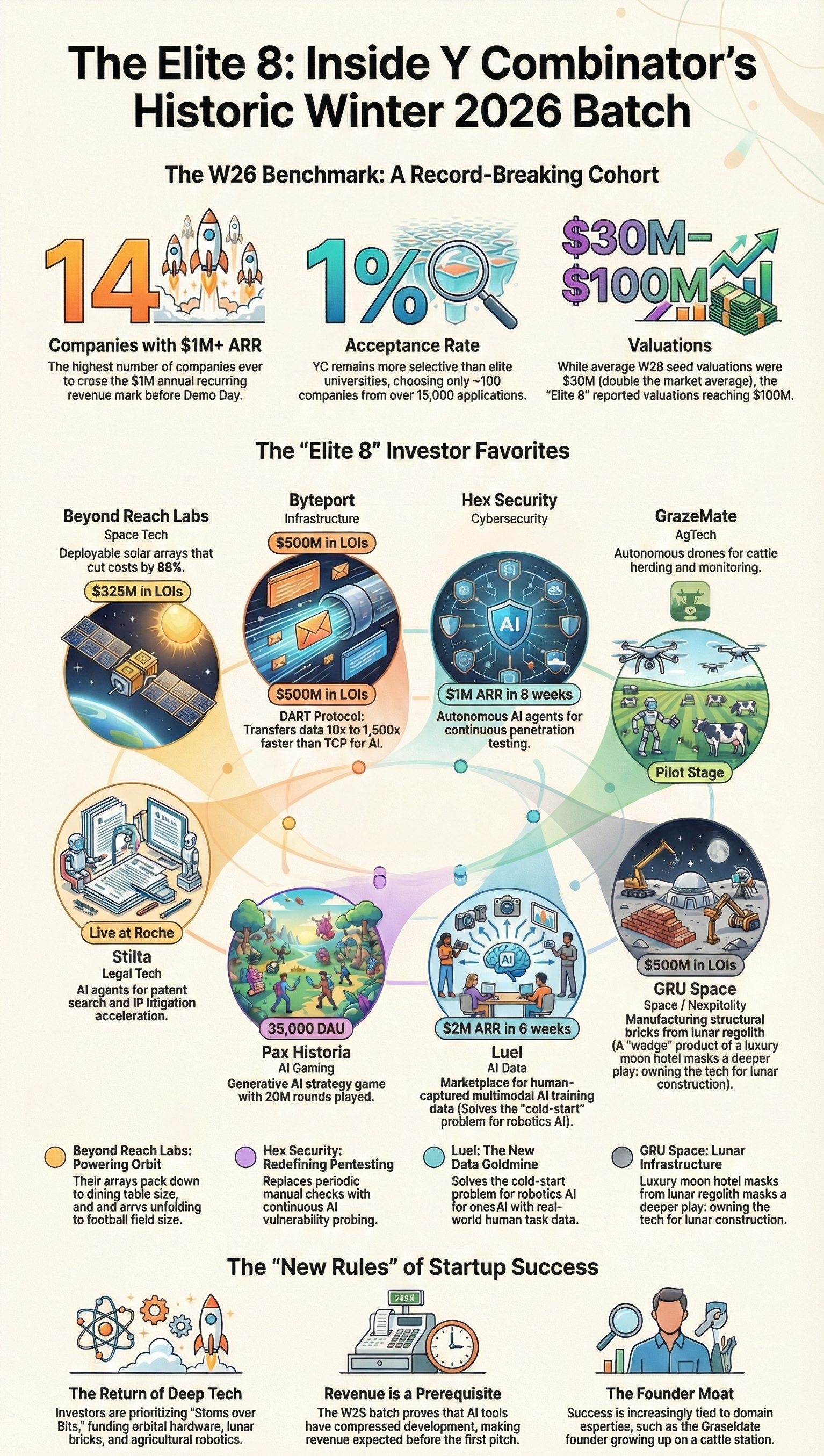

Rebel Fund, which has attended every YC Demo Day since 2013 and built a machine-learning algorithm trained on the entire history of YC companies, published a number before a single startup had presented: 35 percent of W26 companies scored in the top 20 percent of all YC companies ever evaluated. No previous batch had come close to that figure. Garry Tan, YC's CEO, confirmed that 14 companies in the batch had already crossed one million dollars in annualized revenue before Demo Day concluded — three times the number from the batch just three months prior, and the highest total in YC history.

