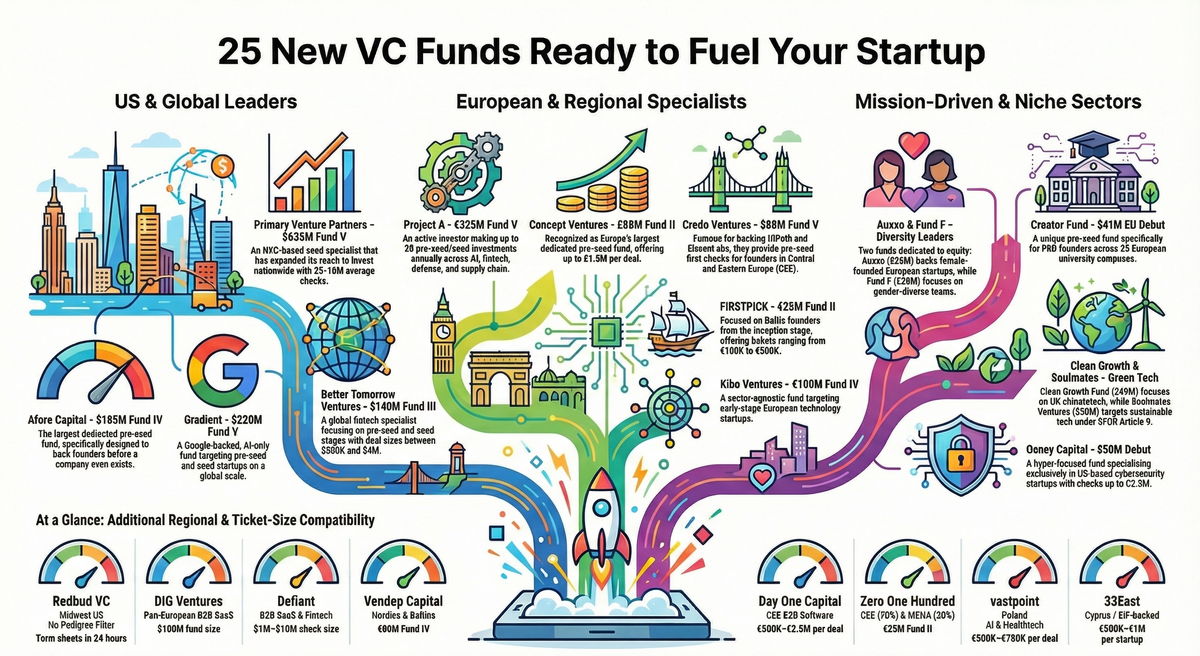

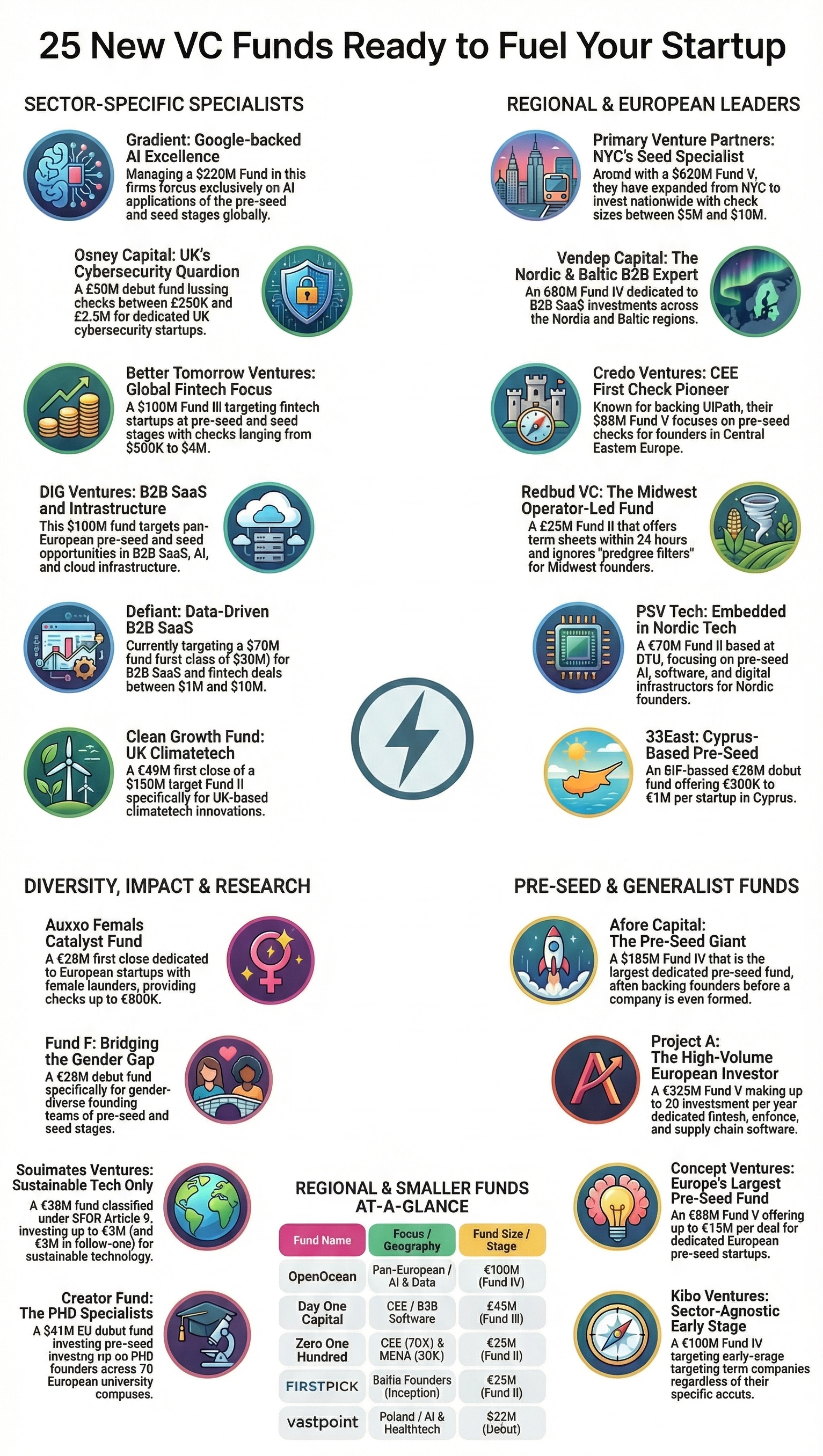

25 Fresh VC Funds Ready to Back Founders Right Now

A Complete Guide to Newly Raised Venture Capital Funds Actively Deploying Capital

Fundraising timing matters more than most founders realize. When a venture capital firm has just closed a new fund, the partners are under pressure to deploy capital. Term sheets move faster. Decision cycles shorten. Deal momentum is at its highest. That window, right after a fund close, is among the best possible moments to pitch.

The funds listed below have all raised new capital recently and are actively looking for companies to back. Each one represents a specific thesis, geography, or stage focus. Whether a founder is building a B2B SaaS product in Warsaw, an AI startup in London, a fintech platform in San Francisco, or a climate technology company in the UK, there is a fund here that is designed specifically for that kind of company.

This guide covers all 25 funds in depth, organized by geography and focus, with research-backed context, key takeaways, and a comprehensive comparison table. The goal is to give founders a clear, actionable map of where fresh capital is waiting to be deployed.

🚀 1000+ Angel Investors

A massive, curated list of angel investors actively funding early-stage startups.

Whether you're building your first product or scaling fast — this is your shortcut to reaching the right backers.

- ✔️ 1000+ verified angel investors

- ✔️ Early-stage & seed-focused

- ✔️ Save months of investor research

- ✔️ Built for founders, freelancers & creators

Limited-time access. Get in front of investors before everyone else does.

The State of Early-Stage Venture Funding

Early-stage venture capital has undergone a significant structural shift over the past few years. The era of cheap capital and frothy valuations that defined 2020 to 2022 gave way to a more disciplined investing environment, one where investors demand leaner teams, cleaner cap tables, and longer runway expectations before writing checks.

But the capital has not disappeared. According to data from Carta, the pre-seed market in 2025 remained remarkably active, with investor volume reaching a point where fewer instruments were being issued but aggregate dollars invested stayed resilient. In Q4 2025 alone, startups raised approximately $2.62 billion at the pre-seed stage even as instrument volume hit a recent low. This signals a market characterized by concentration: investors are writing larger checks into fewer, higher-conviction companies.

The bifurcation of the seed market is real. AI-related startups attracted a disproportionate share of capital, with roughly half of all venture capital raised in 2025 flowing to just one percent of companies. Meanwhile, founders building infrastructure, cybersecurity, B2B SaaS, and fintech continue to find receptive audiences from specialist funds that have maintained discipline throughout the cycle.