Average weekly revenue growth across the nearly 200-company cohort was 14 percent — the fastest ever recorded.

What follows is not a press-release roundup. This is a signal-focused breakdown of the eight companies that multiple venture capitalists independently identified as their top picks — meaning they attracted competitive term sheets, not just polite interest. Each profile examines not just what the company builds, but the structural reason it belongs on every serious founder's radar. The trend synthesis and founder playbook sections that follow the profiles are where the real analytical value sits.

Read this the way an investor memo is meant to be read: with an eye toward the patterns, not just the names.

Top 8 Startups from YC W26: At a Glance

Before the in-depth profiles, this table gives readers an immediate orientation. Every company here was flagged by at least two independent venture capital investors as a top pick. That threshold is deliberately conservative — it filters out single-investor enthusiasm and captures genuine market demand.

|

# |

Startup |

What It

Builds |

Why

Investors Are Watching |

|

01 |

Beyond

Reach Labs |

Deployable

solar arrays for satellites (dining-table to football-field in orbit) |

$325M LoIs

secured; 2027 flight planned; 10x power increase claimed |

|

02 |

Byteport |

DART protocol

— up to 1,500x faster file transfer than TCP |

Critical AI

infrastructure play; no comparable alternative at scale |

|

03 |

Hex

Security |

AI agents that

continuously pen-test company infrastructure |

$1M+ run-rate

in 8 weeks; investors reportedly fought for allocation |

|

04 |

GrazeMate |

Autonomous

drones that herd cattle, estimate weight, monitor pasture |

Founder grew

up on a 6,000-head cattle station; replaces helicopters |

|

05 |

GRU Space |

Lunar regolith

brick factory — foundation for a Moon hotel by 2032 |

$500M LoIs;

White House invitation; in-situ resource utilization moat |

|

06 |

Luel |

Marketplace

connecting AI labs with human-captured daily-life data |

~$2M ARR in 6

weeks; serves robotics and voice AI labs directly |

|

07 |

Pax

Historia |

Generative

alt-history strategy game — infinite scenario engine |

35K daily

users; 20M rounds played; education and gaming crossover |

|

08 |

Stilta |

AI agents that

search and analyze patents for IP lawyers |

Live at Roche;

Swedish founders carry Lovable/Legora halo effect |

The table above rewards close reading. Three patterns are immediately visible: revenue velocity is unprecedented, letters of intent are replacing traditional traction proxies for deep-tech companies, and consumer gaming has found a credible place at the YC table again. The profiles below unpack each of these signals in depth.

490+ Pitch Decks That Raised Millions

Stop guessing what investors want. Get access to 496 real pitch decks used by startups that successfully raised funding.

- 📊 Real decks from funded startups

- 💡 Proven storytelling & slide structures

- 🚀 Learn what actually gets investors to say “yes”

- 🧠 Perfect for founders, freelancers & creators

Used by founders raising pre-seed to Series A

Why YC Demo Day Is Still the World's Most Consequential Startup Signal

Before diving into individual companies, context is warranted. Y Combinator has now funded more than 5,000 startups, and its portfolio carries a combined valuation exceeding 600 billion dollars. Statistically, 4.5 percent of YC companies reach unicorn status — roughly nine times the rate of other venture-backed startups. Forty-five percent raise a Series A. One in four YC unicorns becomes a decacorn.

The W26 Demo Day added a structural data point that changes how those historical numbers should be read. Fourteen companies crossed one million dollars in ARR before presenting — with founding-team-only resources, inside a 90-day program. For reference: the standard benchmark for 'top tier' at YC Demo Day used to be 150,000 to 500,000 dollars in ARR. That bar has now more than doubled for elite companies.

Valuation benchmarks shifted too. The default W26 round — for companies not on anyone's top-eight list — is four million dollars on a 40-million-dollar post-money valuation. Three years ago in W23, that default was two million dollars on a 20-million-dollar valuation. Entry prices doubled in 36 months. The top end of W26 valuations reached 200 million dollars post-money, the highest single-company Demo Day valuation in six years of tracking.

- 14 YC companies crossed $1M ARR before Demo Day — 3x more than the previous cohort.

- 14% Average weekly revenue growth across ~200 W26 companies — fastest in YC history.

- 35% of W26 startups score in the top 20% of all YC companies ever evaluated (Rebel Fund).

The explanation for these numbers is structural, not coincidental. AI tools collapsed the time from founding to working product. What required six months of engineering effort in 2022 now takes six weeks. Companies enter YC with more runway to sell, iterate, and generate revenue before Demo Day arrives. Understanding this compression is critical context for everything that follows.

The 8 Investor-Chased Startups: Deep Profiles

Each profile below follows the same structure: what the company builds, the real signal behind investor interest, and a synthesized key takeaway. The goal is not to summarize press releases but to surface the underlying logic that explains why sophisticated capital is competing for these specific deals.

01. Beyond Reach Labs

Deployable Solar Arrays for Satellites

What It Builds

Every satellite in orbit is power-constrained. Solar arrays must survive the mechanical stresses of a rocket launch, which means they are designed to fold into compact volumes — volumes that directly limit how much power they can generate. Beyond Reach Labs has developed deployable solar arrays that compress to the footprint of a dining table at launch, then unfold to the size of a football field once in orbit.

The claimed performance delta is striking: ten times more available power at 88 percent lower cost than conventional approaches. The company already has a flight scheduled for 2027, a near-term validation milestone that hardware companies rarely possess at seed stage.

The Real Signal

The 325 million dollars in letters of intent from space companies is not marketing. In the satellite industry, where customer acquisition cycles span years and procurement processes involve multi-year budget planning, letters of intent at that scale indicate that the problem being solved is real and the solution architecture is credible enough for operators to commit interest formally.

The market logic is horizontal. Satellite constellations are proliferating across broadband, earth observation, and defense applications. Every satellite operator is power-constrained. A company that solves power constraints for all of them simultaneously is an infrastructure play, not a niche product. Horizontal infrastructure companies at YC tend to attract the most institutional capital.

KEY TAKEAWAY Beyond Reach Labs is not a satellite company — it is a power infrastructure company that operates in orbit. The distinction matters for valuation, because infrastructure multiples are structurally higher than application multiples.

02. Byteport

A File Transfer Protocol Built for the AI Era

What It Builds

TCP, the dominant file transfer protocol, was engineered for a world before petabyte-scale datasets, large language model training runs, and real-time autonomous system data pipelines. Byteport's founder Jayram Palamadai identified this mismatch and built DART — Dynamic Accelerated Record Transfer — a protocol that averages 10 times faster than TCP on standard connections and up to 1,500 times faster on high-reliability infrastructure.

That 1,500x figure requires explanation: TCP allocates significant overhead to error correction and packet-loss recovery, which is critical on unreliable networks but wasteful on modern fiber. DART strips that overhead on connections where packet loss is negligible, recovering speed that TCP permanently sacrifices for robustness.

The Real Signal

Infrastructure that removes bottlenecks in AI workflows has leveraged impact across every company in the AI stack. Faster data transfer compresses training cycles, reduces compute costs, and makes applications practical that were previously rate-limited by data movement. Investors who have spent years funding AI application layers have learned that the next generation of value sits in the infrastructure beneath those layers.

Byteport's addressable market is large and growing: cloud providers, AI labs, autonomous systems companies, genomics firms, and any enterprise moving large datasets continuously. The product does not require a behavior change in how companies build — it requires a protocol swap that immediately reduces costs and latency.

KEY TAKEAWAY Byteport is a classic infrastructure wedge: the product is unsexy, the leverage is enormous, and switching costs grow with every system that adopts the protocol. That combination is what patient institutional investors value most.

03. Hex Security

Continuous AI Penetration Testing Agents

What It Builds

The asymmetry in cybersecurity has reached a structural crisis point. AI-powered attacks are continuous, adaptive, and inexpensive to launch at scale. The traditional defense model — periodic manual penetration testing, conducted perhaps twice a year by expensive contractors — produces a vulnerability snapshot that is outdated the day it is delivered. The gap between offense tempo and defense tempo has never been wider.

Hex Security deploys AI agents that function as permanent autonomous penetration testers. They probe continuously, model attack paths, and surface exploitable gaps before adversaries reach them. The cost structure is a fraction of manual engagements because the agents run without human oversight at scale.

The Real Signal

One million dollars in annualized run-rate revenue within eight weeks of launch. That number is the signal. Enterprise security sales typically require months of procurement cycles, legal review, and security assessments before a contract is signed. A B2B security company crossing that threshold in two months means enterprises are buying without running the full cycle — which in turn means the pain is acute enough to compress procurement. One investor told TechCrunch that venture firms were actively competing for allocation in this round, a characterization that appears in reporting perhaps twice a year for any single company globally.