Post-money SAFEs remain the dominant instrument, accounting for approximately 92% of pre-seed rounds according to Carta. The average seed-stage team in 2025 had just 6.2 equity-holding employees, down sharply from a peak of over 10 in 2021, reflecting the influence of AI tooling on small team productivity and investor preferences for capital efficiency.

The geographic expansion of early-stage investing is another defining trend. Funds that previously focused almost exclusively on San Francisco or New York are now writing checks into Chicago, Warsaw, the Baltics, the Nordics, and Central Eastern Europe. The talent exists everywhere, and the best investors have followed it there.

|

Key Takeaways |

|

•

Pre-seed activity in

2025 outpaced 2024 even as individual round volumes declined, pointing to

larger, more selective checks. |

|

•

Post-money SAFEs now

represent 92% of pre-seed instruments, making them the standard mechanism for

early fundraising. |

|

•

Capital is

increasingly concentrated in AI, infrastructure, and cybersecurity, but

specialist funds in fintech, climate, and SaaS remain active. |

|

•

Geographic

diversification is accelerating, with meaningful early-stage ecosystems now

active across Europe, the Nordics, CEE, and MENA. |

|

•

The best time to pitch

a VC fund is immediately after it has closed, when deployment pressure is

highest and partner attention is freshest. |

North America: US-Based Funds Actively Deploying

The United States remains the largest early-stage venture market in the world, but the geography of deal-making has shifted away from purely coastal hubs. The five funds below represent a spectrum from the world's largest dedicated pre-seed firm to a lean Midwest operator-led fund with a deliberate anti-pedigree philosophy.

1. Afore Capital – Largest Dedicated Pre-Seed Fund in the World

|

Afore

Capital |

|

Fund Size: $185M

Fund IV Check Size: $50K to

$2M+ Focus: Software, all

sectors, product-oriented founders Geography: USA (San

Francisco) with global reach Notable:

Portfolio includes Modern Health, BenchSci, Hightouch ($1.2B valuation), Neo

Financial, Gamma |

Founded in 2016 by Anamitra Banerji and Gaurav Jain, Afore Capital has done more to define the pre-seed category than virtually any other firm. When the fund launched, only 14% of early rounds were classified as pre-seed. By 2023, that share had grown to nearly 60% of all seed deals, according to Crunchbase, a shift Afore helped drive.

Fund IV at $185 million is the firm's largest to date and again holds the distinction of being the world's largest dedicated pre-seed vehicle. The fund backs approximately 35 to 40 pre-seed companies per year, alongside 50 to 75 founders who go through the firm's eight-week Founders-in-Residence program, known as FIR.

The FIR program is what makes Afore structurally different from almost every other investor at this stage. Rather than requiring founders to arrive with a polished pitch, a validated idea, and a co-founder, Afore actively works with aspiring entrepreneurs who are still in the ideation phase. Cohorts of five to eight founders work together for eight to ten weeks, with hands-on mentorship from the Afore team, access to the firm's community of over 10,000 potential customers, and a minimum investment of $100,000 simply for entering the program.

For founders who already know what they want to build, checks run from $500,000 to $2 million or more, depending on the situation. Afore calls its current approach Pre-Seed 2.0, a philosophy of flexibility tailored to where each founder actually is, not where investors want them to be.

The firm's track record supports the thesis. Across its 200-company portfolio, the collective market capitalization now exceeds $13.5 billion. Afore returned more than the full value of its first $47 million fund to limited partners in a single six-month period, a rare achievement in a cycle when most early-stage funds have struggled with distributions.

|

Key Takeaways |

|

•

Afore is the world's

largest dedicated pre-seed fund, with $185M in Fund IV and a 200-company

portfolio valued at over $13.5 billion collectively. |

|

•

The

Founders-in-Residence program is unique in the market, accepting builders who

have not yet formed a company or finalized an idea. |

|

•

Check sizes range from

$50,000 to more than $2 million, making Afore accessible to founders at very

different stages of readiness. |

|

•

The firm accepts both

warm introductions and cold outreach from founders and has offices in San

Francisco's South Park neighborhood. |

|

•

Follow-on support is

strong, with a 34x ratio of follow-on capital sourced through Afore

introductions. |

2. Gradient – Google-Backed, AI-Only Global Fund

|

Gradient

Ventures |

|

Fund Size: $220M

Fund V Check Size: Varies by

deal Focus: Artificial

intelligence applications only, pre-seed and seed globally Geography: Global Notable:

Google-backed; portfolio includes Observe.AI, Lilt, Labelbox |

Gradient Ventures is Google's AI-focused venture fund, and Fund V at $220 million represents one of the largest dedicated AI-only vehicles at the early stage globally. Unlike most corporate venture arms, Gradient operates with a high degree of autonomy and writes checks at the pre-seed and seed stages, competing directly with independent VC firms rather than only participating in later-stage growth rounds.

The fund's thesis is straightforward: every industry vertical will be redefined by artificial intelligence, and the best time to back those companies is before the disruption is obvious. Gradient's investment focus spans AI applications across healthcare, legal, logistics, education, software development, customer service, and data infrastructure.

What makes Gradient distinctive beyond the Google name is the access to infrastructure and expertise that portfolio companies receive. Founders backed by Gradient gain exposure to Google's engineering culture, access to early conversations with Google Cloud teams, and potential pathways for enterprise sales through Google's existing customer relationships. This is particularly valuable for AI companies that depend on large-scale compute access and enterprise distribution.

The fund invests globally, including in European and Asian founders, and has developed a reputation for moving quickly at the term sheet stage. For founders building AI-native products or applying machine learning to specific industry problems, Gradient represents a combination of capital and strategic value that few funds can match.

|

Key Takeaways |

|

•

Gradient is Google's

dedicated early-stage AI fund with $220M in Fund V, investing globally at

pre-seed and seed stages. |

|

•

Portfolio companies

gain meaningful strategic access to Google's cloud infrastructure,

engineering expertise, and enterprise customer networks. |

|

•

The fund operates

independently within Google, allowing it to compete with traditional VCs at

the earliest stages. |

|

•

AI-only focus means

founders outside the AI category should look elsewhere, but for AI-native

companies this fund represents exceptional strategic fit. |

3. Primary Venture Partners – NYC Seed Specialist Now Backing Founders Nationwide

|

Primary

Venture Partners |

|

Fund Size: $625M

Fund V Check Size: $5M to $10M

average check Focus: Generalist seed;

vertical AI, fintech, healthcare, cybersecurity, infrastructure, consumer Geography: USA

(nationwide, historically NYC) Notable:

Portfolio includes Etched, Alloy, Chief, Dandelion Health; $1.65B AUM total |

Primary Venture Partners is one of New York's most established seed-stage funds, but Fund V at $625 million marks a significant evolution in both scale and geography. Founded in 2015 with a $60 million debut fund, the firm has grown steadily through five vehicles, accumulating over $1.65 billion in assets under management.

The $5 million to $10 million average check size puts Primary in a distinct position: this is not a fund for founders raising their first $500,000 on a SAFE. Primary leads at the seed stage and invests into companies that have reached a level of clarity about their market, their go-to-market approach, and their founding team. The fund plans to invest in 40 to 50 companies over approximately three years.

The geographic thesis has shifted materially. While Primary built its reputation as a New York fund, co-founder and general partner Ben Sun has been explicit that the firm now writes checks across San Francisco, Chicago, Seattle, Virginia, and Washington D.C. The underlying belief is that exceptional founders and world-changing startups are emerging everywhere, and a coastal bias in sourcing is a competitive liability, not a strength.

Primary operates with sector specialists covering vertical AI, fintech, healthcare, enterprise software, cybersecurity, and infrastructure, allowing the firm to offer genuine domain expertise rather than generalist advice. The firm's view is that seed investing has matured into its own distinct asset class, one that requires dedicated expertise, deep networks, and meaningful capital to compete effectively at the portfolio level.

|

Key Takeaways |

|

•

Primary's $625M Fund V

is one of the largest seed-stage funds in the US, with $5M to $10M average

check sizes and plans for 40 to 50 investments. |

|

•

The firm has expanded

from a NYC-centric fund to a nationwide investor, with active deals in

Chicago, Seattle, D.C., and San Francisco. |

|

•

Sector specialists in

AI, fintech, healthcare, and cybersecurity allow Primary to offer genuine

domain knowledge alongside capital. |

|

•

Fund V has already

deployed into initial companies, meaning the fund is actively deploying right

now. |

4. Redbud VC – Operator-Led Midwest Fund Without a Pedigree Filter

|

Redbud

VC |

|

Fund Size: $25M Fund

II Check Size: Varies Focus: Tech startups,

operator-founded and operator-centric Geography: USA

(Midwest) Notable:

Offers term sheets within 24 hours; no elite network required |

Redbud VC represents a deliberate counter-narrative to the coastal venture establishment. The fund is operator-led, Midwest-based, and has built its identity around the explicit rejection of pedigree-based pattern matching. While many venture firms rely heavily on warm introductions from trusted networks, elite university affiliations, and recognizable prior employer logos, Redbud has committed to evaluating founders on the quality of their ideas and execution rather than their backstory.

The 24-hour term sheet commitment is among the fastest decision timelines in early-stage venture. For founders who have experienced the frustration of months-long VC processes with ambiguous feedback, this is a meaningful differentiator. The Midwest focus also means Redbud is working in markets with lower competition for deals, lower cost structures for portfolio companies, and access to deep talent pools in industries like manufacturing, logistics, agriculture technology, and enterprise software.

Fund II at $25 million is intentionally small relative to the coastal giants. This keeps the firm nimble, maintains genuine alignment between partners and portfolio founders, and ensures that Redbud's partners are personally involved in every company rather than distributed thinly across a massive portfolio. For founders who want an engaged, hands-on partner rather than a name on the cap table, Redbud's approach is distinctive.

|

Key Takeaways |

|

•

Redbud makes term

sheet decisions within 24 hours, one of the fastest timelines in early-stage

US venture. |

|

•

No pedigree filter

means founders without elite university or employer backgrounds are actively

welcomed. |

|

•

Midwest focus gives

Redbud a structural advantage in a region where quality deal competition is

lower than on the coasts. |

|

•

Fund II at $25M keeps

the partnership small and ensures genuine hands-on engagement with every

portfolio company. |

5. Better Tomorrow Ventures – Global Fintech Pre-Seed and Seed

|

Better

Tomorrow Ventures |

|

Fund Size: $140M

Fund III Check Size: $500K to

$4M per deal Focus: Fintech

globally, with vertical SaaS and marketplace businesses Geography: Global Notable:

Founded by Sheel Mohnot (ex-500 Fintech) and Jake Gibson (NerdWallet

co-founder) |

Better Tomorrow Ventures occupies a unique position in the fintech investment landscape: every member of the investment team is a former fintech operator or founder rather than a career investor. This background gives the firm unusual credibility with founders and allows partners to engage with product, regulatory, and go-to-market challenges in a way that generalist investors typically cannot.

The firm was founded in 2019 by Sheel Mohnot, who previously built and sold two fintech companies before running the 500 Fintech accelerator, and Jake Gibson, co-founder of NerdWallet, which went public on Nasdaq. This founding team background means BTV brings both operator empathy and outcome experience to every portfolio relationship.

Fund III at $140 million plans to invest in 30 to 35 companies, with checks ranging from $500,000 to $3.5 million. The firm is deliberately bullish on fintech at a moment when broader venture enthusiasm for the sector has moderated following the interest rate cycle of 2022 to 2024. The partners' view is that the fundamental digitization of financial services remains enormously underpenetrated, and that the current climate of reduced competition for deals is actually favorable for long-term returns.

BTV takes a broad definition of fintech, including vertical SaaS businesses and marketplace models where financial services are embedded in the product. Global founders are actively considered, and the firm has backed companies across the US, Europe, and emerging markets.

|

Key Takeaways |

|

•

BTV's entire

investment team consists of former fintech operators, providing founders with

hands-on tactical support rather than generic VC advice. |

|

•

$140M Fund III plans

30 to 35 investments with $500K to $3.5M checks, actively deploying across

global fintech founders. |

|

•

The firm maintains a

bullish thesis on fintech even as broader market enthusiasm has moderated,

viewing reduced competition as a return opportunity. |

|

•

BTV takes a broad

definition of fintech, including embedded finance in vertical SaaS and

marketplace businesses. |

💼 1000+ Angel Investors Database

A founder-grade investor list designed to help you raise faster. No guesswork. No outdated contacts.

- ✔️ Handpicked investor database

- ✔️ Early-stage focused

- ✔️ Save weeks of research

- ✔️ Used by startup founders

United Kingdom and Western Europe: Fresh Capital Across the Atlantic

European early-stage venture has experienced significant maturation over the past decade. The emergence of breakout companies from the continent, including Klarna, Wise, UiPath, ElevenLabs, Revolut, and dozens of others, has attracted institutional capital from the US and built a self-reinforcing ecosystem of experienced founders becoming angels and fund managers. The following seven funds represent some of the most active newly capitalized vehicles in the UK and Western European market.

6. Concept Ventures – Europe's Largest Dedicated Pre-Seed Fund

|

Concept

Ventures |

|

Fund Size: $88M Fund

II Check Size: Up to $1.5M

per deal, $1M average Focus: Pre-seed, all

sectors, UK and European founders Geography: UK and

Europe Notable:

Early investor in ElevenLabs; 80% of LPs based in the US |

Concept Ventures holds the distinction of running Europe's largest dedicated pre-seed fund, with $88 million raised for Fund II. The firm's investment approach centers on writing first institutional checks into UK and European founders at the earliest possible stage, typically before a company has significant revenue or an established product.

The ElevenLabs association is particularly significant. Concept was among the earliest investors in the AI voice company, which has since reached a valuation of approximately $11 billion. That investment trajectory has attracted substantial US institutional capital into Fund II, with approximately 80% of the firm's limited partners based in the United States and more than 70% consisting of the firm's own portfolio founders reinvesting.

The fund plans to back up to 50 companies from this vehicle, with an average ticket of $1 million. This positions Concept to be a meaningful first partner rather than a small angel check, while remaining accessible enough to back companies at true ideation stages. The team's willingness to engage with founders who do not yet have revenue or a completed product reflects a genuine pre-seed philosophy rather than what many European funds label as pre-seed but actually constitutes early seed investing.

|

Key Takeaways |

|

•

Concept Ventures runs

Europe's largest dedicated pre-seed fund at $88M, with plans to back up to 50

UK and European startups. |

|

•

The ElevenLabs early

investment has dramatically raised the firm's profile and attracted 80% US LP

participation in Fund II. |

|

•

$1M average tickets

mean Concept is a substantive first partner, not a small angel-equivalent

check. |

|

•

The firm's portfolio

founders reinvesting as LPs creates a self-reinforcing community of aligned

stakeholders. |

7. DIG Ventures – Pan-European B2B SaaS and AI at Pre-Seed and Seed

|

DIG

Ventures |

|

Fund Size: $100M Check Size: N/A Focus: B2B SaaS, AI,

cloud infrastructure Geography: Pan-European Notable:

Focus on enterprise software at pre-seed and seed stages |

DIG Ventures operates as a pan-European fund focused specifically on B2B SaaS, artificial intelligence, and cloud infrastructure companies. The $100 million fund invests at the pre-seed and seed stages, positioning itself as an early partner for European founders building enterprise software products with global ambitions.

The B2B SaaS focus reflects a deliberate specialization. Enterprise software businesses benefit from predictable revenue models, high retention rates, and strong unit economics once product-market fit is established. Cloud infrastructure investments complement this thesis by targeting the foundational layer on which SaaS applications are built. Together, these two focus areas give DIG a coherent portfolio strategy where companies can learn from and support each other.

As a pan-European investor, DIG does not limit its geographic reach to a single country or sub-region, giving founders across the continent access to the fund. This is particularly relevant for founders in smaller startup ecosystems who may struggle to attract London-centric or US-based investors without already having an established presence in a major tech hub.

|

Key Takeaways |

|

•

DIG Ventures brings

$100M to pan-European B2B SaaS and AI at pre-seed and seed stages. |

|

•

The focus on

enterprise software and cloud infrastructure creates a portfolio with

coherent shared learning and mutual support opportunities. |

|

•

Pan-European

geographic mandate means founders in smaller ecosystems are actively

considered alongside those in major hubs. |

8. Osney Capital – UK Cybersecurity Specialist

|

Osney

Capital |

|

Fund Size: £50M

debut fund Check Size: £250K to

£2.5M per check Focus: Cybersecurity

only Geography: UK Notable:

Only UK-based dedicated cybersecurity fund at this stage |

Osney Capital is the only dedicated cybersecurity venture fund operating at the pre-seed and seed stages in the United Kingdom. The £50 million debut fund fills a structural gap in the UK ecosystem, where cybersecurity startups have historically had to compete for attention from generalist funds that lack deep sector expertise.

The cybersecurity investment thesis is compelling from a market standpoint. Global spending on cybersecurity continues to grow at a significant pace, driven by the proliferation of cloud infrastructure, the rise of AI-enabled attack vectors, and increasingly stringent regulatory requirements across Europe and the UK. Early-stage companies that build deep technical capabilities in identity, threat detection, data protection, or security automation can grow into substantial businesses serving enterprise and government customers.