The timing advantage is also structural: AI-powered attacks are documented and accelerating. The market does not need to be educated that the problem exists. Every CISO in an enterprise already knows the defense cadence is broken. Hex is arriving at an inflection point, not trying to create one.

KEY TAKEAWAY When a B2B security company crosses $1M run-rate in eight weeks, investors are not seeing product-market fit — they are seeing proof that an entire industry's defense model is structurally broken and that this team found the crack first.

04. GrazeMate

Autonomous Drones That Herd, Monitor, and Optimize Cattle Operations

What It Builds

Moving cattle across large ranches is expensive, physically dangerous, and increasingly difficult to staff. The traditional tools — helicopters, motorbikes, and experienced hands — are all facing supply constraints: helicopter operating costs have risen, and agricultural labor shortages have made experienced rangeland workers harder to hire and retain.

GrazeMate's founder grew up on a 6,000-head cattle station in Australia before pursuing a robotics degree, then dropped out of university to solve the problem directly. The company's autonomous drones can guide cattle to designated pasture areas without a human pilot, estimate individual animal weights through visual analysis, assess grass availability and growth rates across large acreages, and follow pre-set route plans across varied terrain.

The Real Signal

Founder-market fit of this specificity is rare and extremely valuable. The company did not identify a farming problem from a startup accelerator cohort — it was built by someone who grew up inside the problem and had the technical skills to address it. That combination gives GrazeMate credibility with its customer base that external competitors cannot easily replicate, regardless of engineering quality.

The broader investment thesis extends beyond herding. Drones that move across ranches collecting visual data are simultaneously building a precision livestock management platform: weight estimation, pasture optimization, health monitoring, and herd tracking all compound in value as the data accumulates. The hardware is a distribution mechanism for a data platform.

KEY TAKEAWAY GrazeMate is the canonical example of why domain expertise compounds into structural moat. The product is defensible not primarily because of IP, but because of the institutional trust that comes from a founder who has literally lived the customer's problem.

05. GRU Space

Permanent Lunar Infrastructure, Starting With a Hotel on the Moon

What It Builds

GRU Space founder Skyler Chan — a recent Berkeley graduate who previously built software at Tesla and worked on NASA-funded space technology — has developed a process for manufacturing structural bricks from lunar regolith, the loose granular material that covers the Moon's surface. This in-situ resource utilization approach is essential to any economically viable long-term lunar presence, because the cost of shipping construction materials from Earth makes surface structures prohibitively expensive at scale.

The company is using this lunar brick technology to build what Chan describes as a 'moon factory' — a manufacturing base that can produce structural materials for any lunar application. The luxury hotel announced for 2032 is, in his framing, a 'wedge product': high-visibility, commercially interesting, and a compelling demonstration of what the underlying construction technology can produce.

The Real Signal

The 500 million dollars in letters of intent, the White House invitation, and the reported Trump family reservation are attention signals, not validation signals in the traditional sense. The genuine investor thesis is about timing and infrastructure position. The Artemis program, commercial lunar landers, and intensifying geopolitical competition for lunar presence have created a credible near-term market for lunar surface infrastructure support — a market that did not exist three years ago in anything like its current form.

A company that manufactures structural materials on the lunar surface becomes critical-path for every subsequent lunar operation, regardless of who conducts those operations. That is an infrastructure position with extraordinary optionality — the ultimate platform play, located 238,855 miles from its nearest competitor.

KEY TAKEAWAY GRU Space is not being valued as a hotel company. Sophisticated investors are pricing it as a materials and manufacturing infrastructure play that happens to have a hotel as its most legible early output. The distinction determines the exit multiple.

06. Luel

The Human-Captured Data Marketplace Powering Multimodal AI

What It Builds

Training multimodal AI systems requires data that reflects how humans actually inhabit the physical world. A humanoid robot learning to iron a shirt needs video of humans ironing shirts — captured at angles that match sensor configurations, under varied lighting, across diverse body types. A medical AI conducting patient intake interviews needs recordings of authentic doctor-patient conversations with all their natural ambiguity. That data does not exist in any existing public dataset at the scale or specificity that frontier AI developers need.