With check sizes ranging from £250,000 to £2.5 million, Osney can lead or co-lead rounds at both the earliest pre-seed stage and into seed. The dedicated sector focus means Osney's partners bring a level of domain expertise in cybersecurity that generalist investors cannot replicate, and the fund's network of potential customers, advisors, and follow-on investors within the sector is specifically built for this space.

|

Key Takeaways |

|

•

Osney is the only

UK-based dedicated cybersecurity fund at the pre-seed and seed stages,

filling a structural gap in the ecosystem. |

|

•

Check sizes from £250K

to £2.5M allow Osney to lead rounds at both early pre-seed and seed, giving

founders a flexible entry point. |

|

•

Deep sector expertise

enables Osney to provide customer introductions, technical diligence, and

follow-on investor connections that generalists cannot. |

9. Creator Fund – Pre-Seed for PhD Founders Across 28 European University Campuses

|

Creator

Fund |

|

Fund Size: $41M EU

debut fund Check Size: N/A Focus: PhD and

deep-tech academic founders Geography: Europe (28

university campuses) Notable:

Anchored by Equation Capital and Denmark's EIFO; 60+ LPs |

Creator Fund has built its entire strategy around backing PhD founders and deep-tech researchers who are spinning out of European university environments. With a presence across 28 European university campuses, the fund is embedded directly in the institutions where the next generation of technical founders is working on breakthrough research.

The $41 million debut EU institutional fund, doubled from a prior UK-focused vehicle, represents a significant step up in the firm's ability to support academic founders through the transition from research to commercial product. The fund is anchored by Equation Capital and Denmark's EIFO, joined by more than 60 limited partners, signaling strong institutional conviction in the university spinout opportunity.

PhD founders face distinctive challenges that Creator Fund is specifically designed to address. Academic researchers often have world-class technical depth but limited exposure to commercial go-to-market strategy, customer development, hiring, and fundraising. Creator's campus presence allows the fund to build relationships with founders before they are ready to raise, and to provide mentorship through the commercialization process in a way that requires genuine proximity to the university environment.

|

Key Takeaways |

|

•

Creator Fund is

uniquely positioned at 28 European university campuses to source PhD and

deep-tech founders before they reach the open market. |

|

•

$41M debut EU fund is

doubled from the prior UK vehicle, reflecting strong LP conviction in the

academic spinout opportunity. |

|

•

The fund is

specifically designed to help researchers navigate the transition from

academic work to commercial product, addressing a real gap in founder

support. |

10. Defiant – Data-Driven B2B SaaS and Fintech

|

Defiant |

|

Fund Size: $30M

first close, targeting $70M Check Size: $1M to $10M

per deal Focus: B2B SaaS,

fintech Geography: USA / Global Notable:

Data-driven approach to sourcing and diligence |

Defiant occupies an interesting position in the early-stage landscape, offering check sizes from $1 million to $10 million, which is larger than most pre-seed investors but more flexible than many traditional seed funds. This range allows the firm to participate both at the earliest stages and to lead meaningful rounds for companies with early traction.

The data-driven approach to sourcing and diligence that defines Defiant's methodology reflects a broader trend in venture capital toward systematic deal evaluation rather than purely relationship-driven investing. By using data signals to identify promising companies earlier and evaluate them more consistently, Defiant aims to find opportunities that are being missed by funds that rely primarily on warm networks and founder pedigrees.

At $30 million for the first close and targeting $70 million total, the fund is actively deploying capital while continuing to build toward its final target. This creates an interesting moment for founders: the fund is in active deployment mode, partners are eager to find strong companies, and the fund is operating with the urgency that characterizes an early deployment phase.

|

Key Takeaways |

|

•

Defiant offers $1M to

$10M check sizes, bridging the gap between pre-seed and early seed, with

flexibility on timing within that range. |

|

•

Currently in

first-close deployment with $30M raised against a $70M target, meaning

partners are actively looking for companies now. |

|

•

Data-driven sourcing

methodology allows Defiant to identify opportunities outside of traditional

warm-intro networks. |

11. Project A – Up to 20 Early-Stage Investments Per Year

|

Project

A |

|

Fund Size: €325M

Fund V Check Size: N/A Focus: AI, fintech,

defence, supply chain software, pre-seed and seed Geography: Europe Notable:

Berlin-based; one of Europe's most active early-stage investors |

Project A is one of Europe's most active early-stage venture firms, with a commitment to making up to 20 pre-seed and seed investments annually from Fund V. At €325 million, this is a substantial vehicle for the European market, and the focus areas reflect both the current moment in technology and some of the most significant long-term opportunity areas.

The inclusion of defence technology as a focus area is notable. Across Europe, there is a growing recognition that dual-use technology and defence-adjacent software represent both a moral and commercial opportunity, as governments increase defence budgets and seek modern software solutions for logistics, intelligence, communications, and systems management. Project A's willingness to invest in this space signals a forward-looking thesis that is increasingly shared by major institutional capital in Europe.

AI, fintech, and supply chain software round out the focus areas, creating a portfolio mix that covers both horizontal AI infrastructure and vertical applications in industries with large total addressable markets. The Berlin-based firm has built one of Europe's most comprehensive platform support offerings for portfolio companies, including dedicated teams for recruiting, marketing, and business development.

|

Key Takeaways |

|

•

Project A makes up to

20 early-stage investments per year from a €325M fund, making it one of

Europe's highest-volume dedicated early-stage investors. |

|

•

Defence technology

focus distinguishes Project A in a market where most funds are still

reluctant to engage with this sector. |

|

•

Berlin-based platform

includes dedicated recruiting, marketing, and business development teams

available to all portfolio companies. |

12. Auxxo Female Catalyst Fund – Pre-Seed and Seed for Female-Founded European Startups

|

Auxxo

Female Catalyst Fund |

|

Fund

Size: €26M first close Check

Size: €350,000 to €800,000 per deal Focus:

Female-founded European startups at

pre-seed and seed stages, sector-agnostic Geography:

Europe Notable:

One of the largest dedicated

female-founder-focused funds in the European venture ecosystem |

Auxxo Female Catalyst Fund is built on a commercial thesis as much as a social one: female-founded companies represent one of the most systematically underpriced opportunities in European venture capital, and dedicated capital with the right founder relationships and support infrastructure can generate competitive returns precisely by addressing a market inefficiency that most funds ignore or only superficially engage with.

The evidence supporting this thesis is well-documented. Female founders receive a disproportionately small share of total venture capital relative to both their frequency in the founder population and the performance of companies they lead. Multiple academic and industry studies have shown that mixed-gender and female-founded teams generate stronger risk-adjusted returns on average than all-male teams, yet the allocation of capital has not reflected this. Auxxo is built to capture this structural alpha.

With check sizes ranging from €350,000 to €800,000, Auxxo can lead or meaningfully co-lead rounds at the pre-seed and seed stages across a wide range of sectors. The fund is sector-agnostic, backing female founders across technology verticals including SaaS, fintech, health technology, deep tech, and consumer products. The first close of €26 million confirms the fund is actively deploying, and founders who match the criteria should be reaching out now while the fund is in its highest-urgency deployment phase.

|

Key Takeaways |

|

•

Auxxo is built on a

commercial thesis that female-founded companies are systematically

underpriced in European venture, creating a genuine alpha opportunity for

specialist capital. |

|

•

Check sizes of €350K

to €800K allow the fund to lead or meaningfully participate in pre-seed and

early seed rounds across all sectors. |

|

•

€26M first close means

the fund is in active deployment, making now an optimal time for female

founders in Europe to engage. |

|

•

The fund is

sector-agnostic, backing female founders across SaaS, fintech, health, deep

tech, and consumer verticals. |

13. Fund F – Pre-Seed and Seed for Gender-Diverse Founding Teams

|

Fund F |

|

Fund

Size: €28M debut fund Check

Size: Approximately €300,000 per

check Focus:

Gender-diverse founding teams

across Europe at pre-seed and seed stages Geography:

Europe Notable:

Debut fund with first close

completed and active deployment underway |

Fund F operates with a mandate centered on gender-diverse founding teams broadly, rather than specifically female-only founders. The fund's thesis is that mixed-gender teams bring complementary perspectives, communication styles, and market instincts that produce measurably different outcomes in customer research, product design, and organizational culture, and that the market has consistently underestimated this advantage.

At approximately €300,000 per check, Fund F operates at a smaller ticket size than Auxxo, positioning it as an accessible very-early-stage entry point for diverse founding teams that may be earlier in the ideation or product development process. The debut fund at €28 million is designed to build a portfolio of companies at the earliest possible stage, with the expectation that follow-on rounds from larger seed and Series A funds will be raised as companies progress.