Luel, founded by two UC Berkeley dropouts, has built the marketplace infrastructure connecting AI developers with contributors who record and submit structured daily-life activities — audio, video, and image sequences organized around specific tasks. Robotics companies and voice AI labs purchase this data to train models that require ground-truth human behavior rather than synthetic approximations.

The Real Signal

Nearly two million dollars in annualized recurring revenue within six weeks of launch. For a marketplace business — which typically faces a brutal cold-start problem requiring simultaneous supply and demand development — that traction rate is extraordinary. The usual failure mode for data marketplaces is that developers cannot access data until contributors are recruited, and contributors do not join until buyers are present. Luel appears to have solved this coordination problem within weeks.

The structural demand driver is also favorable long-term: synthetic data approaches have proven insufficient for frontier physical AI applications. Robotics and voice AI companies have exhausted what they can generate computationally and now require human-captured ground truth at scale. Luel is building the distribution infrastructure for a resource that does not yet exist in adequate supply.

KEY TAKEAWAY Marketplace businesses with $2M ARR at six weeks are not just demonstrating product-market fit — they are demonstrating that the supply-demand coordination problem was solved before most investors even knew the company existed. That is an extremely rare early-stage signal.

07. Pax Historia

Rewriting History With Generative AI — An Infinite Strategy Engine

What It Builds

Traditional strategy games simulate historical scenarios through scripted decision trees. Designers anticipate player choices in advance and code responses for each branching path. That architecture creates a ceiling: the game can only respond to scenarios its creators imagined. Pax Historia removes that ceiling entirely.

Using generative AI, the game constructs coherent, internally consistent geopolitical simulations in response to any historical scenario a player proposes. What if the Roman Empire never fell? What if the Soviet Union won the Space Race? What if the United States acquired Greenland in 1952? The system handles cascading historical causation — economic, military, diplomatic, cultural — with enough fidelity to be genuinely engaging rather than superficially plausible.

The Real Signal

Thirty-five thousand daily active users who have collectively played nearly 20 million rounds represent something the W26 batch almost entirely lacks: a proven consumer product with demonstrated retention. The batch is 64 percent B2B. A consumer game with those engagement metrics stands out dramatically, both as a business signal and as evidence that the underlying technology is compelling enough to retain users across repeated sessions.

The adjacency value is what makes the deal genuinely interesting to institutional investors. Alternative history simulation has direct educational applications — history teachers can use AI-generated counterfactuals to engage students in causal reasoning. It has applications in corporate scenario planning. Policy analysis. Conflict simulations. The game is the distribution wedge into a category of AI-native interactive experience that has not yet found its dominant platform.

KEY TAKEAWAY Pax Historia is a consumer game sitting on top of a generative simulation engine that has applications far beyond entertainment. Investors are paying for 35K daily engaged users and optioning the rest of the adjacent market.

08. Stilta

AI Agents for Intellectual Property and Patent Law

What It Builds

Patent litigation is a document-intensive, time-consuming, and expensive process. A single dispute can cost up to four million dollars per case, with a substantial portion of that representing fees for attorneys and paralegals manually reviewing thousands of pages of prior art, competing patent claims, and scientific literature across multiple databases simultaneously.

Stilta has built AI agents that can search and analyze patents across multiple databases and scientific literature in parallel, surface relevant prior art, identify claim conflicts, and organize findings in formats that IP attorneys can act on efficiently. The product accelerates attorneys rather than replacing them — a positioning decision that has proven instrumental in enterprise adoption.

The Real Signal

Stilta's agents are already deployed by IP lawyers at Roche, one of the world's largest pharmaceutical companies. In enterprise legal technology, a reference customer of that caliber carries disproportionate weight with procurement teams at other large enterprises. Roche's security, compliance, accuracy, and reliability standards are among the most demanding in any regulated industry. Surviving that procurement process means the product meets bars that most legal tech tools do not.

The geographic signal adds an additional dimension. Stilta's Swedish founders benefit from a halo effect created by recent Swedish startup successes — Lovable and Legora among them — that have established a pattern of strong technical foundations and disciplined commercial execution from Northern European teams. Investors who backed those companies are primed to recognize similar signals in the next Swedish founder cohort.

KEY TAKEAWAY Legal tech products that reduce attorney time without threatening attorney jobs are structurally easier to sell than those positioned as replacements. Stilta's acceleration framing, combined with a Roche reference, is a textbook enterprise legal tech go-to-market.