Auxxo and Fund F serve complementary founder profiles rather than competing for the same companies. A team led by a female founder that has already achieved early product validation and is raising a meaningful seed round is a natural fit for Auxxo. A mixed-gender team at the pre-product ideation stage looking for a first small institutional check is a better fit for Fund F. Founders who understand both funds can route themselves appropriately and potentially engage with both as complementary investors in the same round.

|

Key Takeaways |

|

•

Fund F backs

gender-diverse founding teams broadly, not only female-only teams, with

approximately €300K checks at pre-seed and seed. |

|

•

Smaller check sizes

than Auxxo position Fund F as an accessible entry point for diverse teams at

the very earliest stages of product development. |

|

•

Fund F and Auxxo serve

complementary profiles and could potentially be co-investors in the same

round for the right founding team. |

|

•

Debut fund with €28M

and active deployment means Fund F is in its peak urgency phase for finding

the initial portfolio companies. |

💼 1000+ Angel Investors Database

A founder-grade investor list designed to help you raise faster. No guesswork. No outdated contacts.

- ✔️ Handpicked investor database

- ✔️ Early-stage focused

- ✔️ Save weeks of research

- ✔️ Used by startup founders

Northern Europe: Nordic and Baltic Funds on the Rise

The Nordic and Baltic startup ecosystems have produced an impressive number of category-defining companies relative to population size. Companies including Klarna, Spotify, Supercell, TransferWise (now Wise), and dozens of B2B software businesses have emerged from the region over the past fifteen years. The following funds are deploying fresh capital specifically targeting founders building in and from these markets.

14. Kibo Ventures – Pan-European Deep Tech and AI from Spanish Roots

|

Kibo

Ventures |

|

Fund

Size: €100M+ Fund IV (targeting

€120M) Check

Size: Approximately €5M lead check

with 40 percent reserved for follow-on Focus:

Deep tech, AI, robotics,

cybersecurity, and vertical software at seed and Series A Geography:

Pan-European (Madrid and Barcelona

roots, expanding to Berlin, Paris, and London) Notable:

Portfolio: 4 unicorns and 1 IPO

over 13 years; exits to Apple, Airbnb, Crowdstrike, and PayPal; Fund IV

investments include THEKER Robotics ($21M seed led by Kibo) and anyformat |

Kibo Ventures was founded in 2012 in Madrid and has grown from a €43 million debut fund to more than €500 million in assets under management across multiple funds and investment vehicles. Fund IV, which has secured more than €100 million in commitments against a €120 million target, represents a deliberate strategic expansion from Southern European roots to a fully pan-European investment mandate.

The firm's technology focus has sharpened with each successive fund. While early funds backed a broader range of technology companies, Fund IV concentrates on deep tech, AI infrastructure, robotics, cybersecurity, and vertical software applications, with particular emphasis on companies where technical depth is the primary competitive moat rather than distribution or marketing. Early Fund IV investments include THEKER Robotics, where Kibo led a $21 million seed round, one of the largest seed rounds in European robotics, and anyformat, a generative AI platform for enterprise document structuring.

Kibo leads seed and Series A rounds, typically committing around €5 million per initial investment with 40 percent of the fund reserved for follow-on rounds in successful portfolio companies. The appointment of Sunir Kapoor as Chairman brings transatlantic perspective and experience across both European and Silicon Valley ecosystems, strengthening Kibo's ability to help portfolio companies expand into the US market, which is a critical milestone for most B2B deep tech and software companies building for global scale.

The firm has backed more than 70 companies across its history, achieving four unicorns and one IPO with exits including acquisitions by Apple, Airbnb, Crowdstrike, and PayPal. This track record across multiple market cycles is the strongest evidence of sustained investment quality and founder-selection ability in Southern European venture.

|

Key Takeaways |

|

•

Kibo Ventures has

produced 4 unicorns and 1 IPO across 70+ portfolio companies with exits to

Apple, Airbnb, Crowdstrike, and PayPal, providing one of Southern Europe's

strongest track records. |

|

•

€100M+ Fund IV is

expanding from Southern European roots to a fully pan-European mandate across

Berlin, Paris, and London alongside Madrid and Barcelona. |

|

•

Fund IV leads seed and

Series A rounds at approximately €5M per deal with 40 percent reserved for

follow-on in successful companies. |

|

•

Deep tech, robotics,

cybersecurity, and AI infrastructure focus means founders need genuine

technical depth rather than distribution advantages to attract Kibo's

attention. |

|

•

The Chairman

appointment of Sunir Kapoor strengthens Kibo's ability to connect portfolio

companies to US markets and enterprise customer relationships. |

15. OpenOcean – European AI and Data Infrastructure at Seed and Series A

|

OpenOcean |

|

Fund

Size: €100M Fund IV (targeting

€130M final close) Check

Size: Up to €6M per initial

investment Focus:

AI-native software, data

infrastructure, and business software at seed and Series A Geography:

Pan-European with selective global

reach Notable:

Founded by creators of MySQL and

MariaDB; portfolio includes IQM (quantum computing), MindsDB, Supermetrics,

Booksy, Binalyze, Truecaller (IPO) |

OpenOcean carries a genuinely unusual founding story in European venture: the firm was established by the creators of MySQL and MariaDB, two of the most widely deployed open-source database technologies in the world. This technical heritage is not marketing biography but active operational DNA. General Partners Tom Henriksson and Patrik Backman bring direct experience building and scaling fundamental software infrastructure to hundreds of millions of users, a perspective that shapes how OpenOcean evaluates technical claims, architectural choices, and long-term defensibility in ways that most investor teams cannot replicate.

Fund IV at €100 million, with a €130 million final close target, focuses on AI-native software, data infrastructure, and business software at the seed and Series A stages. The fund's thesis is that data remains the fundamental moat in AI, even as the capabilities of foundation models become more democratized. Companies that build proprietary data networks, unique data processing pipelines, or deeply integrated workflows where data quality compounds over time will maintain durable competitive advantages even as underlying model capabilities improve.

OpenOcean has already made initial Fund IV investments including Embeddable, a customer-facing analytics startup for enterprise developers, and Dreamfold.ai, a protein search and design AI platform backed from North America. The Dreamfold investment signals that OpenOcean's pan-European mandate has genuine flexibility to back standout technical teams globally when the opportunity meets the investment thesis. The fund also led the Series A of Authologic, a Polish e-ID platform, demonstrating active engagement with the CEE ecosystem alongside major Western European hubs.

With notable exits including Truecaller's IPO and acquisitions by Moodys, SAP, Altair, and Citrix, OpenOcean has built a track record of identifying software companies with genuine enterprise defensibility and scaling them to material outcomes across multiple market cycles.

|

Key Takeaways |

|

•

OpenOcean was founded

by the creators of MySQL and MariaDB, giving the firm genuinely unusual

technical depth in evaluating data infrastructure and software companies. |

|

•

€100M Fund IV with

€130M target is actively deploying at seed and Series A, with initial

investments in AI analytics, protein design AI, and identity verification

software. |

|

•

The data-moat thesis

focuses on companies with proprietary data networks or unique workflow

integrations that compound defensibility over time as models improve. |

|

•

Pan-European mandate

with selective global reach means technically exceptional teams outside

Europe are evaluated when the thesis fits strongly. |

|

•

Notable exits

including Truecaller's IPO and acquisitions by Moodys, SAP, Altair, and

Citrix demonstrate consistent ability to build enterprise software companies

to material outcomes. |

16. Vendep Capital – B2B SaaS Specialist Across the Nordics and Baltics

|

Vendep

Capital |

|

Fund

Size: €80M Fund IV Check

Size: €100,000 to €3M per initial

investment, with follow-on in later rounds Focus:

B2B SaaS from pre-seed to Series A,

with emphasis on AI-first product design Geography:

Nordics and Baltics (headquartered

in Espoo, Finland) Notable:

Portfolio: AlphaSense, Hostaway,

Leadfeeder, Happeo, Syncle; backed by Tesi, Pension Insurance Company Elo,

Sitra, and other Finnish institutional investors |

Vendep Capital has operated as one of Northern Europe's most consistent B2B SaaS specialists since its founding in 2013. Fund IV at €80 million is the firm's largest vehicle to date and arrives at what the partners describe as the most interesting period for SaaS in the firm's history. While parts of the broader venture market have been skeptical about SaaS valuations in the context of AI disruption, Vendep's view is precisely the opposite: almost every meaningful AI product today is delivered and monetized as SaaS, built on cloud infrastructure, recurring revenue models, and data-centric architectures.

The fund will invest in approximately 20 early-stage SaaS companies across the Nordics and Baltics, from pre-seed to Series A, with initial tickets ranging from €100,000 to €3 million. The flexibility of this range is significant: it allows Vendep to engage with founders at inception and scale its commitment as companies prove their thesis, rather than requiring a specific level of traction before writing the first check.

The Nordic and Baltic SaaS ecosystem has produced genuinely remarkable companies at a per-capita rate that is difficult to explain by market size alone. The combination of strong engineering education, high English proficiency, proximity to enterprise-heavy Scandinavian industries in manufacturing, shipping, and financial services, and a cultural orientation toward global product design from the earliest stage creates conditions where SaaS founders build for international markets as a default rather than an afterthought. AlphaSense, one of Vendep's portfolio companies, raised over $650 million and reached a valuation of approximately $4 billion, demonstrating the scale of outcomes this ecosystem can produce.

Fund IV has already made initial investments, one in Denmark and one in Finland, and is maintaining an active deal pace. The fund's eight-person team of former founders and operators works closely with each portfolio company, offering a level of engagement that goes beyond a quarterly check-in.

|

Key Takeaways |

|

•

Vendep brings €80M in

Fund IV to Nordic and Baltic B2B SaaS from pre-seed to Series A, with €100K

to €3M initial tickets and follow-on reserved for successful companies. |

|

•

The firm's AI-first

SaaS thesis is that AI enhances rather than threatens the SaaS model, as

almost every meaningful AI product is delivered and monetized as SaaS. |

|

•

Portfolio company

AlphaSense reaching a $4B+ valuation demonstrates the scale of outcomes the

Nordic SaaS ecosystem can produce. |

|

•

Fund IV has already

made initial investments and is actively seeking additional companies in the

Nordics and Baltics right now. |

|

•

The eight-person team

of former founders and operators provides hands-on support beyond financial

capital. |

17. PSV Tech – Pre-Seed AI and Software for Nordic Founders, Embedded at DTU

|

PSV Tech |

|

Fund

Size: €70M Fund II Check

Size: Varies by deal Focus:

Artificial intelligence, software,

and digital infrastructure for Nordic founders at pre-seed Geography:

Nordics -- with physical presence

at the Technical University of Denmark (DTU) Notable:

Embedded at DTU, one of Northern

Europe's most technically excellent research universities |

PSV Tech has established a physical presence at the Technical University of Denmark, one of the highest-ranked technical research universities in Europe and a consistent producer of deep-tech and engineering founders. This campus embedding mirrors the approach taken by Creator Fund across a broader network of European universities, and reflects a shared recognition among the most forward-thinking pre-seed investors that proximity to the environments where the next generation of technical founders is working is the most durable competitive advantage in early-stage investing.

Fund II at €70 million gives PSV Tech meaningful capital to deploy at the pre-seed stage for Nordic founders working in artificial intelligence, software development, and digital infrastructure. The university embedding creates a natural sourcing moat: PSV can identify exceptional founders during their PhD or Master's programs, build relationships over extended periods before a company is formally incorporated, and provide guidance through the transition from academic research to commercial product that many technical founders find the most challenging part of the journey.

For Nordic AI and software founders who are still in the academic phase or have recently completed research programs, PSV Tech represents one of the most accessible and domain-appropriate early institutional partners available. The combination of pre-seed capital, genuine technical understanding, and physical campus presence creates a level of founder proximity that traditional VC firms operating from city-center offices cannot replicate.

|

Key Takeaways |

|

•

PSV Tech's physical

presence at DTU allows it to identify and build relationships with technical

founders during their academic programs, well before formal fundraising. |

|

•

€70M Fund II provides

meaningful capital to support Nordic founders in AI, software, and digital

infrastructure at the pre-seed stage. |

|

•

The campus-embedding

model creates a sourcing advantage that traditional VC firms cannot replicate

from city-center offices. |

|

•

Nordic technical

founders in academia or recently completing research programs should consider

PSV as one of their earliest institutional conversations. |

💼 1000+ Angel Investors Database

A founder-grade investor list designed to help you raise faster. No guesswork. No outdated contacts.

- ✔️ Handpicked investor database

- ✔️ Early-stage focused

- ✔️ Save weeks of research

- ✔️ Used by startup founders

Central and Eastern Europe: The Region's Most Active Early-Stage Funds

Central and Eastern Europe has emerged as one of the most compelling underappreciated venture markets in the world. The region is home to 170 million people, a combined GDP of approximately $2 trillion, and an extraordinary density of engineering talent. Companies like UiPath, ElevenLabs, Productboard, Mews, and Docplanner have demonstrated that CEE can produce globally competitive, category-defining technology companies. The following funds are deploying fresh capital specifically into this ecosystem.

18. Credo Ventures – First Cheque for CEE Founders with a World-Class Track Record

|

Credo

Ventures |

|

Fund Size: $88M Fund

V (March 2026) Check Size: $1M to $5M

per deal Focus: Pre-seed,

sector-agnostic, CEE founders and diaspora Geography: CEE (Prague

and Krakow) with reach to US and UK diaspora Notable:

Early investor in UiPath ($35B IPO) and ElevenLabs ($11B valuation) |

Credo Ventures is the most successful early-stage venture fund to emerge from Central and Eastern Europe, and its track record is built on two investments that speak for themselves: UiPath and ElevenLabs. In both cases, Credo led or co-led the pre-seed round before the companies were widely known. UiPath went on to list on the NYSE at a $35 billion valuation. ElevenLabs was most recently valued at approximately $11 billion. Both outcomes started with Credo writing the first institutional check.

Fund V at $88 million, raised in a single closing in March 2026, is the firm's largest to date, stepping up from the €75 million fourth fund closed in 2022. The fund is managed by six partners: founding partners Ondrej Bartos and Jan Habermann, alongside Maciek Gnutek (Poland market and diaspora), Jakub Krikava (public policy and Czech defence), Max Kolowrat-Krakowsky (international investment and US networks), and Matej Micek (infrastructure, AI, and developer tools).

The multi-generational partnership structure is deliberate, ensuring that Credo has the networks, perspective, and energy to maintain its position as the fund of choice for CEE founders for the next decade. The firm's thesis is clear: CEE is no longer an underdog market but a proven producer of globally competitive technology companies, and the structural advantages of deep regional knowledge, diaspora access, and founder trust create a moat that outside investors cannot easily replicate.

Credo invests in founders from CEE as well as diaspora entrepreneurs who have built careers in the US, UK, or other major tech hubs but maintain strong connections to the region. Check sizes of $1 million to $5 million position Credo as a meaningful lead investor capable of setting round terms and providing genuine support rather than simply adding a name to a cap table.

|

Key Takeaways |

|

•

Credo backed both

UiPath (which IPO'd at $35B) and ElevenLabs (valued at $11B) at the pre-seed

stage before either was widely known. |

|

•

$88M Fund V raised in

March 2026 in a single close, meaning Credo is one of the most recently

capitalized and actively deploying funds on this list. |

|

•

The firm invests in

both CEE-based founders and diaspora entrepreneurs in the US and UK,

broadening the accessible founder pool significantly. |

|

•

Two of Credo's

previous funds delivered returns exceeding 10x, placing the firm firmly in

top-percentile performance within European venture. |

|

•

LPs include Adams

Street, RSJ, Sequoia, Isomer, and Marktlink, with approximately two-thirds

institutional capital. |

19. Day One Capital – Pre-Seed and Seed B2B Software Across CEE

|

Day One

Capital |

|

Fund

Size: €45M Fund III (second close

completed, final close expected in early 2026) Check

Size: €500,000 to €2.5M per deal,

leading or co-leading rounds Focus:

B2B software and deep tech, with

increasing emphasis on multi-agent applications, robotics, and cybersecurity Geography:

CEE -- Budapest-based with pan-CEE

investment mandate Notable:

Founded by Elek Straub, Gyorgy

Simo, and Csaba Kakosy in 2012; 4 companies from Fund II have surpassed $100M

valuation; exits include Tresorit, Gamee (acquired by Animoca Brands), and

AImotive (acquired by Stellantis) |

Day One Capital was founded in 2012 with a €4 million debut fund and has grown through three vehicles to become one of the most established early-stage investors in the Hungarian and wider CEE startup ecosystem. The name reflects the firm's investment philosophy explicitly: Day One Capital aims to be the partner that commits when the evidence is thinnest and the conviction requirement is highest, the actual first day of a company's institutional journey.

Fund III at €45 million, with €45 million secured at second close and final close expected in early 2026, represents a material step-up from the €34 million second fund. The investment thesis has evolved meaningfully. In earlier funds, roughly 75 percent of investments were B2B SaaS companies with 25 percent in what the team calls deep tech. The partners expect Fund III's allocation to be nearly the reverse, with deep tech including multi-agent AI applications, robotics, and cybersecurity expected to represent the majority of new deals.