Full Comparison: All 8 Startups Side by Side

Use this table as a reference layer on top of the profiles above. The columns surface the dimensions that matter most for investor decision-making at seed stage: technical differentiation, revenue evidence, market scale, and the temperature of investor competition for each deal.

|

Startup |

Category |

Core Technology |

Revenue Signal |

Market Opportunity |

Investor Heat |

|

Beyond

Reach Labs |

Space Tech |

Deployable

satellite solar arrays |

$325M in

letters of intent |

Orbital power

infrastructure |

Very High |

|

Byteport |

Data

Infrastructure |

DART file

transfer protocol |

Pre-revenue;

early traction |

AI training

data pipelines |

High |

|

Hex

Security |

Cybersecurity |

Autonomous AI

pen-testing agents |

$1M+ run-rate

in 8 weeks |

Enterprise

security automation |

Extremely High |

|

GrazeMate |

AgTech /

Robotics |

Autonomous

cattle-herding drones |

Pilot stage;

LoI pipeline |

Global

livestock management |

High |

|

GRU Space |

Lunar

Infrastructure |

Lunar regolith

brick factory |

$500M in

letters of intent |

Lunar

construction & hospitality |

Very High |

|

Luel |

AI / Data

Marketplace |

Human-captured

multimodal data |

~$2M ARR in 6

weeks |

Robotics &

voice AI training data |

Very High |

|

Pax

Historia |

Consumer AI /

Gaming |

Generative

alt-history engine |

35K DAU; 20M

rounds played |

AI-native

gaming & edtech |

High |

|

Stilta |

Legal Tech |

AI patent

search & analysis agents |

Live at Roche

(pharma) |

IP litigation

& patent research |

High |

Reading across the table reveals a pattern worth internalizing: the companies generating the most investor heat are either showing exceptional revenue velocity (Hex Security, Luel) or possessing defensible infrastructure positions with strong letters of intent (Beyond Reach Labs, GRU Space). Consumer products (Pax Historia) and enterprise reference deployments (Stilta) occupy the middle tier. Pure pre-revenue infrastructure plays (Byteport, GrazeMate) are high-upside but require more patient capital.

What the W26 Batch Actually Signals: Four Trends Worth Tracking

1. The Deep Tech Resurgence Is Not a Cycle — It Is a Structural Shift

Beyond Reach Labs, GRU Space, GrazeMate, and Byteport are all building in atoms, not bits. Hardware systems, physical protocols, autonomous machines in agricultural environments, and orbital manufacturing are not the typical territory of a startup accelerator batch. Their presence — and their investor heat — signals something more permanent than a funding cycle rotation.

AI tools have collapsed the engineering time required to develop and validate physical product concepts. What previously required 18 months of prototype development now reaches functional proof-of-concept in six. Hardware startups can now move at software speeds for the early validation stages, which makes the YC model — 90 days to traction — suddenly applicable to categories it could not previously serve.

Investors who have spent years waiting for deep tech to become fundable at accelerator timelines are now seeing it happen. This is not a trend that reverses when interest rates change. It is a structural consequence of AI-accelerated development, and it compounds.

2. Revenue Velocity Has Permanently Reset the Benchmark

One million dollars in annual recurring revenue within eight weeks (Hex Security). Two million dollars ARR within six weeks (Luel). These figures define a new reference class for what top-tier early execution looks like. The previous benchmark — 150,000 to 500,000 dollars ARR by Demo Day — now describes mid-tier companies, not elite ones.

The mechanism behind this shift is the same AI tooling that accelerated physical product development: AI-generated sales outreach, AI-assisted product development, AI-powered customer support that extends what small teams can handle. Companies are reaching revenue milestones with founding teams of two or three people that previously required sales organizations of ten or more.

For investors, this changes the entry calculus. Companies that previously raised pre-revenue now arrive with one million dollars ARR and negotiate from a position of demonstrated momentum. The capital efficiency of the top companies in W26 is not a negotiating tactic — it is a genuine consequence of the current tooling environment.

3. Infrastructure Beats Application at the Valuation Layer

Looking across the eight profiled companies, the highest investor heat clusters around infrastructure plays: satellite power, file transfer protocols, lunar construction materials, AI training data pipelines. Not application-layer products sitting on top of existing infrastructure, but the infrastructure itself.

This pattern is consistent with how venture capital creates outsized returns historically. Infrastructure businesses, when successful, tend to be defensible through technical switching costs rather than network effects or brand. They serve every application built on top of them. And they compound in value as their dependent ecosystem grows. The W26 batch appears to contain more credible infrastructure bets per company than any recent YC cohort — which explains the valuation premium visible at the top of the batch.