The portfolio track record from Fund II demonstrates the quality of the firm's early judgment. Four portfolio companies have surpassed $100 million in valuation, with three more expected to cross that threshold. Companies have attracted follow-on investments from Lightspeed Venture Partners, Lakestar, Dawn Capital, Molten Ventures, Partech, and Hoxton Ventures, demonstrating that Day One's early bets translate into companies sophisticated global investors want to continue backing.

Fund III is already active, with the first two investments co-led by UK and Netherlands-based investors. Two additional deals co-led by German funds were in process at time of writing. The fund plans five to six new investments annually, maintaining a deliberate pace that allows genuine partner engagement with every portfolio company.

|

Key Takeaways |

|

•

Day One Capital is

shifting its Fund III thesis from predominantly B2B SaaS toward deep tech,

robotics, multi-agent AI, and cybersecurity, reflecting the evolution of the

CEE startup opportunity. |

|

•

Four Fund II companies

have already surpassed $100M valuation with follow-on investors including

Lightspeed, Lakestar, Dawn, and Partech. |

|

•

Exits include AImotive

acquired by Stellantis (Hungary's largest startup acquisition) and Gamee

acquired by Animoca Brands ($5.9B unicorn). |

|

•

Fund III is actively

deploying with initial investments already completed and partnership co-led

by UK, Netherlands, and German funds. |

|

•

The day-one investment

philosophy means Day One commits before traction exists, making it accessible

to CEE founders at the very earliest stages. |

20. Soulmates Ventures – Sustainable Tech with SFDR Article 9 Classification

|

Soulmates

Ventures |

|

Fund

Size: €50M fund Check

Size: Up to €3M per deal, with

follow-on funding up to €5M Focus:

Sustainable technology across eight

defined streams: Air, Water, Energy, Mobility, Circular Economy, Food and

Agriculture, Healthcare, and Education Geography:

Europe (expanding from CEE roots to

pan-European coverage) Notable:

SFDR Article 9 classification --

the EU's highest standard for sustainable finance; founded by Hynek Sochor in

2020; portfolio includes eAgronom, Kardi AI, Twinzo, Flowpay, Signapse AI,

Fusebox; named Best VC of the Year at Global Startup Awards |

Soulmates Ventures occupies a genuinely distinctive position in European venture: it is one of very few early-stage funds to operate with full SFDR Article 9 classification, the European Union's highest standard for sustainable financial products. Article 9 classification is not merely a label. It requires that every investment made by the fund contributes directly and demonstrably to a specific sustainable objective, that detailed ESG performance data is tracked and reported for every portfolio company, and that the fund's sustainability claims are verified against EU Taxonomy standards. Soulmates chose to adopt this classification voluntarily, as funds of its size are not legally required to comply, specifically to demonstrate that rigorous sustainability standards and competitive financial returns are not in conflict.

The investment thesis is organized around eight defined sustainability streams: Air, Water, Energy, Mobility, Circular Economy, Food and Agriculture, Healthcare, and Education. Within each stream, Soulmates backs startups with scalable products that create measurable positive environmental or social impact. Check sizes up to €3 million per deal with follow-on capacity to €5 million allow the fund to support companies across the full early-stage spectrum from initial product development through meaningful scaling.

The SFDR Article 9 classification creates a unique commercial dynamic. Many institutional investors, including pension funds, endowments, and family offices, have specific allocation mandates for Article 9-classified investments. By meeting this standard, Soulmates attracts LP capital from pools that cannot invest in conventional venture funds, expanding the firm's fundraising addressable market. This benefits portfolio companies indirectly, as a well-capitalized fund partner with diverse institutional backing is better positioned to support companies through their growth trajectories.

The firm's portfolio includes eAgronom, a sustainable agriculture data platform; Signapse AI, working on AI-powered sign language translation to improve accessibility; and Kardi AI, among other companies across its eight sustainability themes. Soulmates was recognized as Best VC of the Year at the Global Startup Awards, validating both its investment quality and its leadership in demonstrating that sustainability-focused venture capital can compete on financial returns.

|

Key Takeaways |

|

•

Soulmates Ventures is

one of very few European early-stage funds with SFDR Article 9

classification, voluntarily meeting the EU's highest sustainable finance

standard. |

|

•

Article 9 status

attracts institutional LPs with mandatory sustainable investment allocation

requirements, diversifying the fund's capital base beyond conventional

venture LP pools. |

|

•

The eight defined

sustainability streams (Air, Water, Energy, Mobility, Circular Economy, Food

and Agriculture, Healthcare, and Education) create a clear, structured

investment mandate. |

|

•

Up to €3M per deal

with follow-on to €5M allows Soulmates to support founders across the full

early-stage spectrum from initial development through growth. |

|

•

Named Best VC of the

Year at the Global Startup Awards, providing external validation of

investment quality alongside the sustainability mission. |

21. Zero One Hundred – CEE Pre-Seed with MENA Co-Investments

|

Zero One

Hundred |

|

Fund

Size: €25M Fund II Check

Size: Varies by deal Focus:

Technology companies,

sector-agnostic, with 70 percent allocated to CEE and 30 percent to MENA

co-investments Geography:

CEE (primary) and MENA

(co-investments) Notable:

Unique dual-geography mandate

bridging Central and Eastern Europe with the Middle East and North Africa |

Zero One Hundred operates the most geographically distinctive mandate on this list, allocating approximately 70 percent of Fund II to pre-seed and seed investments in CEE and reserving 30 percent for co-investments alongside local GPs in the MENA region. This dual-geography structure reflects a thesis that the two ecosystems share more in common than geography suggests: both have extraordinary technical talent density relative to the capital available, both are producing founders with global commercial ambitions who struggle to access institutional capital from traditional Western European or US-based funds, and both have growing diaspora communities in major technology hubs who maintain strong connections to their home markets.

The CEE allocation follows the established pattern of backing technical founders at the pre-seed and seed stages in markets including Poland, Czech Republic, Slovakia, Hungary, Romania, and the wider region. The MENA co-investment structure is more distinctive: rather than building its own deal flow and diligence capacity across the complex and diverse MENA ecosystem, Zero One Hundred deploys capital alongside local GPs who have the regional knowledge, network, and regulatory understanding needed to identify and support quality companies in markets from the UAE to Egypt to Saudi Arabia.

Fund II at €25 million is modest in size relative to the geographic ambition it represents, but the fund's positioning as a first-check or early-check investor rather than a large seed leader means the capital can cover a meaningful number of companies across both regions. For founders in CEE building technology companies, the MENA co-investment network also represents a potential commercial and customer development resource that most CEE-only funds cannot offer.

|

Key Takeaways |

|

•

Zero One Hundred's

70/30 CEE/MENA split is structurally unique, bridging two of the world's most

technically talented but undercapitalized startup ecosystems. |

|

•

The MENA co-investment

model deploys capital alongside local GPs rather than building independent

MENA expertise, creating speed and quality in a complex regional landscape. |

|

•

CEE founders in the

portfolio gain access to a MENA co-investment network that most CEE-only

funds cannot offer, creating commercial and customer development

opportunities. |

22. FIRSTPICK – First Institutional Check for Baltic Founders at Inception Stage

|

FIRSTPICK |

|

Fund

Size: €25M Fund II -- closed in

March 2026 Check

Size: €100,000 to €500,000 per

ticket Focus:

All technology sectors, Baltic

founders from inception stage Geography:

Baltics -- Estonia, Latvia, and

Lithuania Notable:

One of the earliest-stage

institutional funds in the Baltic ecosystem; Fund II closed March 2026 making

it one of the freshest deployment windows on this list |

FIRSTPICK closed Fund II in March 2026 with €25 million dedicated to backing Baltic founders at the inception stage with tickets from €100,000 to €500,000. The timing makes FIRSTPICK one of the most recently capitalized funds on this entire list, meaning the firm is in the peak urgency phase of deployment right now. Partners are actively building the Fund II portfolio, deal review is a top priority, and the competitive dynamics that favor founders pitching recently closed funds are fully in effect.

The Baltic startup ecosystems of Estonia, Latvia, and Lithuania have an extraordinary track record relative to their combined population of approximately six million people. Skype was built in Estonia. TransferWise, now Wise and worth approximately $10 billion, was founded by Estonians. Pipedrive, the sales CRM that was acquired by Vista Equity Partners, emerged from the Estonian ecosystem. The proportion of technology companies, engineers, and experienced startup operators per capita in Estonia in particular is among the highest in the world.