4. Geographic Concentration Is Breaking Down

The W26 database places 66 percent of companies in the San Francisco Bay Area, which sounds like concentration until one observes the trend line. International founder representation has grown meaningfully over the past five years. Stilta's Swedish founders and GrazeMate's Australian-origin story are illustrative of a broader pattern: the most talented founders increasingly do not relocate to San Francisco as a prerequisite for backing.

YC's sustained international outreach has built pipelines from Stockholm, Sydney, Bangalore, Seoul, and dozens of other cities. The practical implication for investors is that exceptional technical talent is now discoverable globally, and that regional patterns — Swedish engineering discipline, Australian resourcefulness in resource-intensive industries — have predictive value that investors are beginning to price explicitly.

490+ Pitch Decks That Raised Millions

Stop guessing what investors want. Get access to 496 real pitch decks used by startups that successfully raised funding.

- 📊 Real decks from funded startups

- 💡 Proven storytelling & slide structures

- 🚀 Learn what actually gets investors to say “yes”

- 🧠 Perfect for founders, freelancers & creators

Used by founders raising pre-seed to Series A

The Founder Playbook: What These 8 Companies Teach About Building in 2026

The patterns visible across the W26 top eight are not accidental. They reflect deliberate choices about market timing, product positioning, and go-to-market strategy. Founders building now or preparing to raise should internalize these lessons before the next Demo Day.

Revenue Before Demo Day Is the New Table Stakes

The era of arriving at a pitch event with a compelling vision and a beta product is effectively over for founders who want to compete for the most competitive term sheets. The companies that attracted the most aggressive investor interest in W26 had crossed meaningful revenue milestones before anyone outside YC knew their names.

This shifts the preparation calculus significantly. The question is no longer 'how do we tell a compelling story about what we will build?' It is 'how do we get to a number that removes uncertainty before the pitch?' With current AI tools compressing engineering time, the answer is more achievable than it has ever been — but it requires treating revenue as a prerequisite, not a post-funding goal.

Timing Windows Are More Valuable Than Total Addressable Market

Beyond Reach Labs, GRU Space, and GrazeMate are all operating in markets that have recently become viable in ways they were not five years ago. Satellite constellation growth has created demand for orbital power infrastructure that did not previously exist at scale. Artemis and commercial lunar programs have created a credible near-term market for lunar surface support. Agricultural labor shortages have made autonomous rangeland management economically attractive at drone price points.

Each of these founders identified a moment when a historically difficult market had recently become accessible. That identification — the recognition of a timing window — is more valuable than a large total addressable market that has been accessible for decades. Markets with long histories have entrenched competitors. Markets that recently became viable have none.

Infrastructure Positioning Commands Premium Exits

Byteport is building a protocol layer. Beyond Reach Labs is building orbital power infrastructure. Luel is building data pipeline infrastructure. None of these companies are competing in application markets. All of them are building layers that will serve every application built on top of them.

Founders who can position their products as infrastructure rather than applications — who can genuinely credentialize that positioning with technical depth rather than marketing framing — attract both higher valuations at seed and more institutional interest at growth stages. The reason is simple: infrastructure exit multiples are structurally higher than application multiples because the revenue is stickier and the competitive moat compounds with adoption.

Founder-Market Fit Has Replaced Product-Market Fit as the Primary Signal at Pre-Seed

GrazeMate's founder grew up on a 6,000-head cattle station. GRU Space's founder worked on NASA-funded technology before founding the company. Stilta's founders bring Swedish engineering culture shaped by a startup ecosystem that has produced several recent breakout companies. In each case, the founder's background provides insight, credibility, or network access that no outside competitor can easily acquire.

For founders evaluating which problems to pursue, the most durable foundation is the intersection of personal expertise and genuine market need. That intersection creates advantages that capital alone cannot replicate: faster customer development cycles, more accurate problem framing, shorter sales cycles with customers who trust the founder's domain fluency, and defensibility against well-funded late entrants who lack the same depth.

Positioning as Acceleration, Not Replacement, Wins in Regulated Markets

Stilta's success at Roche demonstrates a principle that applies across any regulated or professional-services market: products positioned as acceleration tools for existing professionals close faster, retain longer, and face lower regulatory and legal resistance than products positioned as replacements.