FIRSTPICK's inception-stage focus positions it as the very first institutional partner for Baltic founders who have an idea, a team forming, or early validation but have not yet built enough to attract larger seed funds. The €100,000 to €500,000 ticket range is calibrated to provide meaningful capital for the earliest stages of company building without requiring a level of development that would make the investment seem more like early seed than genuine inception-stage backing. For Baltic founders who are at the very beginning of the journey, FIRSTPICK is the natural first call.

|

Key Takeaways |

|

•

FIRSTPICK Fund II

closed in March 2026, making it one of the freshest deployment windows on

this list with peak urgency and partner attention right now. |

|

•

The Baltic ecosystem

has produced Skype, Wise, Pipedrive, and dozens of strong technology

companies at extraordinary per-capita rates. |

|

•

€100K to €500K tickets

are calibrated specifically for inception-stage founders who are too early

for larger seed funds but need institutional backing to get started. |

|

•

All technology sectors

are considered, making FIRSTPICK relevant for Baltic founders across AI,

SaaS, fintech, deep tech, and other verticals. |

23. vastpoint – AI, B2B SaaS, and Healthtech in Poland

|

vastpoint |

|

Fund

Size: $22M debut fund Check

Size: €500,000 to €750,000 per deal Focus:

Artificial intelligence, B2B SaaS,

and healthtech at seed stage Geography:

Poland (with broader CEE

consideration) Notable:

Founded by a team with ElevenLabs

connections; debut fund focused on Poland's rapidly maturing startup

ecosystem |

vastpoint is a Poland-focused debut fund investing in AI, B2B SaaS, and healthtech companies at the seed stage. With $22 million in its first vehicle, the fund is designed to be a meaningful first institutional partner for Polish founders who have moved beyond the earliest ideation phase and are ready to scale their product and initial commercial traction with professional capital behind them.

Poland is one of Europe's largest and most technically sophisticated startup markets. Warsaw and Krakow have developed strong engineering talent pools, supported by a university system that consistently produces technically excellent computer science and engineering graduates. The country has produced a growing number of globally competitive technology companies including Booksy, Brainly, DocPlanner, and Allegro, and the ElevenLabs connection in the vastpoint founding team reflects the growing maturity of the Polish founder ecosystem as successful startup alumni invest in the next generation.

Check sizes of €500,000 to €750,000 per deal position vastpoint as a meaningful first professional investor rather than a small angel equivalent. This range allows the fund to lead or co-lead seed rounds and provide founders with both the capital and the institutional credibility to attract follow-on investment from larger European and global seed funds. For Polish founders building AI applications, B2B software, or digital health products, vastpoint represents dedicated specialist capital with genuine local ecosystem knowledge.

|

Key Takeaways |

|

•

vastpoint is a debut

Poland-focused fund at $22M investing €500K to €750K per deal in AI, B2B

SaaS, and healthtech at seed stage. |

|

•

Poland's engineering

talent pool and growing founder community make it one of Central Europe's

most compelling early-stage markets. |

|

•

The ElevenLabs

connections in the founding team reflect the maturing self-reinforcing nature

of the Polish startup ecosystem. |

|

•

Check sizes allow

vastpoint to lead or co-lead seed rounds and provide institutional

credibility to attract follow-on from larger European and global funds. |

24. 33East – EIF-Backed Pre-Seed and Seed in Cyprus

|

33East |

|

Fund

Size: €26M debut fund Check

Size: €500,000 to €1M per startup Focus:

Technology companies,

sector-agnostic Geography:

Cyprus -- with broader European

investment reach Notable:

Backed by the European Investment

Fund through EIF guarantee programs; debut fund actively deploying |

33East is a Cyprus-based EIF-backed debut fund investing €500,000 to €1 million per startup at the pre-seed and seed stages. The European Investment Fund backing provides both financial credibility and a clear signal about the fund's governance, institutional quality, and long-term sustainability. EIF backing requires fund managers to meet specific standards for team experience, investment process, and reporting, which distinguishes EIF-backed funds from purely privately raised vehicles.

Cyprus has been developing as a Mediterranean technology hub over the past decade, attracting founders from Eastern Europe, the Middle East, and North Africa who find the island's English-speaking business environment, EU regulatory status, favorable tax treatment for technology companies, and growing community of technology professionals increasingly attractive as a base for building European and global businesses. The 33East positioning within this ecosystem gives it access to a diverse founder base that spans multiple geographies and cultural backgrounds.

For founders based in Cyprus or considering Cyprus as a headquarters for a European startup, 33East represents the most directly relevant institutional early-stage investor. The EIF backing also means 33East can provide portfolio companies with introductions to the broader European Investment Fund ecosystem, including other EIF-backed funds across Europe that might serve as follow-on investors as portfolio companies scale beyond their initial rounds.

|

Key Takeaways |

|

•

33East is EIF-backed,

providing institutional credibility, governance quality, and access to the

broader European Investment Fund ecosystem for portfolio companies. |

|

•

Cyprus has been

developing as a Mediterranean tech hub, attracting founders from Eastern

Europe, the Middle East, and North Africa seeking an EU-based headquarters. |

|

•

€500K to €1M per

startup is meaningful institutional seed capital appropriate for founders at

the early product development and initial traction stages. |

|

•

Debut fund status

means 33East is in active portfolio-building mode, with all the urgency and

attention that characterizes a new fund's deployment phase. |

25. Clean Growth Fund – UK Climatetech Specialist

|

Clean

Growth Fund |

|

Fund Size: £49M

first close of £150M target Fund II Check Size: £500K to

£5M per deal Focus: UK climatetech

only Geography: UK Notable:

BEIS-supported; one of UK's longest-running dedicated climatetech funds |

Clean Growth Fund is the UK's most established dedicated climatetech venture fund, and Fund II's first close at £49 million against a £150 million target signals both current deployment capacity and significant additional capital still being raised. The fund invests exclusively in UK climatetech companies, with checks ranging from £500,000 to £5 million, a range wide enough to support companies from pre-revenue pre-seed through into meaningful growth.

The climatetech investment thesis has become increasingly compelling as the cost trajectories of renewable energy, battery storage, electric vehicles, and sustainable materials have improved dramatically relative to fossil fuel alternatives. Regulatory tailwinds in the UK, including the UK government's commitment to net zero by 2050 and the various clean energy incentive programs that have followed, create a favorable commercial environment for climatetech startups selling into both business and government customers.

Clean Growth Fund's exclusivity around climatetech means the firm has developed deep expertise in the commercial challenges specific to this category: long sales cycles with utilities and government bodies, the capital intensity of hardware-adjacent businesses, and the complexity of measuring and verifying environmental impact. For climatetech founders, this specialist knowledge is often more valuable than capital from a generalist fund that lacks the domain experience to provide meaningful operational support.

The combination of government support, institutional LP participation, and a clear technology improvement curve across multiple climatetech sub-sectors makes this fund particularly well-positioned. Founders building in energy storage, grid management software, sustainable construction, carbon capture, sustainable food systems, or industrial decarbonization should be aware that Clean Growth Fund represents dedicated specialist capital for exactly these types of businesses.

|

Key Takeaways |

|

•

Clean Growth Fund is

one of the UK's longest-running dedicated climatetech funds, with £49M

deployed so far against a £150M target for Fund II. |

|

•

Check sizes from £500K

to £5M allow the fund to support companies across the full early-stage

spectrum, from pre-product to growth. |

|

•

Specialist climatetech

expertise in sales cycles, hardware complexity, and impact measurement

provides portfolio companies with genuinely sector-specific support. |

|

•

Regulatory tailwinds

in the UK create a favorable commercial environment for climatetech startups

serving utilities and government customers. |

Comprehensive Fund Comparison Table

The table below provides a side-by-side comparison of all 25 funds covered in this guide, organized by geography within each region. Use this as a quick reference to identify the funds that match a specific founder's stage, check size requirement, geographic situation, and sector focus.

|

Fund

Name |

Stage |

Fund

Size |

Check

Size |

Geography |

Focus |

|

Afore Capital |

Pre-seed |

$185M |

$50K–$2M+ |

Global / USA |

Software, all sectors |

|

Gradient (Google) |

Pre-seed / Seed |

$220M |

N/A |

Global |

AI-only |

|

Primary Venture Partners |

Pre-seed / Seed |

$625M |

$5M–$10M |

USA (nationwide) |

Generalist |

|

Redbud VC |

Pre-seed / Seed |

$25M |

N/A |

USA (Midwest) |

Operator-led, no pedigree

filter |

|

Better Tomorrow Ventures |

Pre-seed / Seed |

$140M |

$500K–$4M |

Global |

Fintech |

|

Concept Ventures |

Pre-seed |

$88M |

Up to $1.5M |

UK / Europe |

All sectors |

|

DIG Ventures |

Pre-seed / Seed |

$100M |

N/A |