Patent attorneys at Roche are not worried about Stilta eliminating their roles. They are evaluating whether it makes them more thorough and more competitive against opposing counsel who might also adopt AI tools. That framing — acceleration over replacement — is a strategic positioning choice with measurable commercial consequences. It is also more accurate: AI tools at current capability levels genuinely augment expert judgment rather than replacing it.

Frequently Asked Questions

What is Y Combinator Demo Day and why does it matter?

Y Combinator Demo Day is the culminating event of each YC cohort, where founders pitch to venture capitalists, angel investors, journalists, and operators. YC's portfolio has generated over 600 billion dollars in combined alumni valuation, making Demo Day the most reliable early indicator of where startup capital and engineering talent will concentrate over the following several years.

How many companies were in the YC Winter 2026 batch?

The Winter 2026 cohort comprised approximately 196 companies across sectors including AI infrastructure, robotics, cybersecurity, healthcare, space tech, and consumer applications. Of those, 14 had crossed one million dollars in annualized revenue before Demo Day — the highest number in YC history.

What is the default valuation for a YC W26 company?

The standard W26 round is four million dollars on a 40-million-dollar post-money valuation. Companies with strong revenue traction are raising at 50 to 100 million dollars. The highest reported single-company valuation at W26 was approximately 200 million dollars — the highest Demo Day valuation in six years of tracking.

Which YC W26 companies showed the strongest early revenue?

Hex Security reported crossing one million dollars in annualized run-rate revenue within eight weeks of launch. Luel reported approaching two million dollars in ARR within six weeks. One unnamed company in the broader batch entered Demo Day at 27 million dollars ARR. These figures reflect a structural shift in how quickly AI-enabled companies can reach revenue milestones.

Why did investors fight over Hex Security specifically?

Hex Security combined three signals that investors rarely see simultaneously in a single early-stage company: an acute, documented, and growing customer pain (AI-powered cyberattacks); a product that demonstrably addresses that pain; and one million dollars in run-rate revenue within eight weeks of launch. The combination indicated that enterprises were buying without completing standard procurement cycles, which signals urgency severe enough to override institutional friction.

What separates the top-eight companies from the rest of the W26 batch?

Each of the eight companies flagged by multiple investors shared at least one of three characteristics: demonstrated revenue velocity that significantly exceeded historical benchmarks, a credible infrastructure position with large letters of intent, or a uniquely defensible founder-market fit. The companies that failed to generate competitive investor interest generally lacked all three — competent teams building real products in competitive markets without a structural edge.

What is the most important lesson from the YC W26 batch for early-stage founders?

Revenue before the pitch is no longer a differentiator — it is the expected baseline for top-tier companies. Founders who arrive at any major pitch event without demonstrable traction are competing for the portion of investor attention that elite companies have already vacated. AI tools have made it possible to reach early revenue milestones with small teams in short timeframes. The question is whether founders are treating that possibility as an expectation for themselves.

490+ Pitch Decks That Raised Millions

Stop guessing what investors want. Get access to 496 real pitch decks used by startups that successfully raised funding.

- 📊 Real decks from funded startups

- 💡 Proven storytelling & slide structures

- 🚀 Learn what actually gets investors to say “yes”

- 🧠 Perfect for founders, freelancers & creators

Used by founders raising pre-seed to Series A

Final Analysis: The Patterns That Will Define the Next Decade

The eight companies that attracted competitive investor interest at YC's Winter 2026 Demo Day are not randomly distributed across sectors. They cluster around a coherent thesis about where durable value will be created as AI tools compound across the entire startup ecosystem.

Infrastructure — whether orbital, protocol-level, data, or physical — is commanding the highest valuations and the most institutional interest. Revenue velocity has reset the definition of elite execution. Deep tech is becoming fundable at accelerator timelines for the first time in history. And founder-market fit, particularly for physical-world problems, is emerging as the primary signal that sophisticated investors are pricing at pre-seed.

The companies that will matter most from the W26 batch are probably not the ones generating the most press coverage today. The most valuable infrastructure businesses rarely announce themselves loudly. They become indispensable quietly, and then suddenly everyone is dependent on them.

That dynamic — from invisible to indispensable — is the pattern that YC Demo Day has surfaced reliably for two decades. The W26 batch, by every quantitative measure available, offers more legitimate candidates for that trajectory than any cohort that preceded it.

Track accordingly.